Estrategia adaptativa de take profit y stop loss basada en doble marco temporal e indicador de momentum

Resumen

Esta estrategia utiliza una combinación de marcos temporales duales e indicadores de impulso para lograr un take profit y stop loss adaptativos. El marco temporal principal monitorea la dirección de la tendencia, mientras que el marco temporal secundario se utiliza para confirmar las señales. Cuando ambos marcos están en la misma dirección, se genera una señal de trading. Una vez en el mercado, se emplea un método de take profit progresivo para actualizar los niveles de take profit y stop loss.

Principio de la estrategia

-

El marco temporal principal utiliza el indicador de regresión lineal Squeeze Momentum (SQM) para determinar la tendencia, mientras que el marco temporal secundario emplea una combinación de medias móviles (EMA) del SQM para filtrar señales falsas.

-

Cuando el SQM del gráfico principal rompe al alza y el SQM del gráfico secundario también está al alza, se abre una posición larga; cuando el SQM del gráfico principal rompe a la baja y el SQM del gráfico secundario también está a la baja, se abre una posición corta.

-

Tras la entrada, se establecen niveles iniciales de take profit y stop loss según los parámetros de entrada. Cuando el precio alcanza el take profit, se actualizan los niveles de take profit y stop loss. Específicamente: el take profit se incrementa en un porcentaje fijo, y el stop loss se reduce en un porcentaje fijo, logrando un take profit progresivo.

Ventajas de la estrategia

-

El marco temporal dual filtra señales falsas, garantizando la precisión de las señales.

-

El indicador SQM determina la dirección de la tendencia, evitando ser afectado por el ruido del mercado.

-

El mecanismo de take profit y stop loss adaptativo maximiza la fijación de ganancias y controla eficazmente el riesgo.

Análisis de riesgos

-

Si los parámetros del indicador SQM no se configuran adecuadamente, es posible perder puntos de inflexión de la tendencia, lo que puede generar pérdidas.

-

Si el marco temporal secundario no se elige correctamente, no filtrará eficazmente el ruido y puede generar operaciones erróneas.

-

Si la amplitud del stop loss es demasiado grande, la pérdida por operación podría ser considerable.

Direcciones de optimización

-

Los parámetros del indicador SQM deben ajustarse según los diferentes mercados para garantizar su sensibilidad.

-

El marco temporal secundario también debe probarse con diferentes períodos para determinar cuál tiene el mejor efecto de filtrado.

-

La amplitud del stop loss puede configurarse como un rango de fluctuación en lugar de un valor fijo, de modo que pueda ajustarse según la volatilidad del mercado.

Resumen

En general, esta estrategia es muy práctica. Combina marcos temporales duales con indicadores de impulso para determinar la tendencia y utiliza un método de take profit y stop loss adaptativo para lograr ganancias estables. Optimizando los parámetros del indicador SQM, el período del gráfico secundario y la configuración de la amplitud del stop loss, se puede mejorar el rendimiento de la estrategia, lo que la hace digna de ser aplicada y optimizada en operaciones reales.

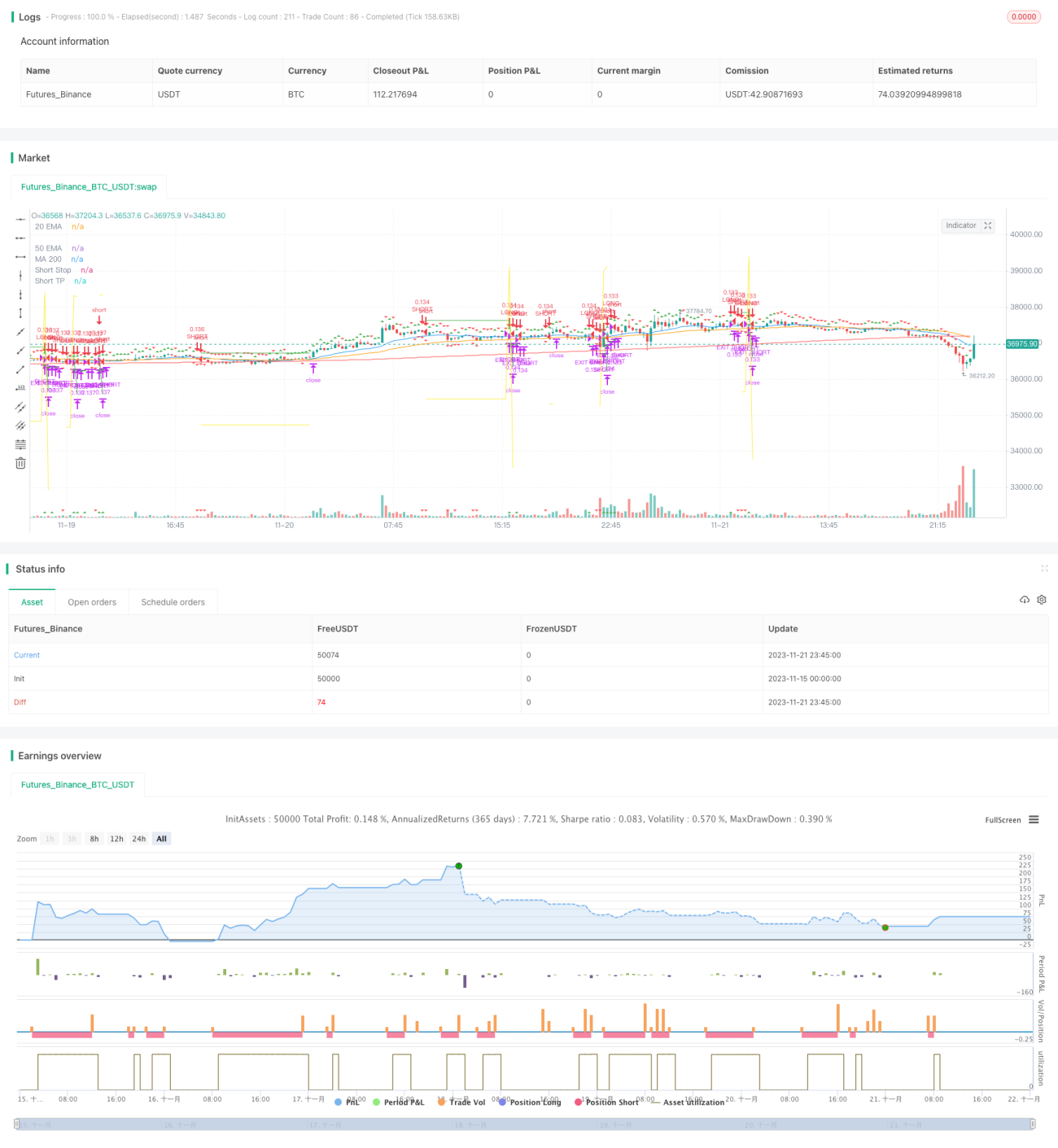

/*backtest

start: 2023-11-15 00:00:00

end: 2023-11-22 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("SQZ Multiframe Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

fast_ema_len = input(11, minval=5, title="Fast EMA")

slow_ema_len = input(34, minval=20, title="Slow EMA")- 1