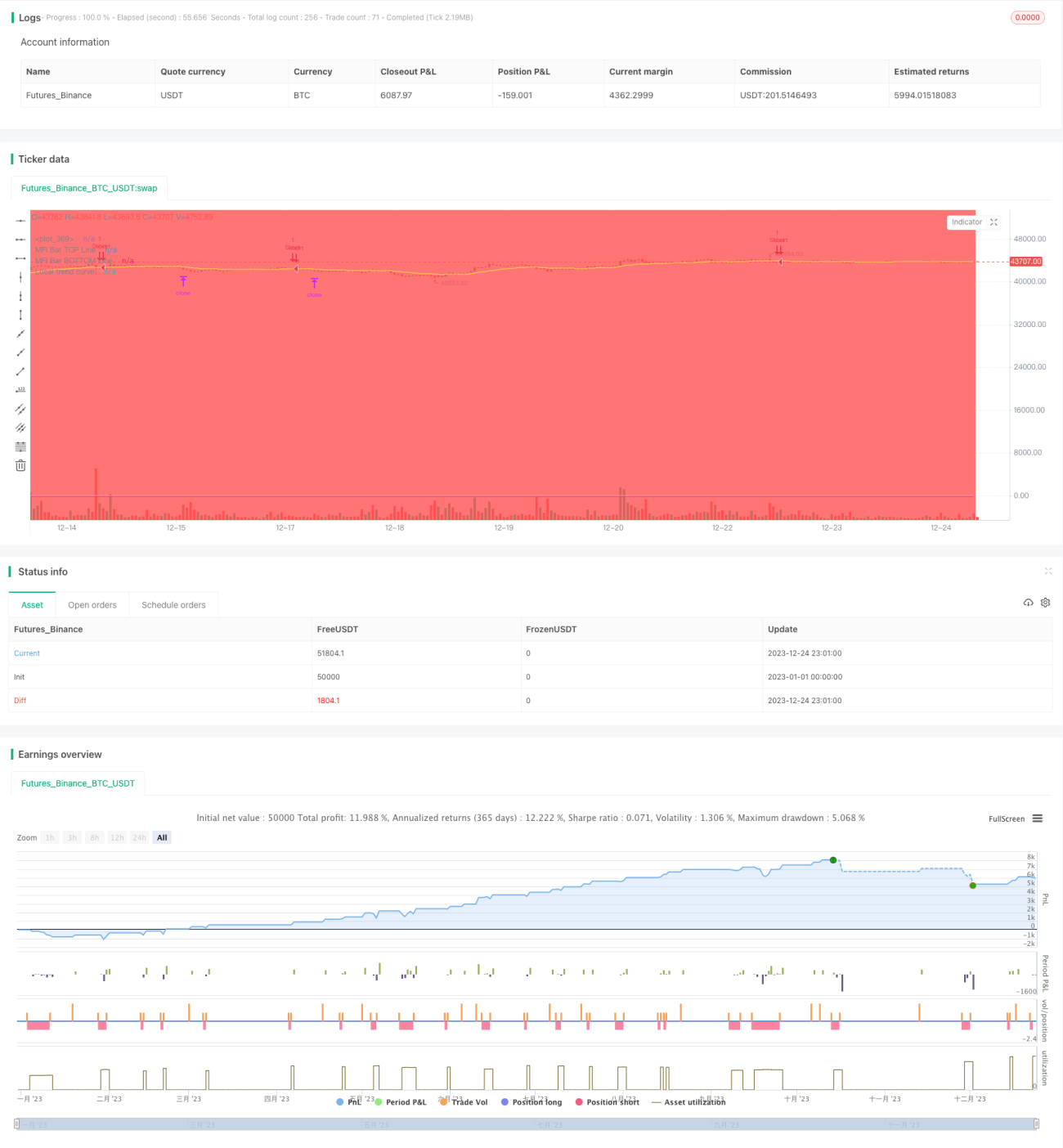

Estrategia de trading cuantitativo basada en un filtro de tendencia dual

Resumen

Se trata de una estrategia de trading cuantitativo que utiliza un filtro de tendencia doble. La estrategia combina un filtro de tendencia global y un filtro de tendencia local, asegurando que solo se abran posiciones cuando la dirección de la tendencia es correcta. Además, la estrategia establece múltiples condiciones de filtro adicionales, como el filtro RSI, el filtro de precio, el filtro de pendiente, etc., para mejorar aún más la fiabilidad de las señales de trading. En cuanto a la salida, la estrategia preestablece niveles de stop loss y take profit. En general, es una estrategia de trading cuantitativa estable y precisa.

