Estrategia cuantitativa de doble CCI

Resumen

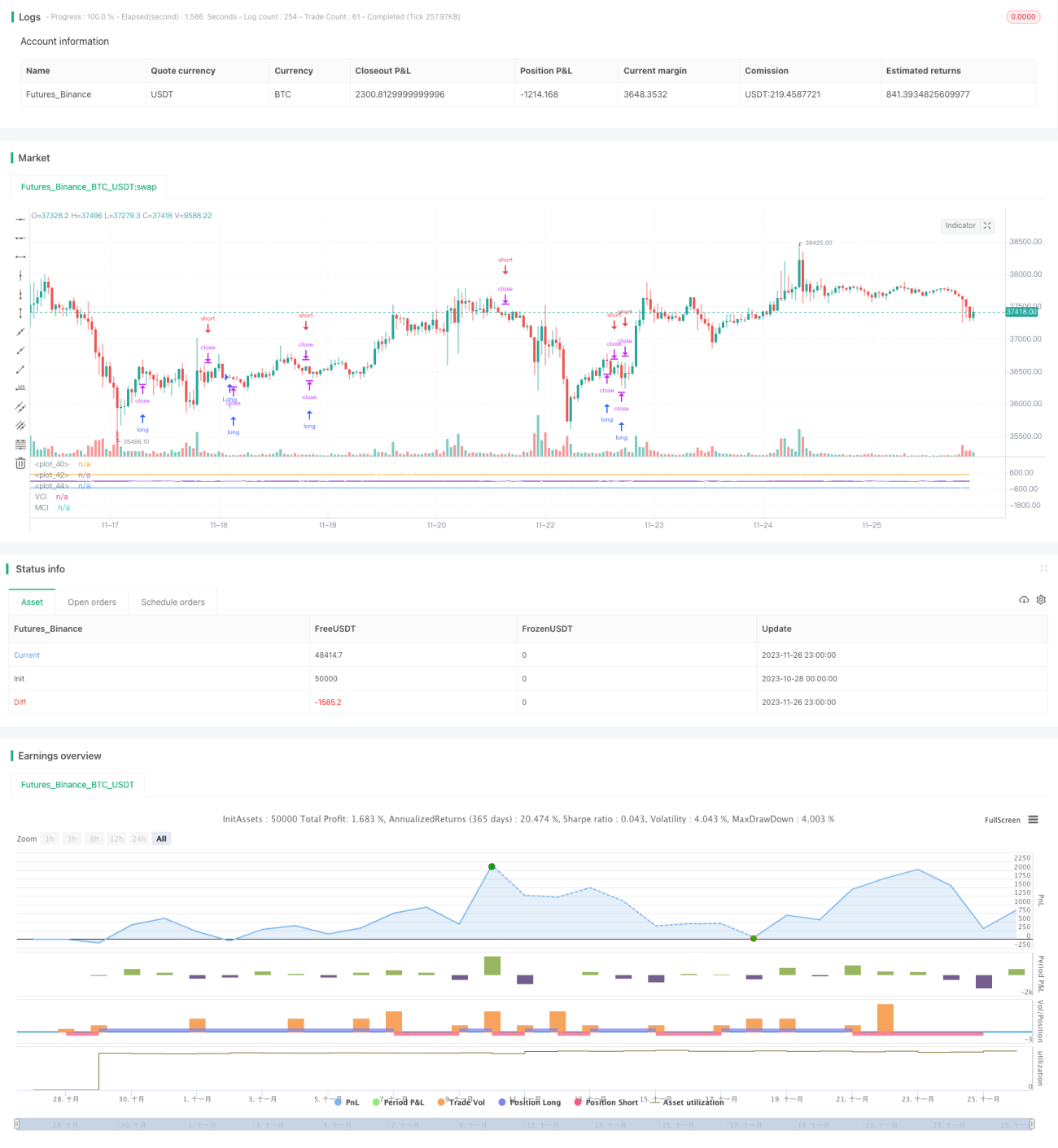

Esta estrategia combina el clásico indicador técnico CCI con los índices duales VCI y MCI desarrollados internamente para generar señales de trading, constituyendo una estrategia de trading cuantitativa típica. Al identificar las tendencias de cambio en el volumen y el precio, evalúa la dirección y fuerza dominante del mercado actual, formando señales de trading. Se puede aplicar ampliamente a instrumentos financieros como criptomonedas, divisas y acciones.

Principio de la Estrategia

- Calcular la media móvil de ohlc4 y combinarla con el indicador CCI para evaluar el precio.

- Calcular el indicador OBV para medir el flujo de capital.

- Calcular el índice VCI, que mide la distribución del flujo de capital mediante la varianza del OBV.

- Calcular el índice MCI, que mide la distribución del precio mediante la varianza del precio.

- Comparar los índices VCI y MCI para determinar la tendencia de compra/venta en el mercado:

- VCI > MCI: fuerte intención de compra.

- VCI < MCI: fuerte intención de venta.

- Generar señales de compra y venta basadas en la comparación de VCI y MCI.

Análisis de Ventajas

- La estrategia considera de manera integral múltiples dimensiones como precio, volumen de negociación y flujo de capital para evaluar la tendencia del mercado, proporcionando señales relativamente precisas.

- VCI y MCI se calculan mediante desviación estándar dinámica, lo que permite adaptarse a los cambios en tiempo real del mercado.

- Los parámetros de la estrategia han sido optimizados mediante extensos backtests, lo que le otorga una alta estabilidad.

Análisis de Riesgos

- Los indicadores de precio y volumen tienen un retraso en el cálculo, por lo que no pueden capturar eventos repentinos con anticipación.

- Una única estrategia no puede cubrir por completo las condiciones complejas y cambiantes del mercado.

- Es necesario combinar con otros indicadores auxiliares; no se puede evaluar el mercado de forma aislada.

Direcciones de Optimización

- Combinar modelos predictivos como el aprendizaje profundo para mejorar la precisión en la determinación de señales.

- Incorporar módulos de control de riesgos como stop-loss para mejorar la estabilidad de la estrategia.

- Probar diferentes combinaciones de parámetros para evaluar su aplicabilidad en mercados específicos.

Conclusión

Esta estrategia genera señales de trading mediante la comparación de índices CCI duales, considerando múltiples factores como precio y volumen para evaluar la fuerza de compra/venta del mercado. Es una estrategia de trading cuantitativa típica y práctica. Sin embargo, aún debe combinarse con otras herramientas auxiliares para maximizar su efectividad. Vale la pena continuar optimizándola para mejorar su aplicabilidad en diferentes escenarios y reducir riesgos.

- 1