Indicador RSI combinado con estrategia de trading de bandas de Bollinger

Una visión general de la estrategia

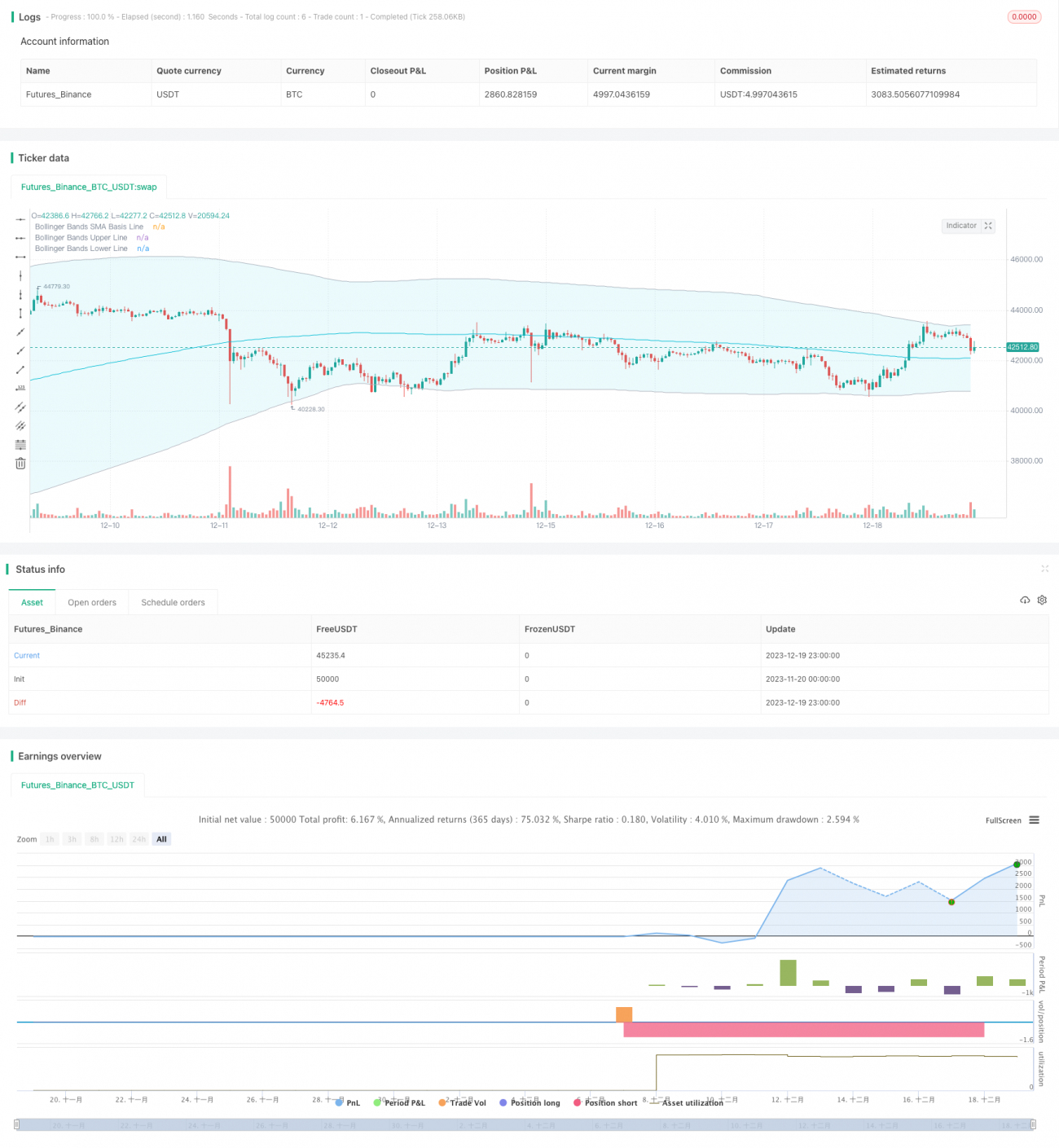

Esta estrategia se llama estrategia de parada de pérdidas de la banda de Bollinger RSI (RSI Bollinger Bands TP/SL Strategy). Esta estrategia combina el indicador RSI con el indicador de la banda de Bollinger para posicionar la tendencia y realizar operaciones de ruptura.

