Estrategia de ruptura adaptativa PMax basada en los indicadores RSI y T3

Resumen

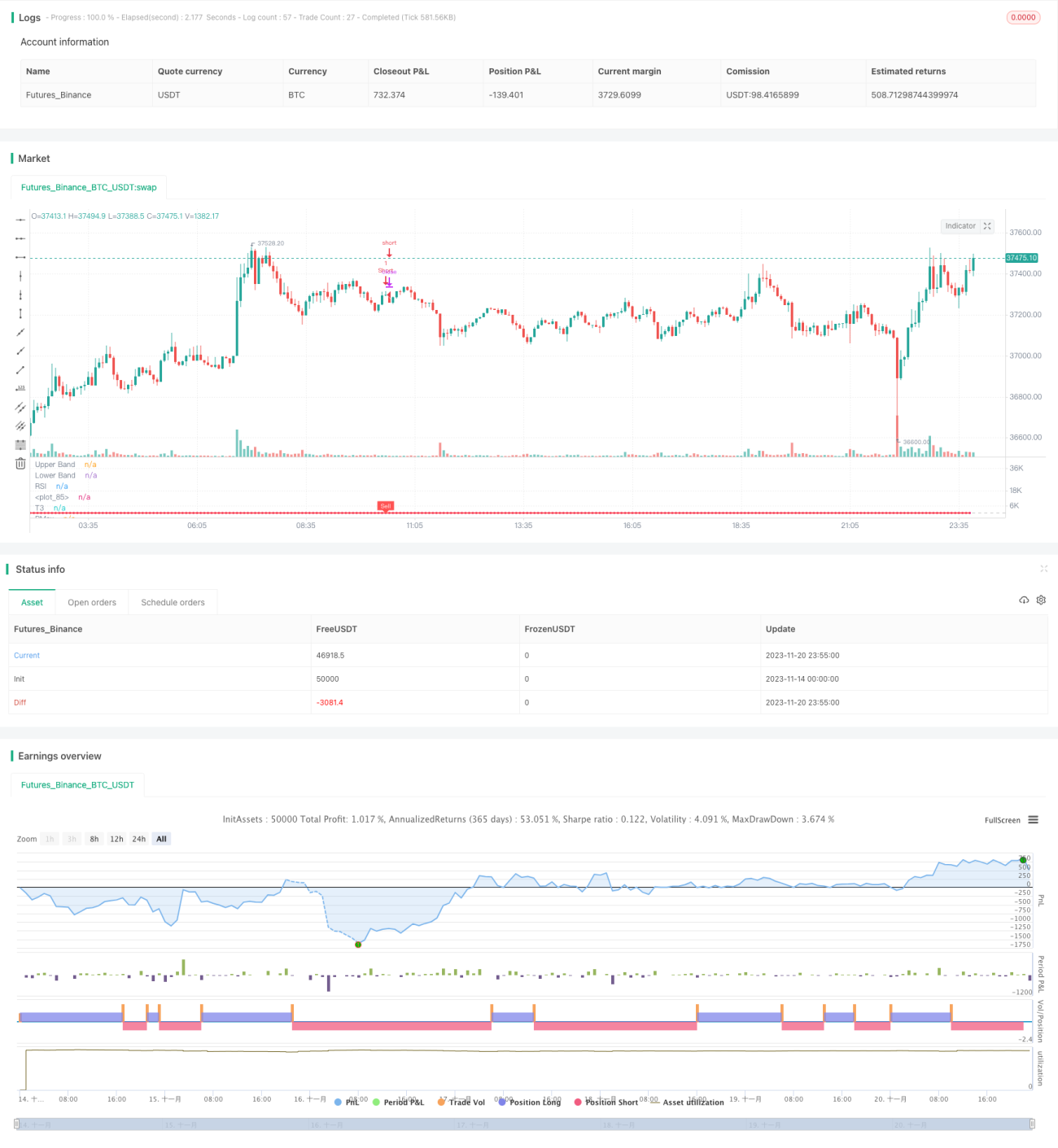

Esta estrategia es una estrategia de trading cuantitativa que utiliza los indicadores RSI y T3 para determinar la tendencia, combinados con el indicador ATR para establecer líneas de stop loss, logrando así una ruptura adaptativa PMax. Su idea principal es optimizar la determinación de la tendencia y la configuración del stop loss para controlar el riesgo mientras se mejora la rentabilidad.

Principio de la estrategia

-

Cálculo de los indicadores RSI y T3 para determinar la tendencia

- Utilizar el indicador RSI para detectar si la acción está sobrecomprada o sobrevendida

- Calcular el indicador T3 basado en el RSI para determinar la tendencia

-

Establecimiento de la línea de stop loss adaptativa PMax según el indicador ATR

- Calcular el indicador ATR como representación de la volatilidad

- Establecer líneas de stop loss por encima y por debajo del indicador T3, con un ancho igual a un múltiplo determinado del indicador ATR

- Lograr un ajuste adaptativo de la línea de stop loss

-

Compra por ruptura y salida por stop loss

- Cuando el precio cruza por encima del indicador T3, se considera una señal de compra

- Cuando el precio cruza por debajo de la línea de stop loss, se sale de la posición actual

Ventajas de la estrategia

Esta estrategia presenta principalmente las siguientes ventajas:

- La combinación de los indicadores RSI y T3 para determinar la tendencia ofrece una alta precisión

- El mecanismo de stop loss adaptativo PMax controla el riesgo

- El indicador ATR como representación de la volatilidad establece la amplitud de la línea de stop loss, evitando ser demasiado agresivo

- Equilibrio entre el drawdown y la rentabilidad

Riesgos de la estrategia

Esta estrategia presenta principalmente los siguientes riesgos:

-

Riesgo de reversión

Cuando se produce una reversión de precios a corto plazo, podría activarse el stop loss, generando pérdidas. Se puede ampliar ligeramente la línea de stop loss para reducir el impacto de la reversión.

-

Riesgo de fallo en la determinación de la tendencia

La efectividad de los indicadores RSI y T3 para determinar la tendencia no es 100% fiable; cuando la determinación es incorrecta, también puede generar pérdidas. Se pueden ajustar los parámetros o agregar otros indicadores para optimizar.

Direcciones de optimización de la estrategia

Esta estrategia se puede optimizar aún más en los siguientes aspectos:

- Agregar otros indicadores como medias móviles para ayudar a determinar la tendencia

- Optimizar los parámetros de longitud de los indicadores RSI y T3

- Probar diferentes múltiplos del ATR como amplitud de la línea de stop loss

- Ajustar la amplitud de la línea de stop loss según los diferentes mercados

Resumen

Esta estrategia integra las ventajas de los tres indicadores RSI, T3 y ATR, logrando una combinación orgánica de determinación de la tendencia y control de riesgos. En comparación con un indicador único, esta combinación ofrece una alta precisión en la determinación y un buen control del drawdown, siendo una estrategia de seguimiento de tendencia confiable. Todavía hay espacio para la optimización en parámetros y control de riesgos, pero en general es una estrategia de trading cuantitativa recomendable.

/*backtest

start: 2023-11-14 00:00:00

end: 2023-11-21 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © KivancOzbilgic

//developer: @KivancOzbilgic- 1