Estrategia de stop loss de seguimiento de tendencia basada en TFO y ATR

Resumen

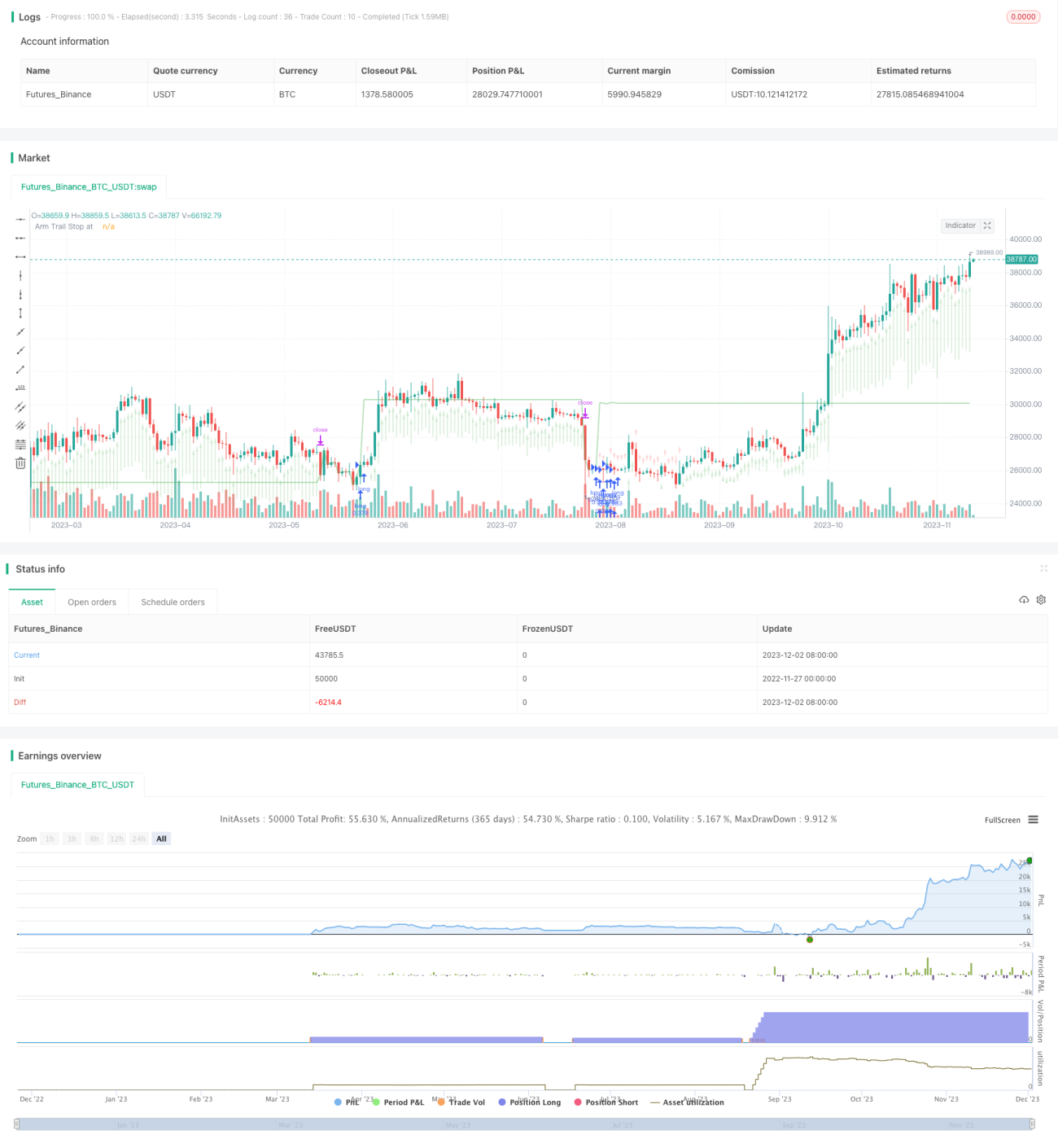

Esta estrategia es una estrategia de trailing stop basada en el Oscilador de Flexibilidad de Tendencia (Trend Flex Oscillator, TFO) del Dr. John Ehlers y el indicador de Rango Verdadero Promedio (Average True Range, ATR). Está diseñada para mercados alcistas, abriendo una posición larga cuando el precio se revierte después de una condición de sobreventa. Normalmente cierra la posición en unos pocos días, a menos que sea atrapada por un mercado bajista, en cuyo caso mantiene la posición. La estrategia ajusta parámetros configurables mediante backtesting simple, pero no se debe confiar completamente en los resultados del backtesting.

