Estrategia de filtro de compra de doble indicador para señales de compra

Resumen

La estrategia de filtro de compra con doble indicador utiliza la combinación del índice estocástico de fuerza relativa suavizado (Stochastic RSI) y las Bandas de Bollinger para identificar oportunidades potenciales de compra. Esta estrategia emplea múltiples condiciones de filtro con el fin de distinguir los puntos de compra más rentables. Esto permite identificar momentos de compra de alta probabilidad en entornos de mercado volátiles.

Principio de la Estrategia

La estrategia utiliza dos grupos de indicadores para identificar oportunidades de compra.

En primer lugar, se usa el índice estocástico de fuerza relativa suavizado para determinar si el mercado está sobrevendido. Este indicador combina el índice estocástico y su media móvil suavizada. Cuando la línea %K cruza al alza su línea %D desde un nivel bajo, se considera una señal de sobreventa. Aquí se establece un umbral: si la línea %K está por encima de 20, se considera sobreventa.

En segundo lugar, la estrategia utiliza las Bandas de Bollinger para identificar cambios en el precio. Las Bandas de Bollinger calculan una banda superior e inferior basadas en la desviación estándar del precio. Cuando el precio se acerca a la banda inferior, se considera un estado de sobreventa. La estrategia emplea un parámetro de 2 desviaciones estándar para ampliar el rango de las bandas, filtrando así más señales falsas.

Después de obtener las señales de sobreventa de los dos indicadores anteriores, la estrategia agrega múltiples condiciones de filtro para identificar aún más los momentos de compra:

- El precio acaba de superar la banda inferior de Bollinger al alza.

- El precio de cierre actual es superior al precio de cierre de N velas atrás, lo que muestra fuerza de compra.

- El precio de cierre actual es inferior al precio de cierre de un período de retroceso a largo o mediano plazo, favoreciendo una corrección.

Cuando se identifican estas condiciones combinadas, se genera una señal de compra.

Análisis de Ventajas

Esta estrategia de filtro con doble indicador presenta varias ventajas:

- El uso de dos indicadores hace que las señales de compra sean más confiables, evitando señales falsas.

- Múltiples condiciones de filtro evitan compras frecuentes en mercados laterales.

- Combina el índice estocástico para determinar sobreventa y las Bandas de Bollinger para detectar precios anómalos.

- Añade un criterio de fuerza del precio para asegurar suficiente impulso comprador.

- Incluye un criterio de retroceso para garantizar aún más la fiabilidad del punto de compra.

En resumen, la estrategia integra múltiples indicadores técnicos y filtros, logrando una identificación más precisa y confiable de los momentos de compra, y por lo tanto un mejor rendimiento en las operaciones.

Análisis de Riesgos

A pesar de las muchas ventajas de esta estrategia de filtro con doble indicador, existen algunos riesgos que deben tenerse en cuenta:

- Una parametrización inadecuada puede generar señales de compra demasiado frecuentes o demasiado conservadoras; se requiere una cuidadosa optimización mediante pruebas.

- Múltiples condiciones de filtro pueden hacer que se pierdan algunas oportunidades de compra, impidiendo seguir mercados rápidos.

- Cuando los indicadores divergen, pueden generarse señales erróneas; es necesario prestar atención a la coherencia de los indicadores.

- No se evalúa la tendencia, por lo que en mercados bajistas podrían generarse señales falsas que lleven a pérdidas.

Para mitigar estos riesgos, la estrategia puede optimizarse de la siguiente manera:

- Ajustar los parámetros de los indicadores para equilibrar la sensibilidad de los filtros.

- Incorporar indicadores de tendencia para evitar señales falsas en mercados bajistas.

- Agregar mecanismos de stop loss.

Direcciones de Optimización

Esta estrategia de filtro con doble indicador puede optimizarse aún más en las siguientes dimensiones:

- Probar combinaciones de más indicadores técnicos para encontrar mejores formas de identificar momentos de compra, como VRSI, DMI, etc.

- Incorporar algoritmos de aprendizaje automático para optimizar los parámetros de forma automática.

- Agregar un mecanismo de stop loss adaptativo: cuando las ganancias alcancen cierto nivel, elevar gradualmente el nivel de stop loss.

- Combinar indicadores de volumen para asegurar que exista suficiente fuerza compradora.

- Optimizar la estrategia de gestión de capital, estableciendo un tamaño de operación dinámico para reducir la pérdida por operación.

Al incorporar tecnologías y métodos más avanzados, esta estrategia de filtro con doble indicador puede lograr una selección más precisa de los momentos de compra y un mejor control del riesgo, obteniendo así rentabilidades más estables y confiables en operaciones reales.

