Estrategia de momentum de reversión a la media

Resumen

La estrategia de momentum de reversión a la media es una estrategia de trading de tendencia que sigue el promedio de precios a corto plazo. Combina indicadores de reversión a la media e indicadores de momentum para evaluar la tendencia de mediano plazo del mercado.

Principio de la estrategia

La estrategia primero calcula la línea de reversión a la media y la desviación estándar de los precios. Luego, utilizando los umbrales superior e inferior predefinidos, determina si el precio ha superado un rango de una desviación estándar de la línea de reversión a la media. Si es así, se genera una señal de trading.

Para las señales largas, se requiere que el precio esté por debajo de la línea de reversión a la media en una desviación estándar, que el precio de cierre esté por debajo de la SMA del período LENGTH y por encima de la SMA de tendencia (TREND SMA). Si se cumplen estas tres condiciones, se abre una posición larga. La condición de cierre es que el precio supere al alza la SMA del período LENGTH.

Para las señales cortas, se requiere que el precio esté por encima de la línea de reversión a la media en una desviación estándar, que el precio de cierre esté por encima de la SMA del período LENGTH y por debajo de la SMA de tendencia. Si se cumplen estas tres condiciones, se abre una posición corta. La condición de cierre es que el precio supere a la baja la SMA del período LENGTH.

La estrategia también combina un porcentaje de beneficio objetivo y un porcentaje de stop loss para gestionar el take profit y el stop loss.

El método de salida puede ser mediante la ruptura de la media móvil o la ruptura de la regresión lineal.

A través de la combinación de operaciones largas y cortas, filtro de tendencia, take profit y stop loss, la estrategia logra identificar y seguir la tendencia de mediano plazo del mercado.

Ventajas de la estrategia

-

El indicador de reversión a la media puede determinar eficazmente si el precio se desvía del valor central.

-

El indicador de momentum SMA puede filtrar el ruido del mercado a corto plazo.

-

Las operaciones en ambas direcciones (largas y cortas) permiten capturar oportunidades de tendencia de manera integral.

-

El mecanismo de take profit y stop loss puede controlar eficazmente el riesgo.

-

El método de salida opcional permite adaptarse de manera flexible a las condiciones del mercado.

-

Es una estrategia completa de trading de tendencia que captura bien las tendencias de mediano plazo.

Riesgos de la estrategia

-

El indicador de reversión a la media es sensible a la configuración de parámetros; umbrales inadecuados pueden generar señales falsas.

-

En mercados con grandes oscilaciones, los stops pueden activarse con demasiada frecuencia.

-

En mercados laterales, la frecuencia de trading puede ser demasiado alta, aumentando los costos de transacción y el riesgo de deslizamiento.

-

Cuando la liquidez del activo es baja, el control del deslizamiento puede no ser óptimo.

-

Las operaciones en ambas direcciones implican un mayor riesgo, por lo que se requiere una gestión cuidadosa del capital.

Estos riesgos se pueden controlar mediante la optimización de parámetros, el ajuste de los métodos de stop loss y la gestión del capital.

Direcciones de optimización de la estrategia

-

Optimizar los parámetros de los indicadores de reversión a la media y momentum para que se adapten mejor a las características de diferentes activos.

-

Agregar indicadores de identificación de tendencia para mejorar la capacidad de reconocer tendencias.

-

Optimizar la estrategia de stop loss para que se adapte mejor a las grandes fluctuaciones del mercado.

-

Incorporar un módulo de gestión de posición que ajuste el tamaño de la posición según las condiciones del mercado.

-

Agregar más módulos de control de riesgo, como control de drawdown máximo y control de la curva de valor liquidativo.

-

Considerar la combinación con métodos de aprendizaje automático para optimizar automáticamente los parámetros de la estrategia.

Resumen

En resumen, la estrategia de momentum de reversión a la media, mediante un diseño de indicadores simple y efectivo, logra capturar la tendencia de reversión al valor de mediano plazo. La estrategia tiene una buena adaptabilidad y universalidad, pero también conlleva ciertos riesgos. Mediante la optimización continua y la combinación con otras estrategias, se pueden obtener mejores resultados. En general, esta estrategia es bastante completa y es un método de trading de tendencia que vale la pena considerar.

