Estrategia de seguimiento de tendencia con la combinación del indicador estocástico modificado y mejorado en múltiples marcos temporales y la SMA

Resumen

Esta estrategia utiliza la combinación clásica del indicador Stochastic y el indicador SMA para lograr una fuerte capacidad de seguimiento de tendencias. La idea central de la estrategia es utilizar el indicador Stochastic para identificar señales de dirección de tendencia, combinarlo con el indicador SMA para filtrar y mejorar la calidad de las señales, y ajustar los parámetros del indicador mediante diferentes modos de riesgo para lograr un ajuste dinámico entre riesgo y rentabilidad. Además, la estrategia utiliza un juicio de múltiples marcos temporales para optimizar la selección del momento de entrada.

Principio de la estrategia

- La estrategia utiliza una versión mejorada del indicador Stochastic, con parámetros que incluyen el período %K, el período de suavizado de %K y el período de suavizado de %D, controlando la sensibilidad del indicador mediante el ajuste de parámetros.

- Los parámetros del indicador SMA incluyen la SMA de máximos y la SMA de mínimos, que se utilizan para filtrar señales, mejorar la calidad de las señales y evitar falsas rupturas.

- Según las preferencias de riesgo, la estrategia ofrece opciones de modo de bajo riesgo, modo de riesgo medio y modo de alto riesgo. El modo de riesgo afecta los parámetros de cruce del indicador Stochastic, logrando así un ajuste dinámico entre riesgo y rentabilidad.