Principio de la estrategia

La estrategia combina los indicadores TFO y ATR, abriendo una posición larga cuando se cumplen las condiciones de compra, y cerrando la posición cuando se cumplen las condiciones de venta.

Condición de compra: cuando el TFO está por debajo de cierto umbral (indicando sobreventa), y el valor del TFO de la vela anterior es menor que el de la vela actual (indicando que el TFO está revertiendo al alza), y al mismo tiempo el ATR está por encima del umbral de volatilidad establecido (indicando un aumento de la volatilidad del mercado), se abren posiciones largas si se cumplen las tres condiciones.

Condición de venta: cuando el TFO está por encima de cierto umbral (indicando sobrecompra), y al mismo tiempo el ATR está por encima del umbral establecido, se cierran todas las posiciones largas si se cumple la condición. Además, la estrategia establece un trailing stop: cuando el precio cae por debajo del nivel de trailing stop definido, también se cierran todas las posiciones largas. El usuario puede elegir que la estrategia cierre según las señales del indicador o solo según el nivel de stop.

La estrategia puede abrir hasta 15 posiciones largas simultáneamente. Sus parámetros son ajustables y se adaptan a diferentes marcos temporales.

Ventajas de la estrategia

-

Combina tendencia y volatilidad para determinar la dirección del mercado, lo que resulta bastante estable. El TFO capta señales tempranas de rupturas de tendencia, mientras que el ATR aprovecha los momentos de aumento de la volatilidad.

-

Parámetros ajustables de compra, venta y stop loss, ofreciendo flexibilidad operativa. El usuario puede ajustar los parámetros según el mercado para lograr una optimización.

-

Incorpora una función de stop loss que puede reducir las pérdidas en condiciones extremas del mercado. El stop loss es un elemento muy importante en el trading cuantitativo.

-

Permite abrir posiciones adicionales y cerrar parcialmente, lo que permite ampliar las ganancias aumentando el tamaño de la posición. Adecuado para escenarios alcistas.

Riesgos de la estrategia

-

La estrategia solo opera en largo, no en corto, por lo que no puede generar ganancias en mercados bajistas. Si se encuentra con un mercado bajista severo, puede provocar pérdidas enormes.

-

Una configuración incorrecta de los parámetros puede llevar a un exceso de operaciones o a no capturar operaciones necesarias. Se requiere probar repetidamente para encontrar la mejor combinación de parámetros.

-

En condiciones extremas del mercado, el stop loss puede no ser efectivo y no impedir pérdidas masivas. Esto es un problema que enfrentan todas las estrategias de stop loss.

-

Los resultados del backtesting no reflejan completamente el trading en tiempo real; los resultados reales pueden desviarse.

Optimización de la estrategia

-

Se podría considerar agregar una línea de trailing stop a la condición de venta para que la estrategia detenga las pérdidas de manera oportuna y controle el riesgo a la baja de manera efectiva.

-

Se podría extender el mecanismo de venta en corto: abrir posiciones cortas cuando el TFO se revierte a la baja y el ATR es suficientemente grande, permitiendo que la estrategia se adapte a mercados bajistas.

-

Se podrían agregar más filtros, como cambios en el volumen, para reducir el impacto de condiciones anormales del mercado en la estrategia.

-

Se podrían probar configuraciones de parámetros y resultados de backtesting en diferentes marcos temporales para encontrar la mejor combinación de período y parámetros.

Conclusión

Esta estrategia integra las ventajas del análisis de tendencia y el monitoreo de la volatilidad, determinando la dirección del mercado mediante la combinación de los indicadores TFO y ATR. Incorpora mecanismos como apertura adicional, cierre parcial y trailing stop, lo que permite ampliar las ganancias y controlar los riesgos, siendo adecuada para mercados alcistas. Además, tiene espacio de optimización extensible: al agregar más filtros de indicadores y ajustar parámetros se puede mejorar aún más el rendimiento de la estrategia. Básicamente cumple con los requisitos funcionales de una estrategia cuantitativa, y merece un estudio y aplicación más profundos.

/*backtest

start: 2022-11-27 00:00:00

end: 2023-12-03 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Chart0bserver

//

// Open Source attributions:- 1