Estrategia de robot escalable personalizada con MACD y MFI de HTF no repintante

Resumen

Esta estrategia es una combinación altamente personalizable de los indicadores MACD y MFI que no se repintan, diseñada para robots de trading algorítmico. Combina indicadores de tendencia y de momento, generando señales de trading a través de múltiples filtros.

Principio de la Estrategia

La estrategia utiliza el indicador MACD para determinar la dirección de la tendencia del mercado. El MACD es un indicador de momento de seguimiento de tendencia, que se obtiene restando una media móvil lenta de una media móvil rápida para formar el histograma MACD, y luego utilizando una media móvil exponencial del MACD para obtener la línea de señal. Cuando la línea rápida cruza por encima de la línea lenta, es una señal de compra; cuando cruza por debajo, es una señal de venta.

Además, la estrategia también utiliza el indicador MFI para evaluar las condiciones de sobrecompra y sobreventa del mercado. El MFI combina información de precio y volumen, oscilando entre 0 y 100. Valores por debajo de 20 indican zona de sobreventa, mientras que por encima de 80 indican zona de sobrecompra.

Para filtrar señales falsas, la estrategia incorpora un filtro de tendencia y un filtro RSI. Se genera una señal de compra cuando el precio está en una tendencia alcista y el RSI es inferior a un umbral establecido.

Ventajas de la Estrategia

- Combina múltiples indicadores para evaluar de forma integral el estado del mercado, mejorando la tasa de aciertos.

- Incorpora mecanismos de filtro para evitar señales falsas y reducir operaciones innecesarias.

- Parámetros y filtros totalmente personalizables, adaptables a diferentes activos y preferencias de trading.

- Puede utilizarse tanto para trading manual como para conectarse a robots algorítmicos para trading programático.

Riesgos y Soluciones

-

Una configuración inadecuada de los parámetros de los indicadores puede generar señales falsas.

-

Se pueden probar diferentes parámetros para seleccionar la combinación óptima.

-

Los parámetros no son universales entre distintos activos; requieren pruebas y optimización individuales.

-

La frecuencia de trading puede ser demasiado alta, aumentando los costos de transacción y el riesgo de deslizamiento.

-

Se pueden ajustar los filtros para reducir la frecuencia de trading.

-

En operativa real, prestar atención al control de costos.

Direcciones de Optimización

- Probar períodos de datos más largos para evaluar la estabilidad de los parámetros.

- Experimentar con diferentes combinaciones de parámetros de los indicadores.

- Optimizar los pesos de los indicadores para mejorar la estabilidad de la estrategia.

- Incorporar más filtros para reducir operaciones innecesarias.

Conclusión

Esta estrategia es un sistema de seguimiento de tendencia altamente personalizable que combina indicadores de tendencia y momento para evaluar el estado del mercado, utilizando eficazmente mecanismos de filtro para controlar el riesgo. Puede utilizarse para trading manual o conectarse a robots algorítmicos para lograr una automatización de alto nivel. Es un sistema de estrategia que merece un seguimiento y optimización a largo plazo.

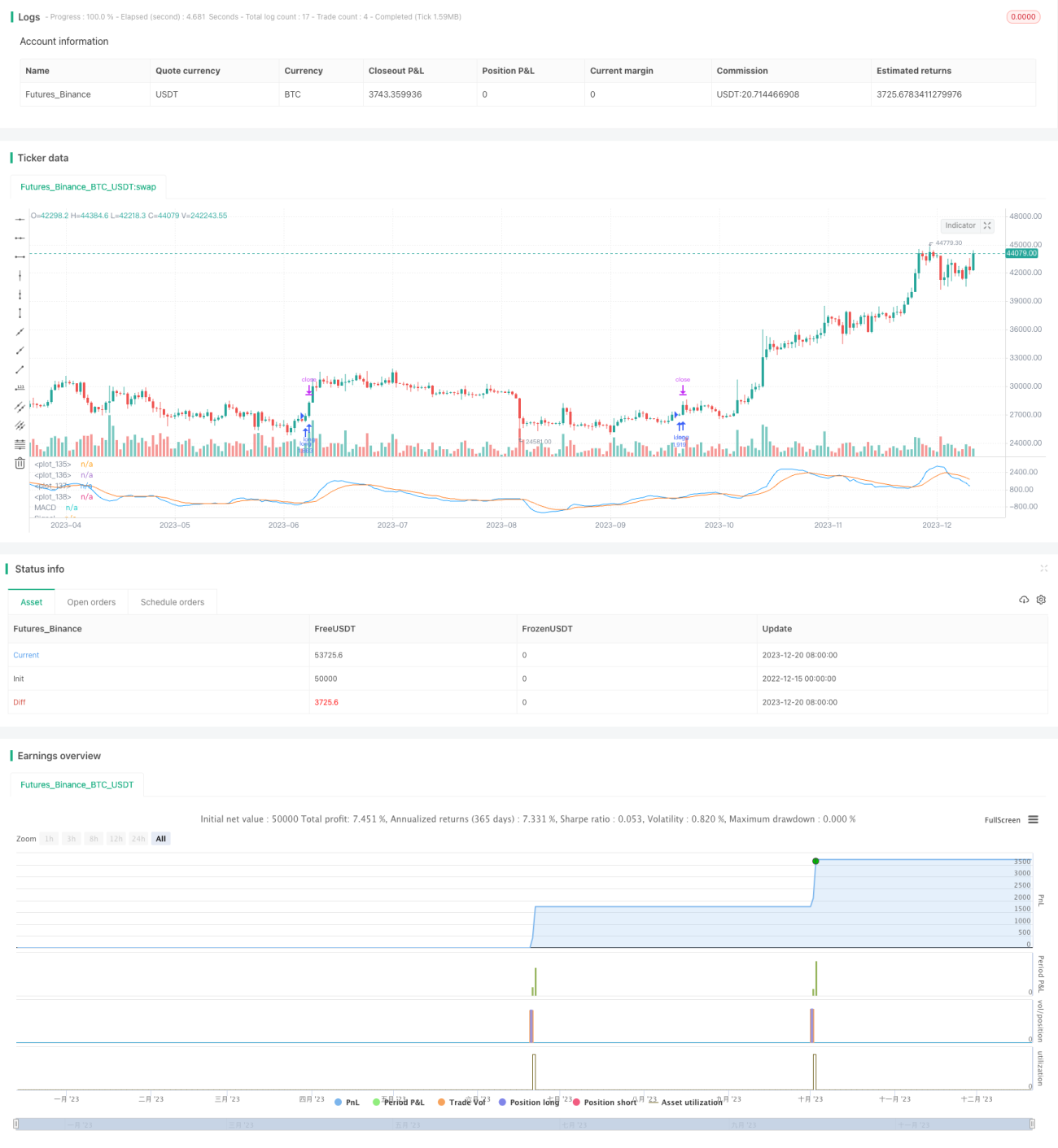

/*backtest

start: 2022-12-15 00:00:00

end: 2023-12-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//(c) Wunderbit Trading

//Modified by Mauricio Zuniga - Trade at your own risk

//This script was originally shared on Wunderbit website as a free open source script for the community. (https://help.wundertrading.com/en/articles/5246468-macd-mfi-trading-bot-for-ftx)

// - 1