Estrategia de momentum simple basada en SMA, EMA y volumen

Resumen

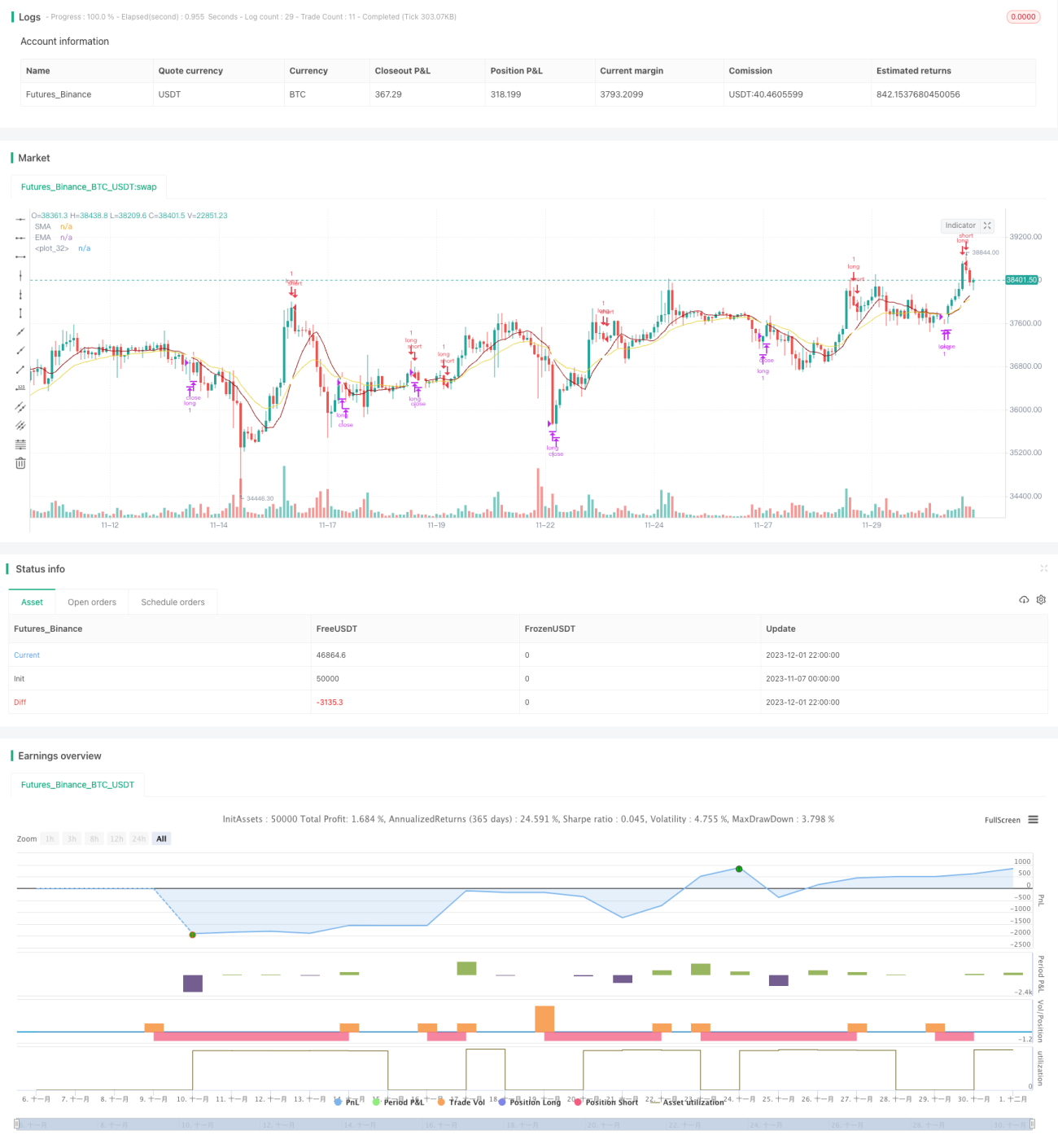

Esta estrategia es una estrategia simple de impulso intradía que solo opera en largo (sin posiciones cortas). Utiliza los indicadores SMA, EMA y volumen para intentar entrar en el mercado en el momento óptimo (cuando tanto el precio como el impulso están subiendo). Su ventaja es que es fácil de implementar y tiene cierta capacidad para identificar tendencias.

Principio de la estrategia

La lógica de generación de señales de entrada (Entry) es la siguiente: cuando el indicador SMA está por encima del EMA y se forman 3 o 4 velas consecutivas con tendencia alcista, y el mínimo de la vela intermedia es superior al precio de apertura de la vela que inició el alza, se genera una señal de entrada.

La lógica de generación de señales de salida (Exit) es: cuando el SMA cruza por debajo del EMA, se genera una señal de salida.

La estrategia solo opera en largo, no en corto. Su lógica de entrada y salida tiene cierta capacidad para identificar tendencias alcistas sostenidas.

Análisis de ventajas

Esta estrategia tiene las siguientes ventajas:

- La lógica de la estrategia es simple, fácil de entender e implementar.

- Utiliza indicadores técnicos comunes como SMA, EMA y volumen, con parámetros ajustables de forma flexible.

- Tiene cierta capacidad para identificar tendencias alcistas sostenidas, lo que permite capturar parte de las oportunidades en la tendencia.

Análisis de riesgos

Esta estrategia también presenta los siguientes riesgos:

- No puede identificar mercados a la baja o en consolidación, lo que puede generar grandes retrocesos.

- No puede aprovechar oportunidades en corto ni cubrirse contra tendencias bajistas, perdiendo posibles oportunidades de ganancias.

- El indicador de volumen no es eficaz con datos de alta frecuencia, por lo que es necesario ajustar los parámetros.

- Se puede utilizar un stop loss para controlar el riesgo.

Direcciones de optimización

Esta estrategia se puede optimizar en los siguientes aspectos:

- Agregar oportunidades de operaciones en corto para lograr operaciones bidireccionales (largo y corto), aprovechando las tendencias bajistas.

- Utilizar indicadores más avanzados como MACD, RSI, etc., en combinación para mejorar la capacidad de juicio de tendencias.

- Optimizar la lógica del stop loss para reducir el riesgo de retroceso.

- Ajustar parámetros y probar datos en diferentes períodos para encontrar la mejor combinación de parámetros.

Resumen

En general, esta estrategia es una estrategia de seguimiento de tendencias muy simple que juzga el momento de entrada mediante los indicadores SMA, EMA y volumen. Su ventaja es la simplicidad y facilidad de implementación, adecuada para el aprendizaje inicial, pero no puede identificar tendencias de consolidación o bajista, por lo que conlleva ciertos riesgos. Se puede mejorar introduciendo operaciones en corto, optimizando indicadores y stop loss, entre otros métodos.

- 1