2. Principios de estrategia

1. El índice RSI dice que ha invertido

El indicador RSI puede determinar si una acción está en el rango de sobreventa cuando el RSI es mayor que la línea de sobreventa establecida y es sobreventa cuando es menor que la línea de sobreventa establecida. Esta estrategia establece la línea de sobreventa en 50 y la línea de sobreventa en 50.

2. Tendencia a juzgar con el brote.

La banda de Bryn se obtiene calculando la diferencia estándar del precio de la acción. La línea de resistencia es la línea de resistencia y la línea de apoyo es la línea de apoyo.

3. El RSI se combina con el indicador de las Bandas de Brin

Cuando el indicador RSI aparece una señal de inversión inferior, mientras que el precio de las acciones rompe la banda de Brin hacia abajo, considere que el movimiento se invierte de abajo hacia arriba, haga más; cuando el indicador RSI aparece una señal de inversión superior, mientras que el precio de las acciones cae por encima de la banda de Brin, considere que el movimiento se invierte de arriba hacia abajo, haga un vacío.

Tres, las ventajas estratégicas.

1. El filtro de doble indicador aumenta la precisión de la señal

El indicador RSI y el indicador de las bandas de Brin se utilizan para determinar tendencias y puntos de reversión. El uso de ambos en combinación puede mejorar la precisión de identificación de señales de compra y venta reales y evitar falsas rupturas.

2. El control de riesgos del mecanismo de parada de pérdidas

La estrategia establece un punto de parada para detener la pérdida, haciendo un punto de parada adicional como precio de entradaEl precio de entrada es el punto de parada.(1- Proporción de Stop Loss); por el contrario, el shorting puede bloquear ganancias, evitar pérdidas al máximo y controlar el riesgo.

3. Dirección de compra y venta personalizada

La estrategia puede ser solo de largo plazo, solo de corto plazo o bidireccional, y los usuarios pueden elegir diferentes direcciones según el entorno del mercado, controlando el riesgo de manera flexible.

Cuatro, los riesgos estratégicos

1. Las bandas de Bryn son sensibles a los parámetros

El tamaño estándar de la banda de Brin influye en el ancho de la banda de Brin, lo que afecta a la generación de señales de transacción. Si los parámetros no se ajustan correctamente, puede generar una gran cantidad de señales erróneas.

2. Riesgos de las pérdidas por frenado

En caso de una reversión de tipo V, la configuración de stop-loss puede ser demasiado radical y causar pérdidas innecesarias.

3. El RSI es sensible

Los parámetros del RSI también afectan a la forma de la curva RSI. Si los parámetros del RSI se establecen incorrectamente, la precisión de la señal de inversión del RSI disminuye.

Cinco, el mejoramiento de la estrategia

1. Optimización de los parámetros RSI

Se pueden probar más parámetros de longitud RSI para encontrar la combinación de parámetros óptima.

2. Optimización de los parámetros de las bandas de Bryn

Se pueden probar más longitudes de banda de Brin y parámetros de diferencia estándar para encontrar la combinación óptima de parámetros.

3. Prueba de diferentes proporciones de pérdida de frenado

Se puede encontrar el parámetro óptimo para el Stop Loss Ratio a través de la retroalimentación.

VI. Conclusión

Esta estrategia utiliza el indicador RSI y el indicador de la banda de Brin para evaluar la tendencia y la reversión, y se agrega el control de riesgo del mecanismo de stop-loss, que puede identificar automáticamente los puntos de compra y venta y detener el stop-loss a tiempo. La estrategia también tiene ciertos riesgos, y se puede mejorar principalmente mediante métodos como la optimización de parámetros.

- 1