Estrategia de ruptura de volatilidad dinámica

Resumen

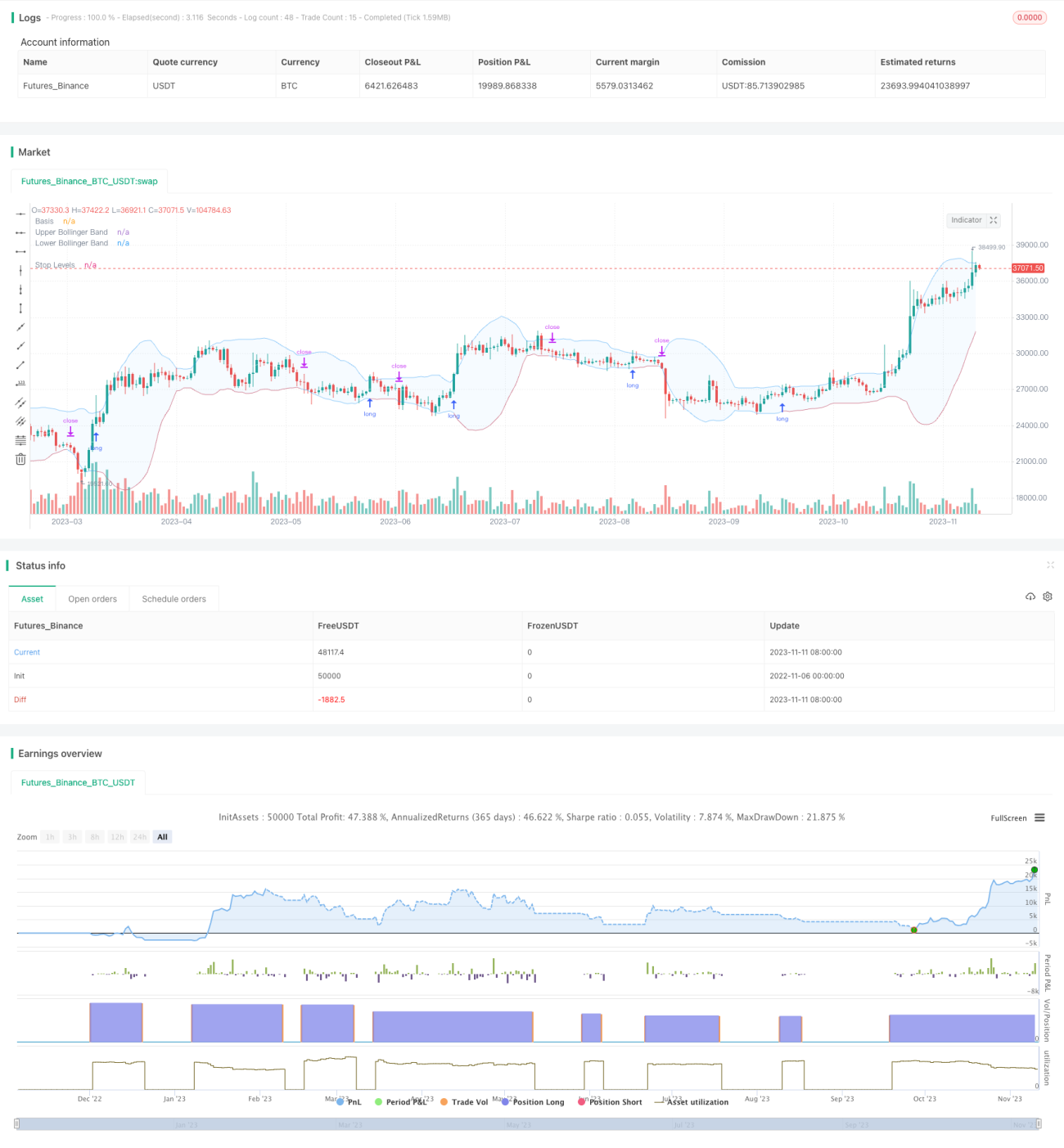

Esta estrategia utiliza las bandas superior e inferior dinámicas de Bollinger para generar señales de compra cuando el precio supera la banda superior y de cierre cuando el precio cae por debajo de la banda inferior. A diferencia de las estrategias de ruptura tradicionales, las bandas de Bollinger se ajustan dinámicamente según la volatilidad histórica, lo que permite identificar mejor las condiciones de sobrecompra y sobreventa del mercado.

