Estrategia de media móvil suavizada estocástica de momentum

Resumen

Esta estrategia combina la Media Móvil Exponencial (EMA) con el Oscilador Estocástico (Stochastic Oscillator), adoptando un enfoque de seguimiento de tendencia y continuación, además de contar con algunas funcionalidades interesantes. La diseñé específicamente para operar con altcoins, pero también funciona para Bitcoin y algunos pares de Forex.

Principio de la Estrategia

La estrategia tiene 4 condiciones necesarias para generar una señal de entrada. A continuación se muestran las condiciones para abrir una operación larga (las señales de cierre son las opuestas):

- La EMA rápida está por encima de la EMA lenta.

- La línea K del estocástico se encuentra en zona de sobrecompra.

- La línea K del estocástico cruza por encima de la línea D del estocástico.

- El precio cierra entre la EMA lenta y la EMA rápida.

Una vez que todas las condiciones son verdaderas, se abre una posición al inicio de la siguiente vela.

Análisis de Ventajas

Esta estrategia combina las fortalezas de la EMA y el oscilador estocástico para capturar eficazmente el inicio y la continuación de las tendencias, siendo adecuada para operaciones de mediano y largo plazo. Además, la estrategia ofrece múltiples parámetros personalizables, permitiendo al usuario ajustarlos según su estilo de trading y las características del mercado.

Específicamente, las ventajas son:

- El cruce de EMAs determina la dirección de la tendencia, aumentando la estabilidad y fiabilidad de las señales.

- El oscilador estocástico identifica condiciones de sobrecompra/sobreventa para buscar oportunidades de reversión.

- Combina ambos indicadores, ofreciendo tanto seguimiento de tendencia como trading en contra de la misma.

- El ATR calcula automáticamente la distancia del stop loss, ajustándose a la volatilidad del mercado.

- Relación riesgo-recompensa personalizable para satisfacer diferentes necesidades.

- Parámetros personalizables para adaptarse a diferentes mercados.

Análisis de Riesgos

Los principales riesgos de esta estrategia provienen de:

- Los cruces de EMA pueden generar señales falsas (falsos rompimientos).

- El oscilador estocástico tiene un retraso inherente, lo que puede hacer que se pierda el punto óptimo de reversión del precio.

- Una sola estrategia no puede adaptarse completamente a entornos de mercado cambiantes.

Para mitigar estos riesgos, se pueden tomar las siguientes medidas:

- Ajustar adecuadamente los períodos de la EMA para reducir señales falsas.

- Combinar más indicadores para juzgar la tendencia y los niveles de soporte/resistencia, asegurando la fiabilidad de las señales.

- Establecer una estrategia clara de gestión de capital para controlar la exposición al riesgo en cada operación.

- Adoptar una estrategia compuesta, donde diferentes estrategias puedan validar las señales mutuamente, mejorando la estabilidad.

Direcciones de Optimización

Esta estrategia puede optimizarse en los siguientes aspectos:

- Agregar un módulo de ajuste de posición basado en la volatilidad. Cuando la volatilidad del mercado aumenta, reducir el tamaño de la posición; cuando disminuye, se puede aumentar.

- Incorporar el análisis de tendencias de mayor temporalidad para evitar operar en contra de la tendencia. Por ejemplo, combinar velas diarias o semanales para determinar la dirección.

- Agregar modelos de aprendizaje automático para evaluar señales de compra/venta. Se puede entrenar un modelo de clasificación con datos históricos para ayudar a generar señales.

- Optimizar el módulo de gestión de capital para que el stop loss y el tamaño de la posición sean más inteligentes.

Conclusión

Esta estrategia integra las ventajas del seguimiento de tendencia y las operaciones de reversión, considerando tanto el contexto del mercado a gran escala como la acción del precio actual. Es una estrategia efectiva que vale la pena seguir en operaciones reales a largo plazo. Mediante la optimización continua de los parámetros, la adición de módulos de evaluación de tendencias y otros medios, el rendimiento de la estrategia aún tiene un gran margen de mejora, mereciendo una mayor inversión en I+D.

