Estrategia de ruptura por volatilidad del volumen dinámico de compra y venta

Resumen

Esta estrategia utiliza el volumen de compra y venta en un período de tiempo personalizado para determinar la dirección alcista o bajista, combinándolo con el VWAP semanal y las Bandas de Bollinger para filtrar señales, logrando un seguimiento de tendencia de alta probabilidad. Además, incorpora un mecanismo dinámico de take profit y stop loss para controlar eficazmente el riesgo unilateral.

Principio de la estrategia

- Calcular el indicador de volumen de compra y venta dentro de un período de tiempo personalizado

- BV: Volumen de compra, generado por compras en puntos bajos

- SV: Volumen de venta, generado por ventas en puntos altos

- Procesar el volumen de compra y venta

- Suavizar mediante EMA de 20 períodos

- Separar el volumen de compra y venta procesado en valores positivos y negativos

- Determinar la dirección del indicador

- Indicador mayor que 0 indica alcista, menor que 0 indica bajista

- Combinar con el VWAP semanal y las Bandas de Bollinger para detectar divergencias

- Precio por encima del VWAP e indicador alcista: señal de largo

- Precio por debajo del VWAP e indicador bajista: señal de corto

- Take profit y stop loss dinámicos

- Establecer porcentajes de take profit y stop loss basados en el ATR diario

Ventajas de la estrategia

- El volumen de compra y venta refleja la fuerza real del mercado, capturando la energía potencial de la tendencia

- El VWAP semanal determina la dirección de la tendencia de gran ciclo, y las Bandas de Bollinger identifican señales de ruptura

- El ATR dinámico para take profit y stop loss maximiza la fijación de ganancias y evita el exceso de ajuste

Riesgos de la estrategia

- Los datos de volumen de compra y venta pueden contener cierto error, lo que podría llevar a juicios incorrectos

- La combinación de un solo indicador puede generar señales falsas fácilmente

- Una configuración inadecuada de los parámetros de las Bandas de Bollinger puede reducir las rupturas efectivas

Direcciones de optimización de la estrategia

- Optimizar los indicadores de volumen de compra y venta en múltiples marcos temporales

- Agregar indicadores auxiliares como el volumen de operaciones para filtrar

- Ajustar dinámicamente los parámetros de las Bandas de Bollinger para mejorar la eficiencia de las rupturas

Conclusión

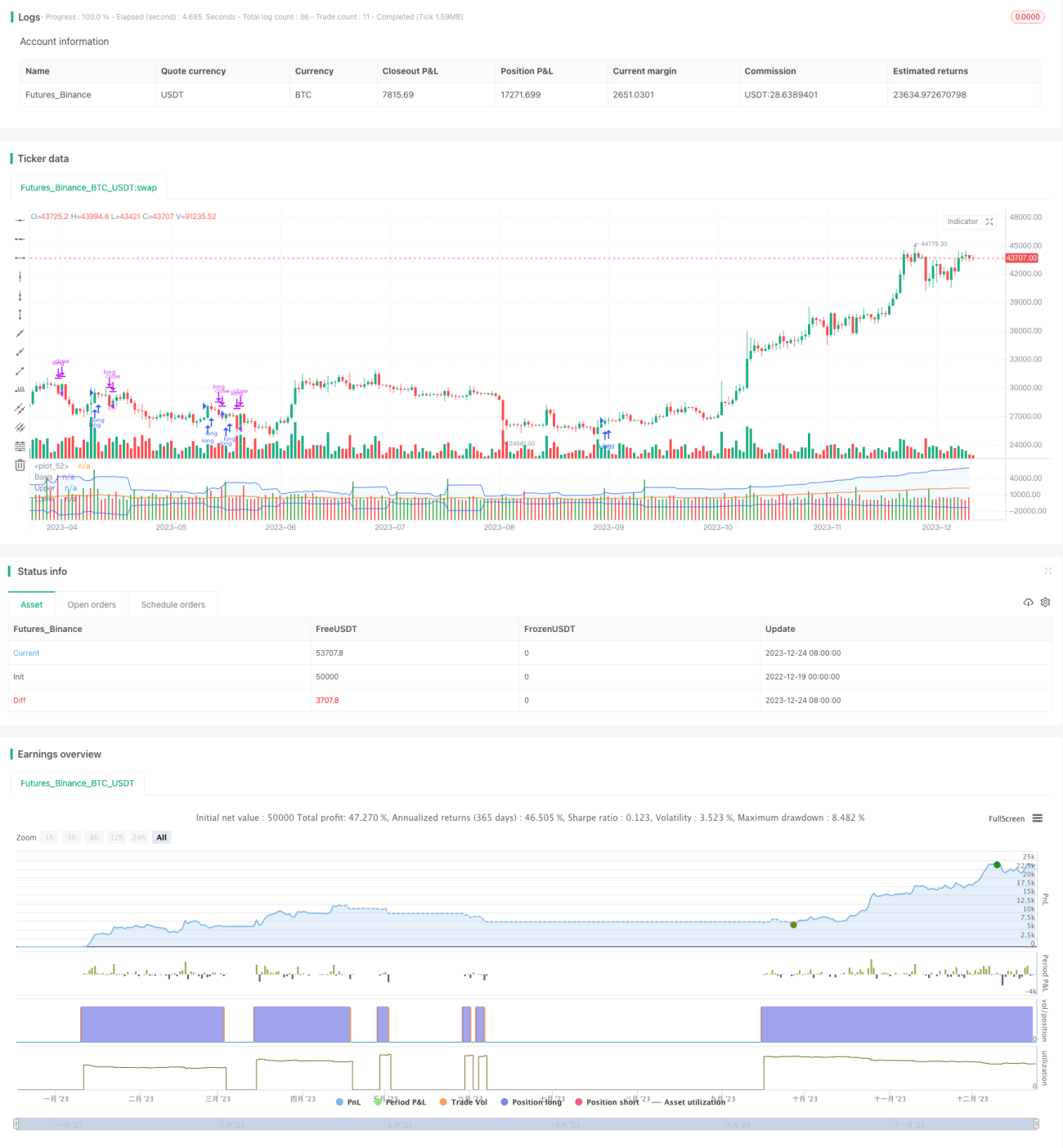

Esta estrategia aprovecha al máximo la capacidad predictiva del volumen de compra y venta, complementada con el VWAP y las Bandas de Bollinger para generar señales de alta probabilidad. Mediante el uso de take profit y stop loss dinámicos, controla eficazmente el riesgo, constituyendo una estrategia de trading cuantitativo eficiente y estable. A medida que los parámetros y reglas se optimicen continuamente, se espera que los resultados sean aún más evidentes.

/*backtest

start: 2022-12-19 00:00:00

end: 2023-12-25 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © original author ceyhun

//@ exlux99 update

- 1