Principio de la Estrategia

La estrategia se basa principalmente en el indicador de Bandas de Bollinger para detectar rupturas de precio. Las Bandas de Bollinger constan de tres líneas:

- Línea media: media móvil de n días

- Banda superior: línea media + k * desviación estándar de n días

- Banda inferior: línea media - k * desviación estándar de n días

Cuando el precio sube por encima de la banda superior, se considera que el mercado está en condiciones de sobrecompra, por lo que se puede tomar una posición larga. Cuando el precio cae por debajo de la banda inferior, se considera que el mercado está en condiciones de sobreventa y se debe cerrar la posición.

La estrategia permite personalizar los parámetros de las Bandas de Bollinger: la longitud de la línea media (n) y el múltiplo de la desviación estándar (k). La configuración predeterminada es una línea media de 20 días y un múltiplo de desviación estándar de 2.

Al cierre de cada día de negociación, se verifica si el precio de cierre ha superado la banda superior. De ser así, al día siguiente al abrir el mercado se ejecuta una señal de compra. Una vez en largo, se monitorea en tiempo real si el precio rompe la banda inferior; si lo hace, se cierra la posición.

La estrategia también incorpora un filtro de media móvil: solo se genera una señal de compra cuando el precio está por encima de la media móvil. Se puede elegir dibujar la media móvil en el período actual o en un período superior para controlar el momento de entrada.

Además, se ofrecen dos opciones de stop loss: un stop loss fijo porcentual o un trailing stop basado en la banda inferior de Bollinger. Esta última opción proporciona más espacio para que las ganancias sigan su curso.

Ventajas de la Estrategia

- Utiliza las Bandas de Bollinger para identificar condiciones de sobrecompra/sobreventa en el mercado.

- Filtro de media móvil para evitar operar en contra de la tendencia.

- Parámetros de Bandas de Bollinger personalizables, adaptables a diferentes períodos.

- Ofrece dos opciones de stop loss.

- Admite backtesting para optimizar parámetros y validación en tiempo real.

Riesgos de la Estrategia

- Las Bandas de Bollinger no siempre identifican correctamente las condiciones de sobrecompra/sobreventa.

- El filtro de media móvil puede hacer que se pierdan oportunidades de ruptura rápida.

- El stop loss fijo puede ser demasiado conservador, mientras que el trailing stop puede ser demasiado agresivo.

- Requiere optimización de parámetros para adaptarse a diferentes activos y períodos.

- No limita el tamaño de las pérdidas; se debe considerar la gestión del capital.

Optimización de la Estrategia

- Probar diferentes combinaciones de parámetros de media móvil.

- Experimentar con diferentes parámetros de las Bandas de Bollinger.

- Comparar la rentabilidad entre el stop loss porcentual fijo y el trailing stop basado en la banda inferior.

- Agregar un módulo de gestión de capital para limitar pérdidas por operación.

- Combinar con otros indicadores para validar las señales de las Bandas de Bollinger.

Conclusión

Esta estrategia utiliza las bandas superior e inferior dinámicas de Bollinger para determinar sobrecompra/sobreventa, se apoya en un filtro de media móvil para las señales y emplea stop loss para proteger el capital. En comparación con las rupturas de bandas fijas tradicionales, se adapta mejor a la volatilidad del mercado. Mediante la optimización de parámetros y el control de riesgos, se puede mejorar aún más la estabilidad y la rentabilidad de la estrategia. En general, esta estrategia aprovecha la naturaleza dinámica de las Bandas de Bollinger para obtener las ventajas de las estrategias de ruptura, por lo que merece ser validada en tiempo real y optimizada a largo plazo.

- 1