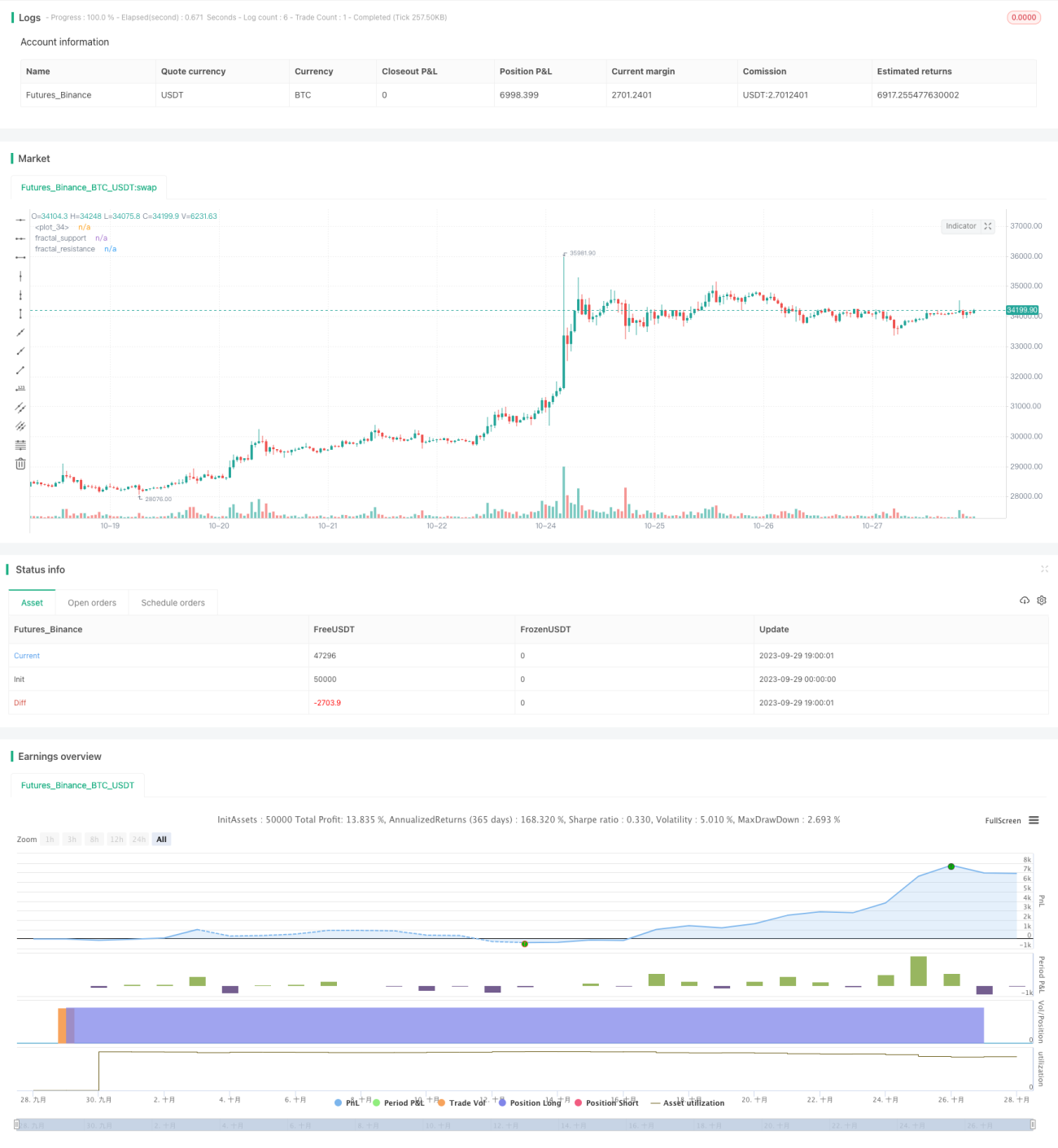

Estrategia de trading de reversión basada en soporte/resistencia generalizado

Resumen

Esta estrategia se basa en la reversión de operaciones utilizando factores largos/cortos de indicadores, y establece puntos de obtención de beneficios objetivo. El núcleo del factor largo/corto es una forma ampliada de "soporte/resistencia generalizada" basada en el volumen de operaciones, adecuada para activos con alto volumen de negociación y volatilidad. La ventaja de la estrategia es que puede capturar oportunidades de reversión de tendencia a mediano y corto plazo de gran magnitud, obteniendo ganancias rápidamente; sin embargo, también conlleva el riesgo de quedar atrapado en posiciones perdedoras.