Principio de la Estrategia

La lógica central de esta estrategia se basa en un filtro de tendencia doble. El filtro de tendencia global utiliza una EMA de período alto para juzgar la tendencia general del mercado, mientras que el filtro de tendencia local utiliza una EMA de período bajo para juzgar la tendencia local. Solo cuando ambos determinan que la tendencia es consistente, se abre una posición.

Específicamente, la estrategia calcula la línea EMA de BTCUSDT para determinar si el mercado general está en una tendencia alcista o bajista, lo que constituye el filtro de tendencia global. Al mismo tiempo, la estrategia calcula la línea EMA del contrato actual para determinar la tendencia local del mercado, que es el filtro de tendencia local. Cuando ambos coinciden en la misma tendencia, se combinan con otros filtros auxiliares para generar una señal de trading y se abren posiciones con niveles preestablecidos de take profit y stop loss.

Una vez que se determina la señal de trading, la estrategia realiza inmediatamente la orden de apertura. Al mismo tiempo, la estrategia establece previamente los precios de take profit y stop loss. Cuando el precio activa el take profit o el stop loss, la estrategia cierra automáticamente la posición.

Análisis de Ventajas

Esta es una estrategia de trading cuantitativa estable y confiable, con las siguientes ventajas principales:

-

Utiliza un mecanismo de filtro de tendencia doble, que filtra la mayoría de las señales falsas, haciendo que las señales de trading sean más fiables y precisas.

-

Combina múltiples filtros auxiliares, como el filtro RSI, el filtro de precio, etc., mejorando aún más la calidad de las señales.

-

Calcula automáticamente los niveles de take profit y stop loss, eliminando la necesidad de monitoreo manual y reduciendo el riesgo de trading.

-

Los parámetros de la estrategia se pueden personalizar y ajustar, adaptándose a más instrumentos de trading, con una fuerte adaptabilidad.

-

La lógica de la estrategia es clara y fácil de entender, lo que facilita su optimización y mejora, con un amplio margen de expansión.

Análisis de Riesgos

Aunque la estrategia tiene muchas ventajas, todavía existen algunos riesgos de trading, que se concentran principalmente en:

-

El filtro de tendencia doble puede no determinar con precisión el punto de entrada. Se puede optimizar ajustando los parámetros del filtro.

-

La configuración de los niveles de take profit y stop loss puede ser inexacta, lo que podría provocar cierres demasiado tempranos. Se pueden probar diferentes combinaciones de parámetros para encontrar la solución óptima.

-

La elección inadecuada del instrumento de trading y del período puede hacer que la estrategia sea ineficaz. Se recomienda ajustar y probar los parámetros para cada instrumento de trading por separado.

-

Existe cierto riesgo de sobreajuste. Es necesario realizar backtesting en más entornos de mercado para garantizar la solidez de la estrategia.

Direcciones de Optimización

Esta estrategia se puede optimizar principalmente en las siguientes direcciones:

-

Ajustar los parámetros del filtro doble para encontrar la mejor combinación de parámetros.

-

Probar y seleccionar los mejores filtros auxiliares.

-

Optimizar el algoritmo de take profit y stop loss para hacerlo más inteligente.

-

Intentar introducir medios como el aprendizaje automático para lograr un ajuste dinámico de parámetros de la estrategia.

-

Realizar backtesting en más instrumentos de trading y durante períodos más largos para mejorar la estabilidad de la estrategia.

Conclusión

En general, esta estrategia es una estrategia de trading cuantitativa estable, precisa y fácil de optimizar. Utiliza un filtro de tendencia doble combinado con múltiples filtros auxiliares para generar señales de trading, lo que puede filtrar la mayor parte del ruido y hacer que las señales sean más precisas y fiables. Además, la estrategia incorpora configuraciones de take profit y stop loss, lo que puede reducir el riesgo de trading. Es una estrategia de gran valor práctico que, después de la optimización y validación, se puede utilizar directamente en trading real. También tiene un gran potencial de expansión, lo que la convierte en una estrategia cuantitativa digna de un estudio en profundidad.

- 1