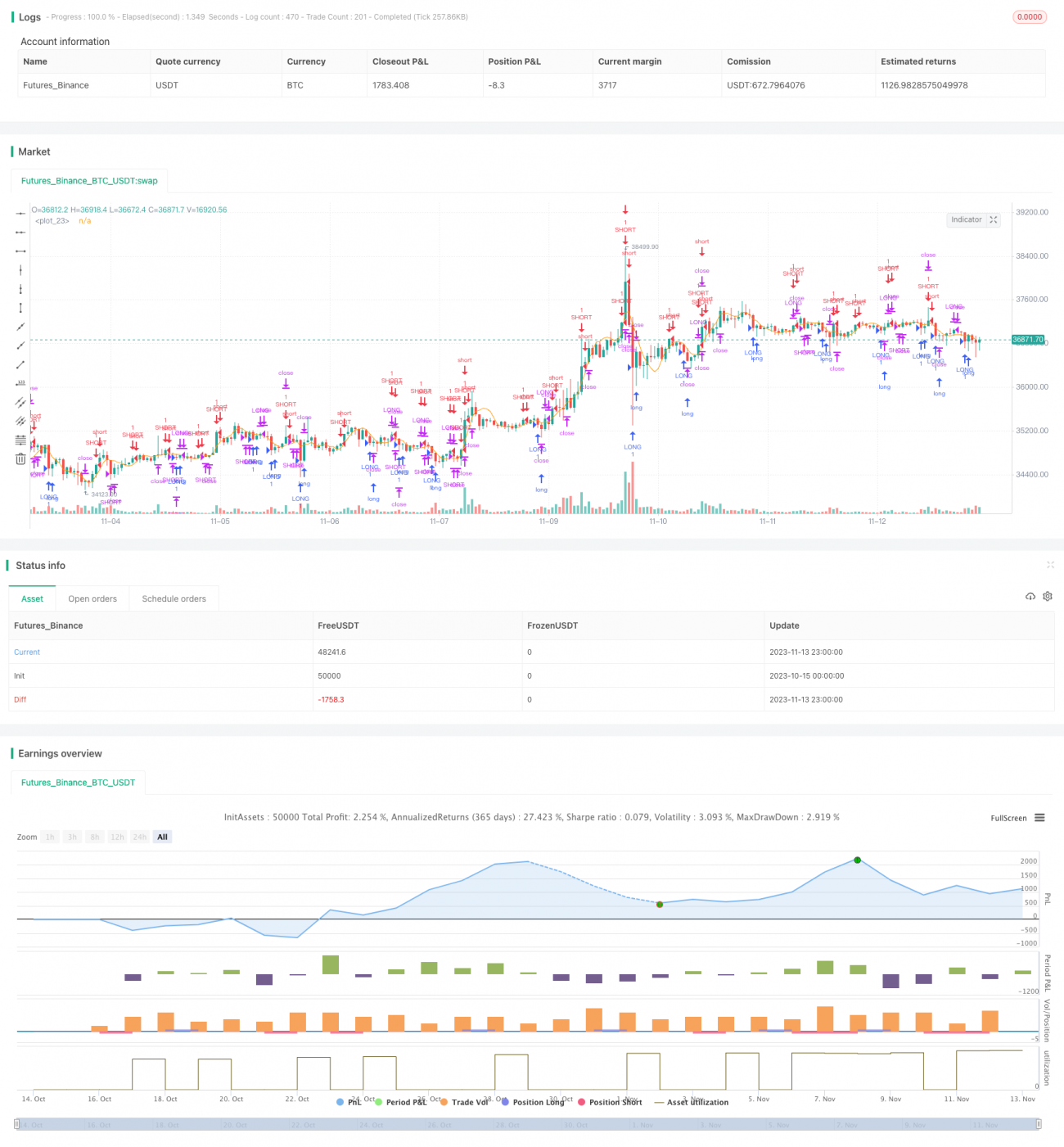

/*backtest

start: 2023-10-15 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © GlobalMarketSignals

//@version=4- 1