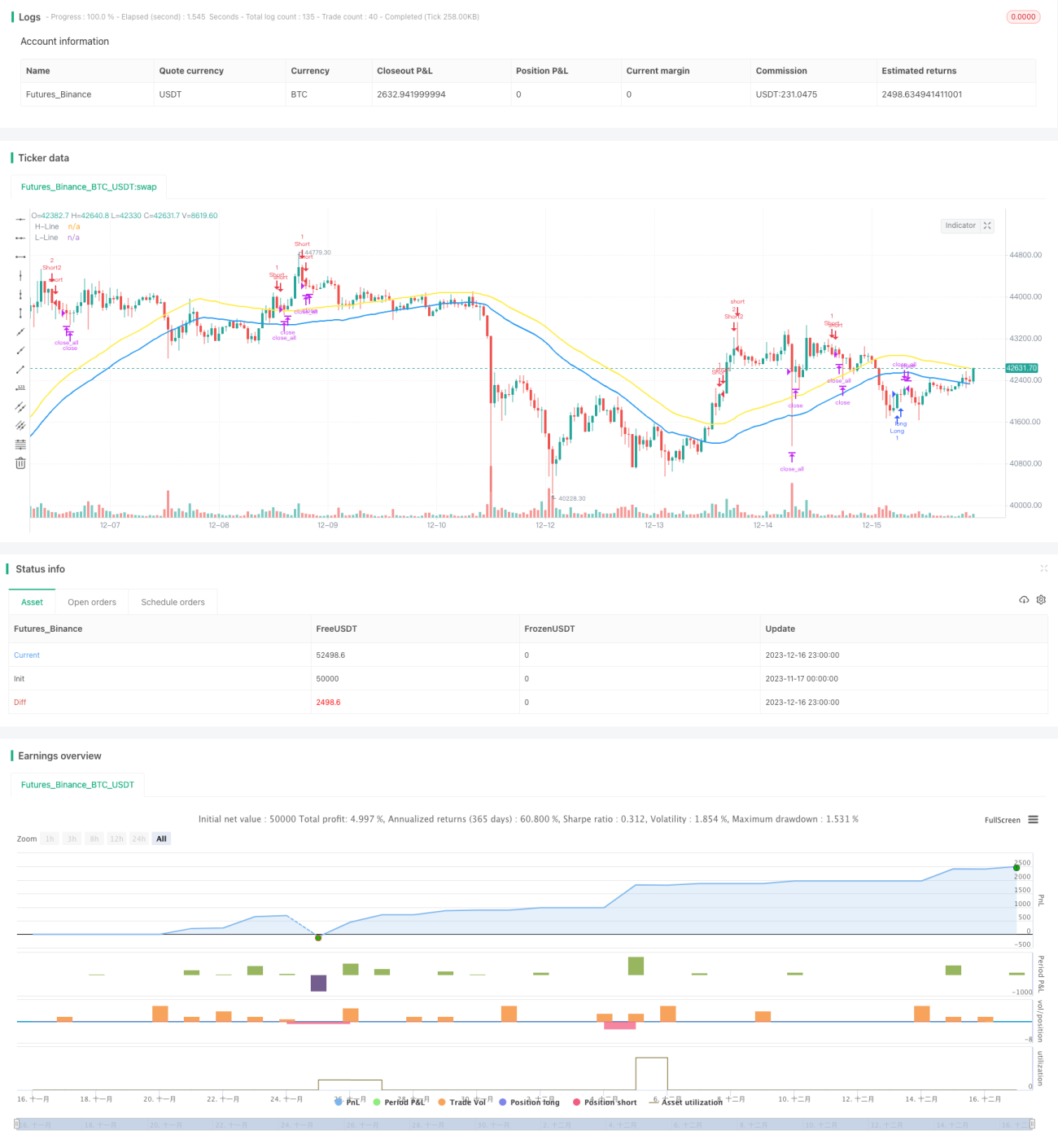

- La estrategia determina una señal de posición larga cuando el indicador Stochastic cruza por encima del umbral y el precio de cierre está por debajo de la SMA de mínimos; determina una señal de posición corta cuando el indicador Stochastic cruza por debajo del umbral y el precio de cierre está por encima de la SMA de máximos.

- La estrategia introduce un módulo de juicio de múltiples marcos temporales para verificar señales en diferentes rangos de tiempo y seleccionar un mejor momento de entrada, con el fin de controlar el riesgo de las operaciones.

Ventajas de la estrategia

- Utiliza una versión mejorada del indicador Stochastic, aumentando la sensibilidad del indicador para capturar rápidamente los cambios del mercado.

- Añade un mecanismo de filtro de doble banda SMA, que puede filtrar eficazmente señales falsas y mejorar la calidad de las señales.

- Ofrece múltiples modos de riesgo para elegir, permitiendo a los usuarios ajustar los parámetros de manera flexible según sus preferencias de riesgo.

- Añade un módulo de juicio de múltiples marcos temporales para optimizar la selección del momento de entrada y reducir el riesgo de las operaciones.

- La configuración de los parámetros de la estrategia es razonable, el uso de los indicadores es natural, el marco general es científico y riguroso, con buena estabilidad y fuerte adaptabilidad.

Riesgos de la estrategia

- La estrategia en sí misma no cuenta con un mecanismo de stop loss; es necesario establecer manualmente un nivel de stop loss para controlar el riesgo de pérdidas.

- Las señales de la estrategia son frecuentes, lo que puede provocar un exceso de operaciones y aumentar los costos de transacción.

- La estrategia es sensible a los parámetros y a la configuración del modo de riesgo; es necesario realizar pruebas y optimizaciones para encontrar los mejores parámetros.

- El drawdown de la estrategia puede ser grande; no es adecuada para operar con toda la posición, por lo que se debe controlar el tamaño del capital de trading.

Métodos correspondientes:

- Establecer un porcentaje de stop loss razonable según la volatilidad del mercado para controlar al máximo las pérdidas.

- Ajustar adecuadamente los parámetros del indicador Stochastic para reducir la frecuencia de las señales. O establecer un take profit mínimo para reducir operaciones innecesarias.

- Se recomienda seleccionar el modo de bajo riesgo por defecto y ajustar otros parámetros según los datos de backtesting.

- Controlar el tamaño de la posición, abrir posiciones en lotes para reducir el riesgo de cada operación individual.

Direcciones de optimización de la estrategia

- Realizar pruebas exhaustivas de los parámetros del indicador Stochastic y del indicador SMA para encontrar la combinación óptima de parámetros.

- Aumentar la cantidad de marcos temporales múltiples para enriquecer las bases de juicio y optimizar la selección del momento de entrada.

- Introducir combinaciones de indicadores de stop loss, como el stop loss basado en ATR, que puede seguir dinámicamente el nivel de stop loss y reducir el riesgo.

- Construir mecanismos de filtrado y confirmación de señales de indicadores, como agregar el juicio del indicador de volumen para evitar quedar atrapado.

- Agregar un módulo de gestión de posiciones para ajustar activamente el tamaño de la posición según las condiciones del mercado, reduciendo el riesgo de cada operación individual.

Conclusión

Esta estrategia combina las ventajas del indicador Stochastic y el indicador SMA para lograr un fuerte efecto de seguimiento de tendencias. El marco de la estrategia es razonable, el uso de los indicadores es natural, y al controlar los parámetros y el modo de riesgo se restaura la esencia del indicador, optimizando la estabilidad de la estrategia. El módulo de juicio de múltiples marcos temporales también mejora la adaptabilidad de la estrategia, permitiendo ajustes según diferentes instrumentos y períodos. En general, esta estrategia tiene una buena universalidad y también ofrece un gran espacio para la optimización, lo que merece una investigación más profunda.

- 1