Estrategia de filtrado de corrección de índices

Resumen

Esta estrategia utiliza una combinación de operaciones de módulo y medias móviles exponenciales (EMA) para implementar un filtro de tendencia con un fuerte componente aleatorio, utilizado para determinar la dirección de la posición. La estrategia primero calcula si el resto de dividir el precio entre un número establecido es 0; si es así, se genera una señal de trading. Si esta señal está por debajo de la media móvil exponencial, se abre una posición corta; si está por encima, se abre una posición larga. La estrategia combina la aleatoriedad de las operaciones matemáticas con la identificación de tendencias de los indicadores técnicos, utilizando la validación cruzada entre indicadores de diferentes períodos para filtrar eficazmente parte del ruido aleatorio que impacta el precio.

Principio de la Estrategia

- Se establece el valor de entrada del precio

acomo el precio de cierre (close), que puede modificarse; se establece el valor del divisorben 4, que también puede modificarse. - Se calcula el resto

modulode dividiraentreby se verifica si es igual a 0. - Se establece la longitud de la media móvil exponencial

MALen, por defecto de 70 períodos, como indicador de tendencia a medio-largo plazo. - Cuando el resto

moduloes 0, se genera una señal de trading (evennumber). La relación con la EMA determina la dirección. Cuando el precio cruza por encima de la EMA, se genera una señal de compra (BUY); cuando cruza por debajo, una señal de venta (SELL). - Las entradas se realizan en la dirección de la señal, ya sea larga o corta. La estrategia puede restringir la apertura de posiciones en dirección opuesta para controlar el número de operaciones.

- Las condiciones de stop loss se establecen según tres métodos: stop loss fijo, stop loss con ATR, stop loss basado en el rango de fluctuación del precio. La condición de take profit es la inversa del stop loss.

- Se puede optar por usar un stop loss móvil para asegurar más ganancias; por defecto no se utiliza.

Análisis de Ventajas

- La aleatoriedad de la operación de módulo evita verse afectada por las oscilaciones del precio, y combinada con la identificación de tendencia de la media móvil, puede filtrar eficazmente señales no válidas.

- La media móvil exponencial actúa como indicador de tendencia a medio-largo plazo, y al combinarse con las señales a corto plazo de la operación de módulo, se logra una validación multicapa que evita señales falsas.

- Los parámetros personalizables son muy flexibles, permitiendo ajustarlos según diferentes mercados para encontrar la mejor combinación.

- Integra múltiples métodos de stop loss para controlar el riesgo, y establece condiciones de take profit para asegurar ganancias.

- Permite abrir posiciones en dirección opuesta directamente, facilitando un cambio fluido de dirección de la posición. También se puede desactivar esta función para reducir el número de operaciones.

Análisis de Riesgos

- Una configuración inadecuada de los parámetros puede generar demasiadas señales de trading, aumentando la frecuencia de operaciones y los costos de deslizamiento.

- La media móvil exponencial como único indicador de tendencia puede generar retrasos, perdiendo el momento de reversión del precio.

- El stop loss fijo puede ser demasiado mecánico, sin capacidad de ajustarse a la volatilidad del mercado.

- La apertura directa de posiciones en dirección opuesta aumenta la frecuencia de ajuste de posiciones, incrementando los costos de trading y el riesgo.

Direcciones de Optimización

- Se pueden probar diferentes indicadores de media móvil en lugar de la EMA, o combinar la EMA con otras medias móviles, para ver si se mejora la tasa de ganancias.

- Se puede intentar combinar el filtro de módulo con otras estrategias, como Bandas de Bollinger, patrones de velas, etc., para formar un filtro más estable.

- Se puede investigar un método de stop loss adaptativo que ajuste la distancia del stop loss según el nivel de volatilidad del mercado.

- Se puede establecer un límite en el número de operaciones o un umbral de ganancias/pérdidas para restringir la frecuencia de apertura de posiciones en dirección opuesta.

Resumen

Esta estrategia logra una combinación efectiva entre el filtro aleatorio de la operación de módulo y la identificación de tendencia de la media móvil. Los parámetros son flexibles, permitiendo ajustes y optimizaciones según diferentes entornos de mercado, obteniendo así señales de trading más confiables. Además, integra múltiples mecanismos de stop loss para controlar el riesgo, así como take profit y stop loss móvil para asegurar ganancias. En general, la estrategia tiene una lógica clara, es fácil de entender y modificar, y merece más pruebas y optimizaciones, con un gran potencial para aplicación en trading real.