Principio de la estrategia

-

Identificación de factores largos/cortos mediante "soporte/resistencia generalizada" basada en el volumen de operaciones

-

Se utiliza la morfología de las velas para identificar soportes/resistencias clásicos, filtrando falsas rupturas con alto volumen de operaciones.

-

El soporte/resistencia generalizada tiene una mejor cobertura que las formaciones clásicas.

-

La ruptura del soporte generalizado es una señal de factor largo, mientras que la ruptura de la resistencia generalizada es una señal de factor corto.

-

-

Operaciones de reversión

-

Después de que se emite la señal del factor, se realiza la operación contraria.

-

Si ya hay una posición abierta, se reduce o se abre una posición contraria.

-

-

Establecimiento de objetivos de ganancias

-

Se fija un stop loss basado en el ATR.

-

Se establecen múltiples objetivos de ganancia, como 1R, 2R, 3R, etc.

-

Al alcanzar diferentes objetivos, se reduce la posición en lotes.

-

Análisis de ventajas

-

Puede capturar reversiones significativas a mediano y corto plazo

Las rupturas de soporte/resistencia representan señales de reversión de tendencia relativamente confiables, capaces de capturar movimientos considerables a mediano y corto plazo.

-

Ganancias rápidas y reducción de drawdown

Mediante el uso de stop loss y múltiples objetivos de ganancia, se pueden obtener ganancias rápidas y limitar el retroceso individual de los activos.

-

Adecuado para activos con alta participación de capital institucional y volatilidad

La estrategia depende del indicador de volumen, requiriendo suficiente flujo de capital institucional para respaldar la tendencia, así como cierto margen de volatilidad para lograr ganancias.

Análisis de riesgos

-

Riesgo de quedar atrapado en mercados laterales

En mercados laterales, las operaciones de salida con stop loss y reingreso contrario pueden provocar quedar atrapado con frecuencia.

-

Riesgo de falla de soporte y resistencia

Los niveles de soporte/resistencia generalizada no son absolutamente confiables; existe la probabilidad de que fallen en la prueba de reversión.

-

Riesgo de posiciones unidireccionales

La estrategia es puramente de reversión, sin considerar el seguimiento de tendencia, lo que podría hacer perder oportunidades direccionales importantes.

-

Aspectos de gestión de riesgos

-

Se pueden relajar adecuadamente las condiciones del factor de reversión, sin necesidad de revertir cada ruptura.

-

Se puede combinar con otros indicadores de filtro, como divergencia de precio-volumen.

-

Se puede optimizar la estrategia de stop loss para reducir la probabilidad de quedar atrapado.

-

Direcciones de optimización

-

Optimizar parámetros de alcance

Optimizar los parámetros del soporte/resistencia generalizada para identificar factores más confiables.

-

Optimizar la estrategia de obtención de ganancias

Se pueden agregar más niveles de objetivos de ganancia o utilizar objetivos no fijos.

-

Optimizar la estrategia de stop loss

Ajustar los parámetros del ATR o utilizar stop loss estadísticos para reducir los costos de transacción causados por stop loss innecesariamente agresivos.

-

Combinar con tendencia y otros factores

Se puede introducir el juicio de tendencia mediante medias móviles para evitar una confrontación severa con la tendencia; también se pueden incorporar otros factores auxiliares.

Conclusión

El núcleo de esta estrategia es utilizar la reversión para capturar movimientos significativos a mediano y corto plazo. La idea de la estrategia es simple y directa, y mediante el ajuste de parámetros se pueden obtener buenos resultados en el trading real. Sin embargo, la estrategia de reversión es agresiva y conlleva cierto drawdown y riesgo de quedar atrapado, por lo que es necesario optimizar aún más las estrategias de stop loss y obtención de ganancias, y combinar adecuadamente con el juicio de tendencia para reducir pérdidas innecesarias.

- 1