Resumen

En conclusión, la estrategia de filtro de compra con doble indicador utiliza múltiples indicadores técnicos como el Stochastic RSI y las Bandas de Bollinger, junto con varias condiciones de filtro como la fuerza del precio y el retroceso, para identificar momentos de compra de alta probabilidad y confiabilidad. Con una optimización adicional de parámetros y la configuración de stops, esta estrategia puede convertirse en una de las estrategias de trading cuantitativo de rentabilidad estable.

Su principal ventaja radica en la combinación efectiva de indicadores y condiciones de filtro, lo que hace que la identificación de los momentos de compra sea más precisa. Tanto los riesgos como las direcciones de optimización son controlables y solucionables. En general, se trata de una estrategia cuantitativa eficiente y aplicable en operaciones reales.

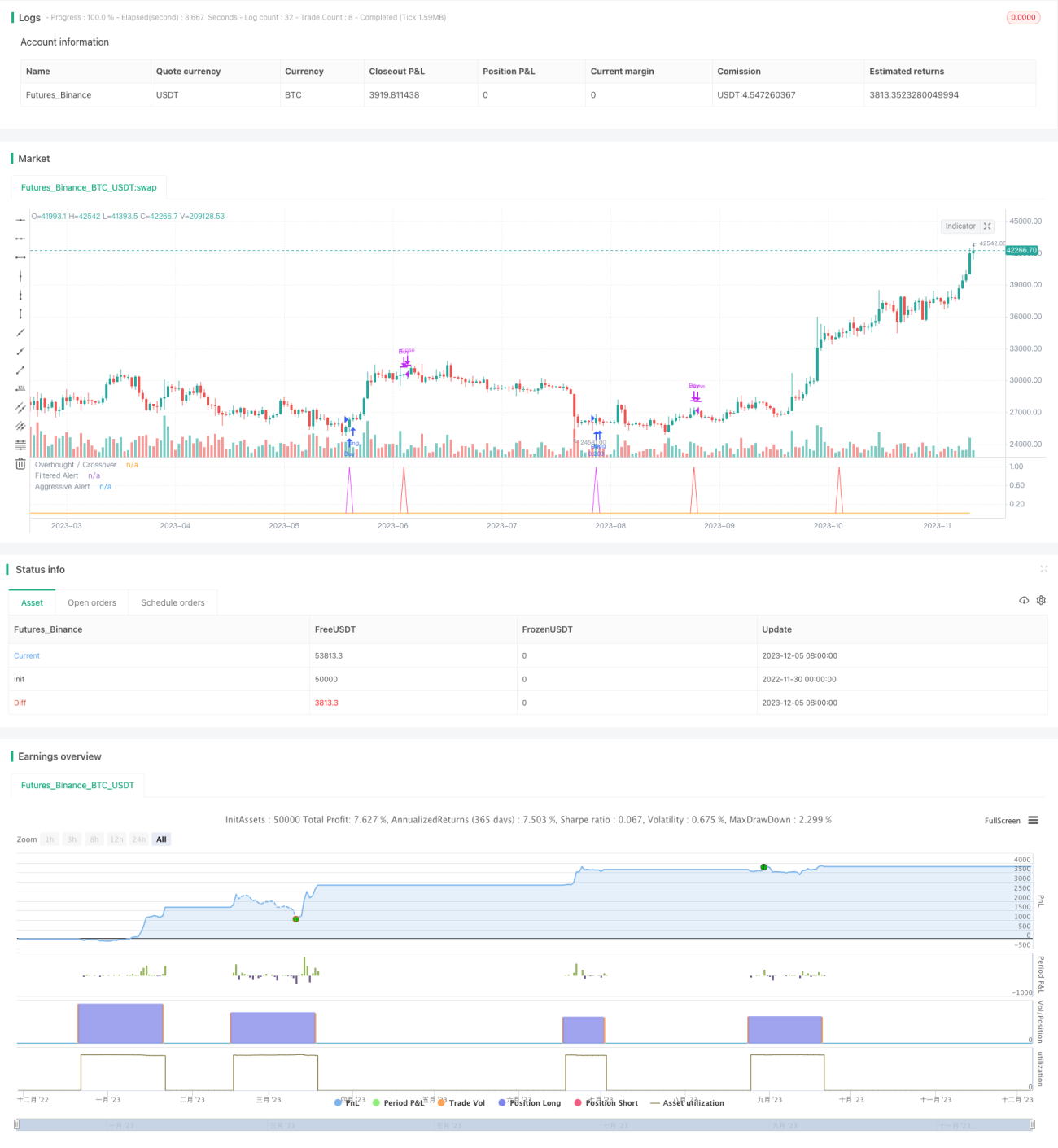

/*backtest

start: 2022-11-30 00:00:00

end: 2023-12-06 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("SORAN Buy and Close Buy", pyramiding=1, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=10, overlay=false)

////Buy and Close-Buy messages- 1