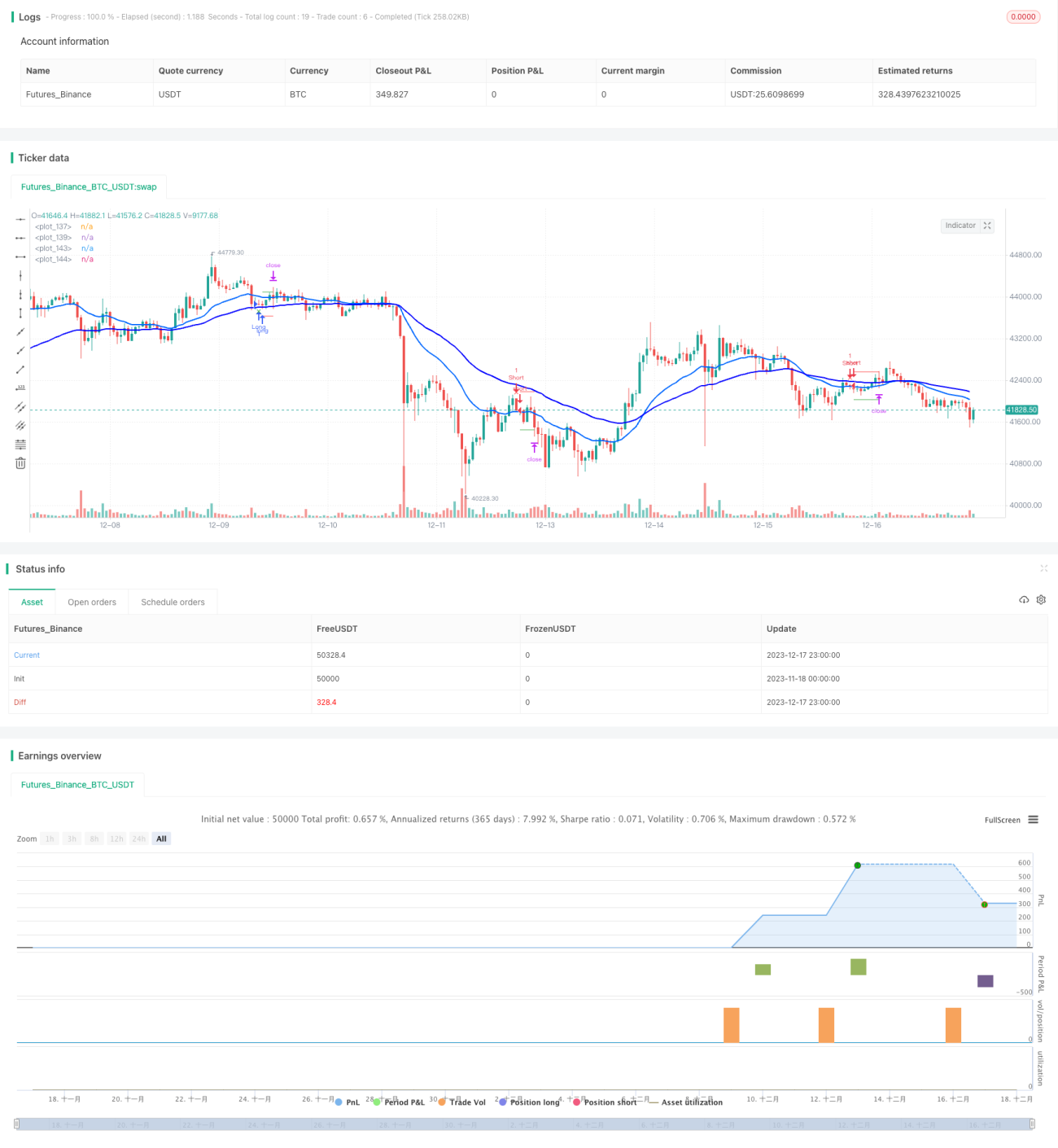

/*backtest

start: 2023-11-18 00:00:00

end: 2023-12-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © LucasVivien

// Since this Strategy may have its stop loss hit within the opening candle, consider turning on 'Recalculate : After Order is filled' in the strategy settings, in the "Properties" tabs- 1