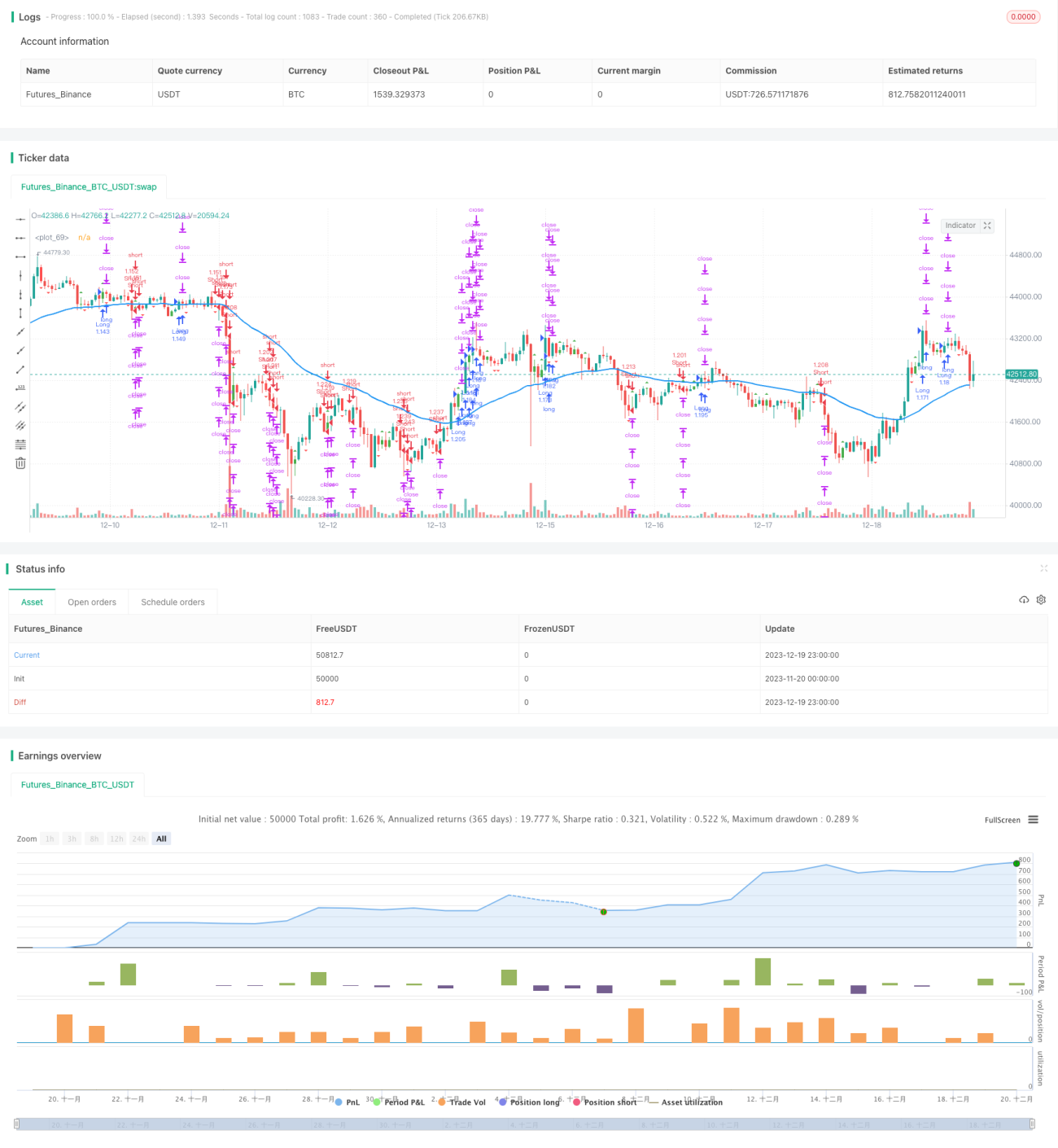

Estrategia de trading cuantitativa automática basada en barras internas y medias móviles.

Resumen

El núcleo de esta estrategia combina el patrón de barra interior (inside bar) con indicadores de media móvil para lograr trading automatizado. Cuando aparece un patrón de barra interior, indica que la tendencia actual podría revertirse, y en ese momento utilizamos la posición de la media móvil para determinar la dirección final de la operación.

Principio de la estrategia

-

Identificar el patrón de barra interior. El patrón de barra interior se produce cuando el máximo y el mínimo de una vela se encuentran dentro del cuerpo de la vela anterior. Según el color del cuerpo, podemos determinar si la barra interior es alcista o bajista.

-

Evaluar la posición de la media móvil. Cuando se encuentra una barra interior, si el precio está por encima de la media móvil, es una señal alcista; si está por debajo, es una señal bajista.

-

Combinar el patrón de barra interior con la señal de la media móvil para obtener la dirección final de la operación. Es decir, se vende cuando una barra interior bajista rompe por debajo de la media móvil, y se compra cuando una barra interior alcista rompe por encima de la media móvil.

Ventajas de la estrategia

-

Combina indicadores técnicos y patrones de precios para mejorar la precisión de las decisiones comerciales.

-

El patrón de barra interior en sí mismo contiene una fuerte señal de reversión de precios, que permite anticipar puntos de inflexión en la tendencia.

-

La media móvil filtra parte del ruido, evitando quedar atrapado en rangos laterales.

-

Implementa trading totalmente automatizado, reduciendo significativamente el tiempo y el costo de esfuerzo del trading manual.

Riesgos de la estrategia y soluciones

-

Cuando el precio oscila cerca de la media móvil, pueden aparecer muchas señales falsas, lo que lleva a un exceso de operaciones. Esto puede reducirse optimizando los parámetros de la media móvil o agregando filtros adicionales.

-

La estrategia funciona mejor en mercados con tendencias claras; en mercados laterales su rendimiento puede verse afectado. Se puede añadir un indicador de tendencia como ADX para controlar la activación del algoritmo.

-

Existe cierto rezago temporal. Se puede acortar el período o mejorar la forma de calcular la media móvil para reducir el retraso.

-

El riesgo de drawdown puede ser alto. Se pueden establecer stops de pérdidas para controlar el riesgo y ajustar la gestión de posiciones para reducir el drawdown.

Direcciones de mejora de la estrategia

-

Optimizar el período de detección de la barra interior para encontrar la mejor combinación de parámetros.

-

Probar diferentes tipos de medias móviles, como EMA, SMA, etc., para determinar la más adecuada.

-

Agregar indicadores auxiliares como MACD, KDJ, etc., para enriquecer los criterios alcistas y bajistas y mejorar la precisión de las señales.

-

Incorporar filtros como ADX, ATR, etc., para controlar el entorno en que se ejecuta el algoritmo, evitando operar en condiciones desfavorables.

-

Optimizar la estrategia de gestión de posiciones, como el control del riesgo por posición o la recuperación de pérdidas, para controlar el riesgo y buscar mayores rendimientos.

Resumen

Esta estrategia logra un plan de trading cuantitativo totalmente automatizado mediante el seguimiento dinámico de las señales de barra interior y la media móvil. La generación de señales es simple y clara, fácil de entender y seguir. Funciona notablemente bien en mercados con tendencias claras. Mediante una mayor optimización de parámetros y reglas, se puede mejorar aún más la estabilidad y rentabilidad de la estrategia.

- 1