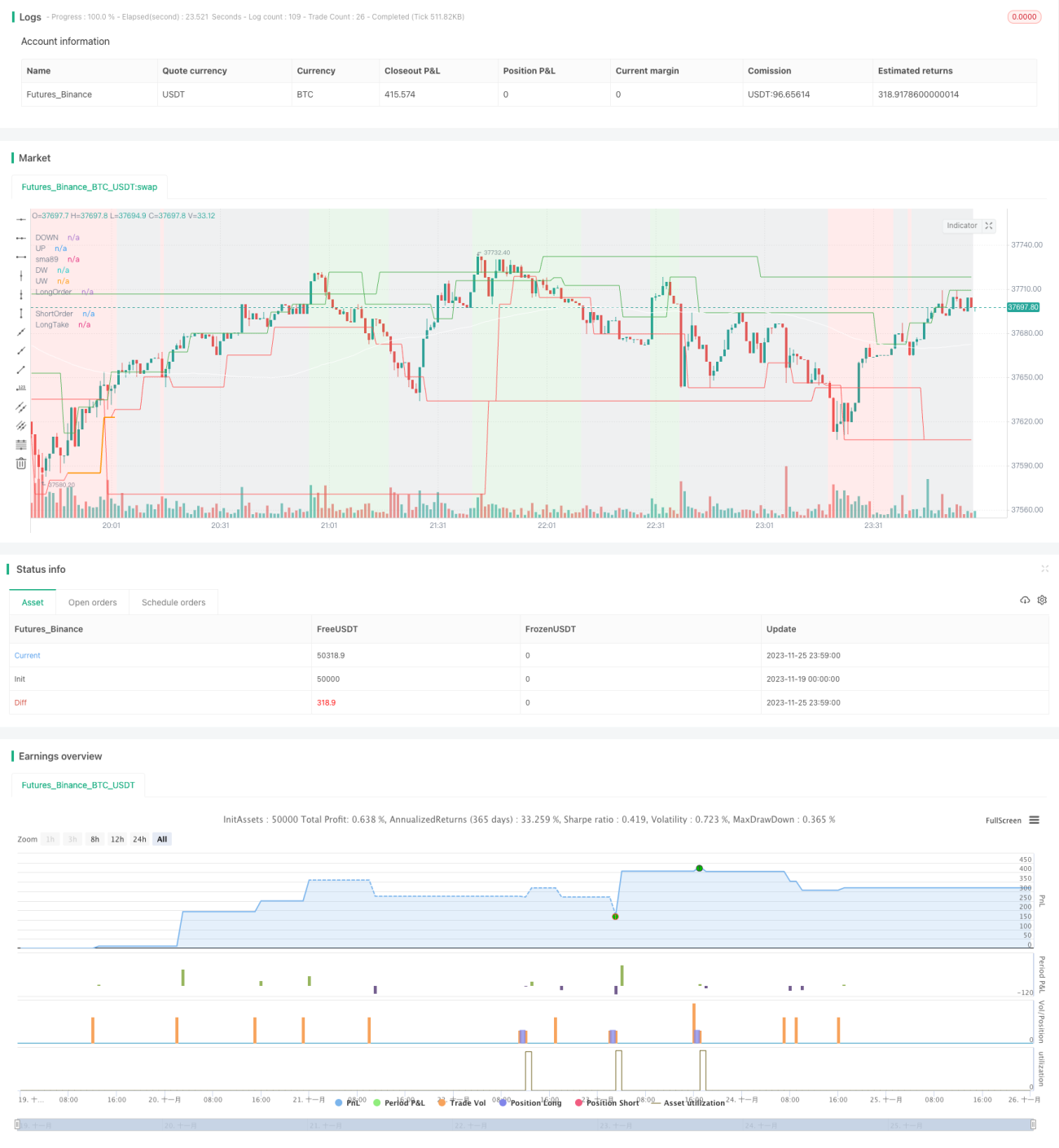

Estrategia de trading cuantitativo de alta frecuencia basada en doble filtro

Resumen

El nombre de esta estrategia es "Cuantificación de Doble Filtro". Utiliza un enfoque de marcos temporales múltiples para implementar una estrategia de trading cuantitativo de alta frecuencia basada en la idea de doble filtro. La estrategia emplea indicadores de diferentes marcos temporales para realizar juicios, logrando un filtrado más riguroso de las señales de trading, lo que permite eliminar una gran cantidad de señales falsas y obtener una mayor tasa de aciertos.