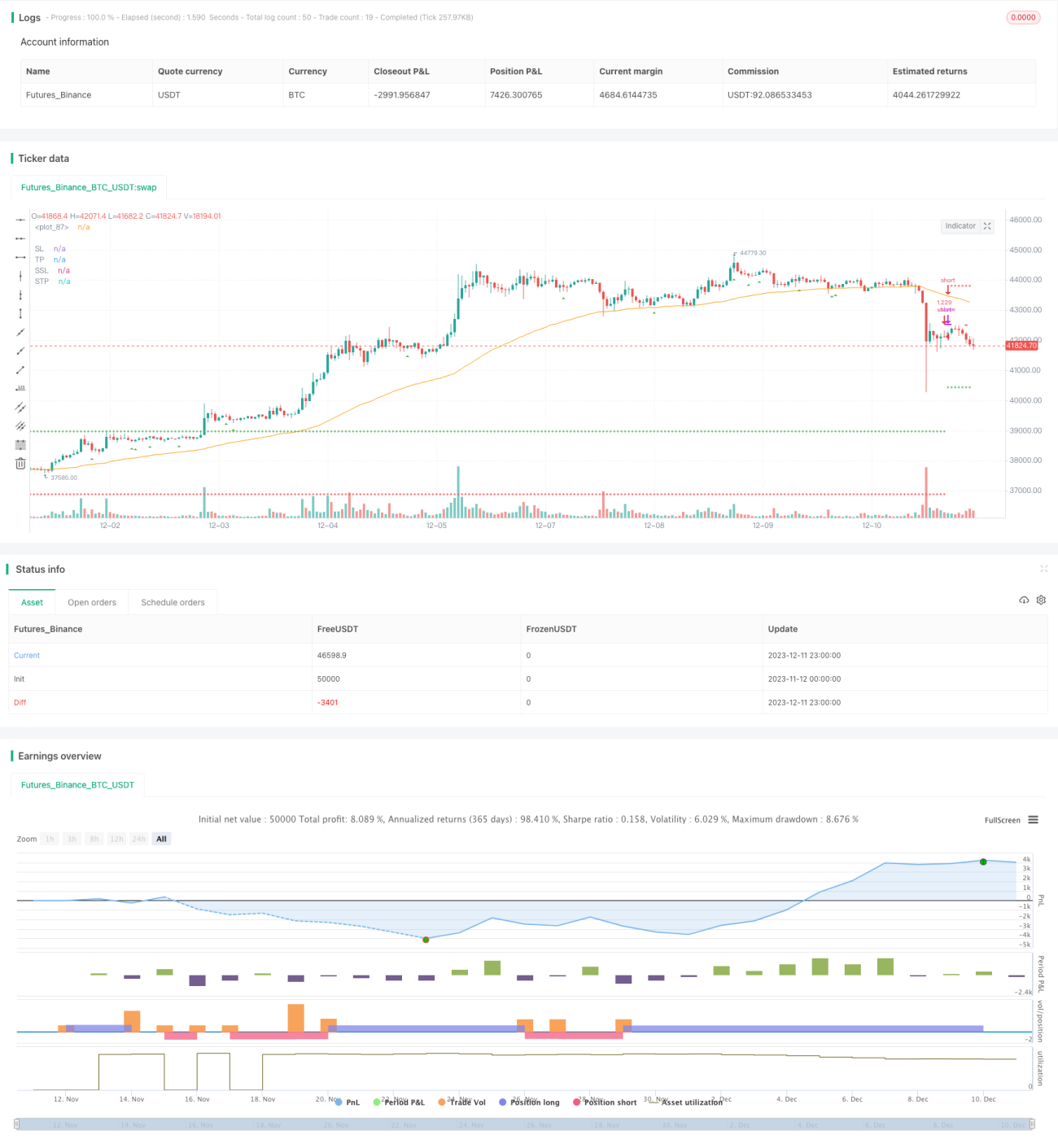

/*backtest

start: 2023-11-12 00:00:00

end: 2023-12-12 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © tweakerID

// To understand this strategy first we need to look into the Modulo (%) operator. The modulo returns the remainder numerator - 1