Estrategia de indicadores técnicos de Bandas de Bollinger basada en descomposición de series temporales y ponderación por volumen

Resumen

Esta estrategia combina cuatro indicadores técnicos: descomposición de series temporales, precio promedio ponderado por volumen, bandas de Bollinger y delta (OBV-PVT), para lograr un juicio multidimensional de la tendencia de precios, sobrecompra y sobreventa.

Principio de la estrategia

- Utiliza la descomposición de series temporales para eliminar el ruido y la ciclicidad del precio, obteniendo un juicio de tendencia más preciso.

- Basándose en esa línea de tendencia, calcula un nuevo precio ponderado por volumen.

- Calcula el ancho porcentual de las bandas de Bollinger (BB%B) del precio de cierre para determinar sobrecompra/sobreventa.

- Calcula el cambio Delta(OBV-PVT) y su ancho porcentual en las bandas de Bollinger como criterio para medir divergencias precio-volumen.

- Genera señales de trading basadas en los cruces de los indicadores de precio-volumen y los rebasamientos/retrocesos de las bandas de Bollinger.

Ventajas

- Combina múltiples juicios de precio, volumen y características estadísticas, lo que otorga robustez a la estrategia.

- La combinación de BB%B y Delta(OBV-PVT) permite detectar mejor los fenómenos de sobrecompra/sobreventa a corto plazo.

- Las señales de cruce precio-volumen filtran parte de los puntos de trading ruidosos.

Análisis de riesgos

- La configuración de parámetros es demasiado compleja y difícil de ajustar.

- La oscilación en un rango corto puede aumentar las pérdidas.

- La divergencia precio-volumen no logra filtrar por completo las señales engañosas.

Se puede optimizar la estrategia ajustando los períodos de medias móviles, la amplitud de las bandas de Bollinger y la relación riesgo-beneficio, reduciendo la frecuencia de trading y aumentando la relación ganancia/pérdida por operación.

Resumen

Esta estrategia integra diversas herramientas analíticas como descomposición de series temporales, bandas de Bollinger e indicador OBV. A través de la combinación orgánica de la relación precio-volumen, características estadísticas y juicio de tendencia, logra identificar las réplicas a corto plazo y capturar efectivamente la tendencia principal del mercado. Sin embargo, también conlleva ciertos riesgos que deben mitigarse mediante el ajuste de parámetros para alcanzar un estado óptimo.

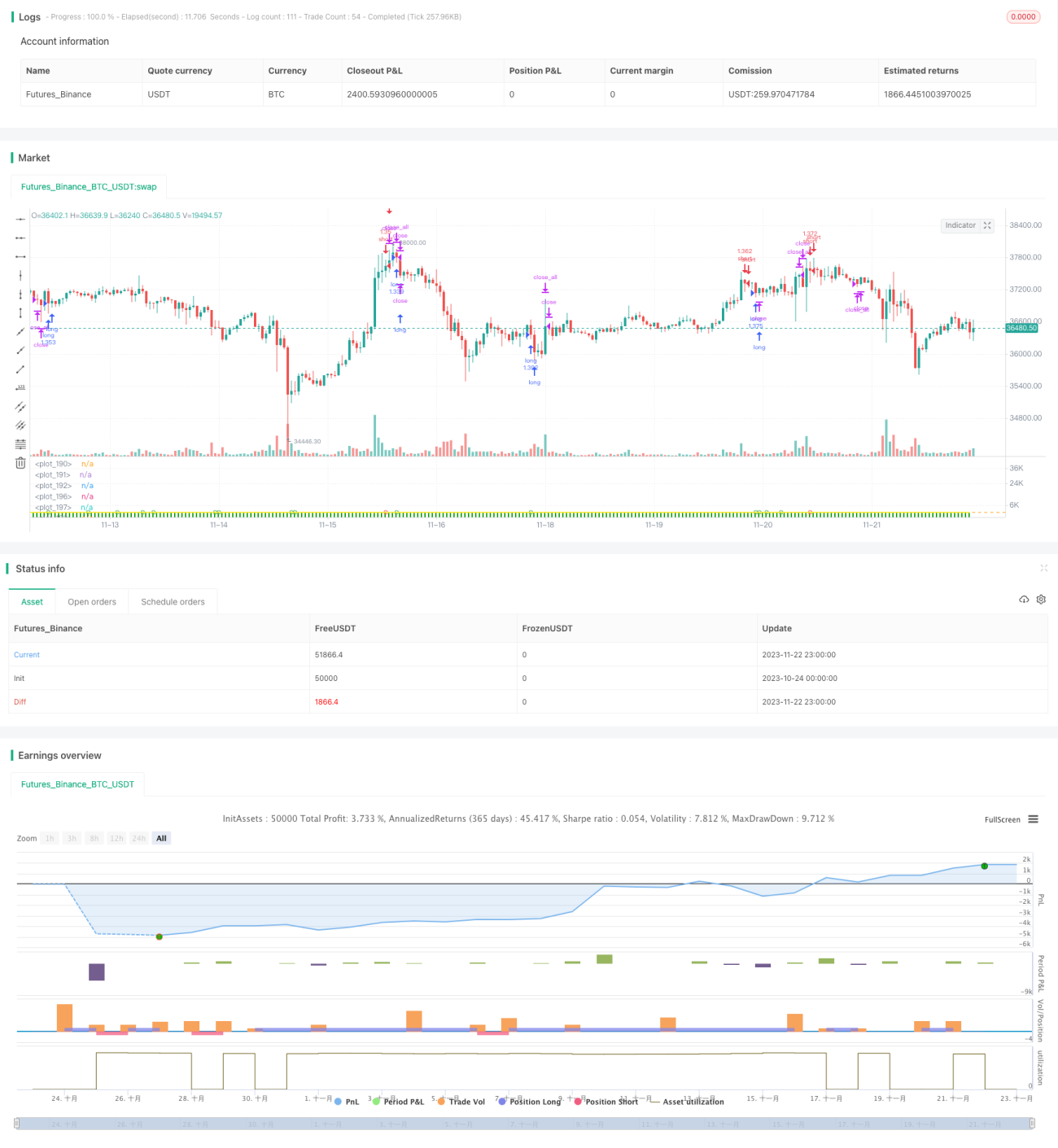

/*backtest

start: 2023-10-24 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © oakwhiz and tathal

- 1