Principio de la Estrategia

El principio central de la estrategia es:

-

Utilizar las líneas semanales y diarias para determinar la dirección de la tendencia del mercado, como condición de filtrado direccional de la estrategia; solo se puede operar si se cumple la condición de tendencia.

-

En el marco temporal de 4 horas, se construye un canal para determinar los puntos de venta y compra, emitiendo señales de trading.

-

La consistencia de dirección entre las líneas semanales, diarias y el marco de 4 horas permite filtrar una gran cantidad de señales falsas, mejorando la fiabilidad de las señales de trading.

-

Utilizar los puntos de retroceso de Fibonacci para determinar los niveles de take profit y stop loss, logrando una rápida toma de ganancias y detención de pérdidas.

En concreto, la estrategia primero determina la dirección preferente de la tendencia en las líneas semanales y diarias. El principio para determinar la dirección preferente es: si el precio de cierre de la vela actual se encuentra en el lado con un ángulo rezagado mayor en la línea del período correspondiente, se determina esa dirección de la línea del período. Luego, en el marco de 4 horas, se construye un canal A B C D, y a través de la dirección del canal y los puntos de retroceso se determinan los puntos de compra y venta, emitiendo señales de trading. Finalmente, es necesario que la dirección preferente determinada por la línea del período actual sea consistente con la dirección de la señal de trading de 4 horas; de esta forma, se filtran muchas señales falsas, mejorando la fiabilidad de las señales de trading.

Ventajas de la Estrategia

Esta estrategia tiene principalmente las siguientes ventajas:

-

Mecanismo de doble filtro basado en múltiples marcos temporales, capaz de eliminar gran parte del ruido y obtener oportunidades de trading de alta fiabilidad.

-

Utilización de un canal para determinar los puntos de compra y venta, con señales de trading claras.

-

Los puntos de retroceso de Fibonacci establecen niveles de take profit y stop loss, permitiendo una rápida toma de ganancias y detención de pérdidas.

-

La estrategia tiene pocos parámetros, lo que facilita su comprensión y dominio.

-

Buena escalabilidad, fácil de optimizar y mejorar.

Riesgos de la Estrategia

Esta estrategia presenta principalmente los siguientes riesgos:

-

Monitorear demasiados marcos temporales aumenta la complejidad y es propenso a errores.

-

No se consideran eventos especiales del mercado, como fluctuaciones bruscas causadas por noticias importantes.

-

El uso de puntos de retroceso para fijar take profit y stop loss puede resultar en ganancias insuficientes.

-

Una configuración inadecuada de parámetros puede llevar a un exceso de operaciones o a la pérdida de oportunidades.

Medidas correctivas:

-

Reforzar la supervisión de situaciones anómalas y eventos noticiosos importantes.

-

Optimizar la lógica de take profit y stop loss para asegurar que las ganancias alcancen un nivel adecuado.

-

Realizar pruebas detalladas y optimización de parámetros para reducir la probabilidad de exceso de operaciones y pérdida de señales.

Direcciones de Optimización de la Estrategia

Las principales direcciones de optimización de esta estrategia son:

-

Incorporar modelos de aprendizaje automático para determinar la dirección preferente de la tendencia, utilizando más datos para mejorar la precisión del juicio.

-

Probar otros indicadores para construir el canal y determinar los puntos de compra y venta.

-

Explorar formas más avanzadas de take profit y stop loss, como el trailing stop o el take profit escalonado.

-

Utilizar resultados de backtesting para derivar parámetros óptimos, haciendo que la configuración de parámetros se ajuste más a los principios de inversión cuantitativa.

-

Agregar mecanismos de monitoreo y respuesta ante eventos imprevistos importantes.

Conclusión

En general, la idea central de esta estrategia es una estrategia de trading cuantitativo de alta frecuencia basada en la reducción de ruido mediante doble filtro. Utiliza la determinación de múltiples marcos temporales y el método de canales para identificar puntos de compra y venta, logrando un filtrado de doble fiabilidad de las señales de trading. Al mismo tiempo, la estrategia tiene pocos parámetros, es fácil de dominar y cuenta con buena escalabilidad para su optimización y mejora. En el futuro, se optimizará en aspectos como la precisión del juicio, el método de take profit y stop loss, y la optimización de parámetros para lograr mejores resultados.

- 1