Estrategia de trading basada en el cruce de doble media móvil

Resumen

Esta estrategia genera señales de compra y venta basadas en el cruce dorado y el cruce de la muerte de medias móviles. Específicamente, la estrategia utiliza simultáneamente la media móvil exponencial (EMA) de 5 días y la media móvil exponencial doble (DEMA) de 34 días. Cuando la EMA de 5 días a corto plazo cruza al alza la DEMA de 34 días a largo plazo, se genera una señal de compra; cuando la EMA de 5 días a corto plazo cruza a la baja la DEMA de 34 días a largo plazo, se genera una señal de venta.

Principio de la estrategia

- Calcular la EMA de 5 días y la DEMA de 34 días.

- Cuando la EMA de 5 días a corto plazo cruza al alza la DEMA de 34 días a largo plazo, se genera una señal de compra.

- Cuando la EMA de 5 días a corto plazo cruza a la baja la DEMA de 34 días a largo plazo, se genera una señal de venta.

- Opcionalmente, se puede operar solo en un horario de negociación específico.

- Opcionalmente, se puede activar un stop loss dinámico.

Esta estrategia combina dos factores: seguimiento de tendencia y cruce de medias móviles, lo que proporciona un efecto estable. La media móvil, como indicador de seguimiento de tendencia, puede identificar eficazmente la tendencia del mercado; la combinación de EMA y DEMA suaviza los datos de precios para generar señales de trading; el cruce de medias a corto y largo plazo permite anticipar señales de trading en los grandes cambios de tendencia.

Análisis de ventajas

- La idea de la estrategia es simple y clara, fácil de entender e implementar.

- La combinación de medias móviles considera tanto el juicio de tendencia como el suavizado de los datos de precios.

- El cruce de medias a corto y largo plazo puede adelantar señales de trading en puntos de inflexión importantes del mercado.

- Se puede optimizar ajustando la longitud de las medias para adaptarse a diferentes activos y plazos.

- La integración de dos factores mejora la estabilidad de la estrategia.

Análisis de riesgos

- En mercados laterales, pueden generarse múltiples señales falsas.

- Una longitud inadecuada de las medias puede provocar retraso en las señales.

- Un mal ajuste del horario de negociación y del stop loss puede afectar la rentabilidad.

Estos riesgos pueden reducirse ajustando la longitud de las medias, optimizando el horario de negociación y estableciendo un stop loss razonable.

Direcciones de optimización

- Ajustar los parámetros de longitud de las medias para adaptarse a diferentes activos y plazos.

- Optimizar los parámetros de horario de negociación para operar en los períodos de mayor actividad.

- Comparar las ventajas y desventajas del stop loss fijo y el stop loss dinámico.

- Probar el impacto de diferentes métodos de fijación de precios en la estrategia.

Conclusión

Esta estrategia genera señales de trading mediante el cruce de dos medias móviles, combinando el seguimiento de tendencia y el suavizado de datos. Es una estrategia de seguimiento de tendencia simple y práctica. Mediante la optimización de parámetros y reglas, puede adaptarse a diferentes activos y plazos, anticipando señales de trading en los grandes cambios de tendencia y evitando señales falsas. Es recomendable y aplicable.

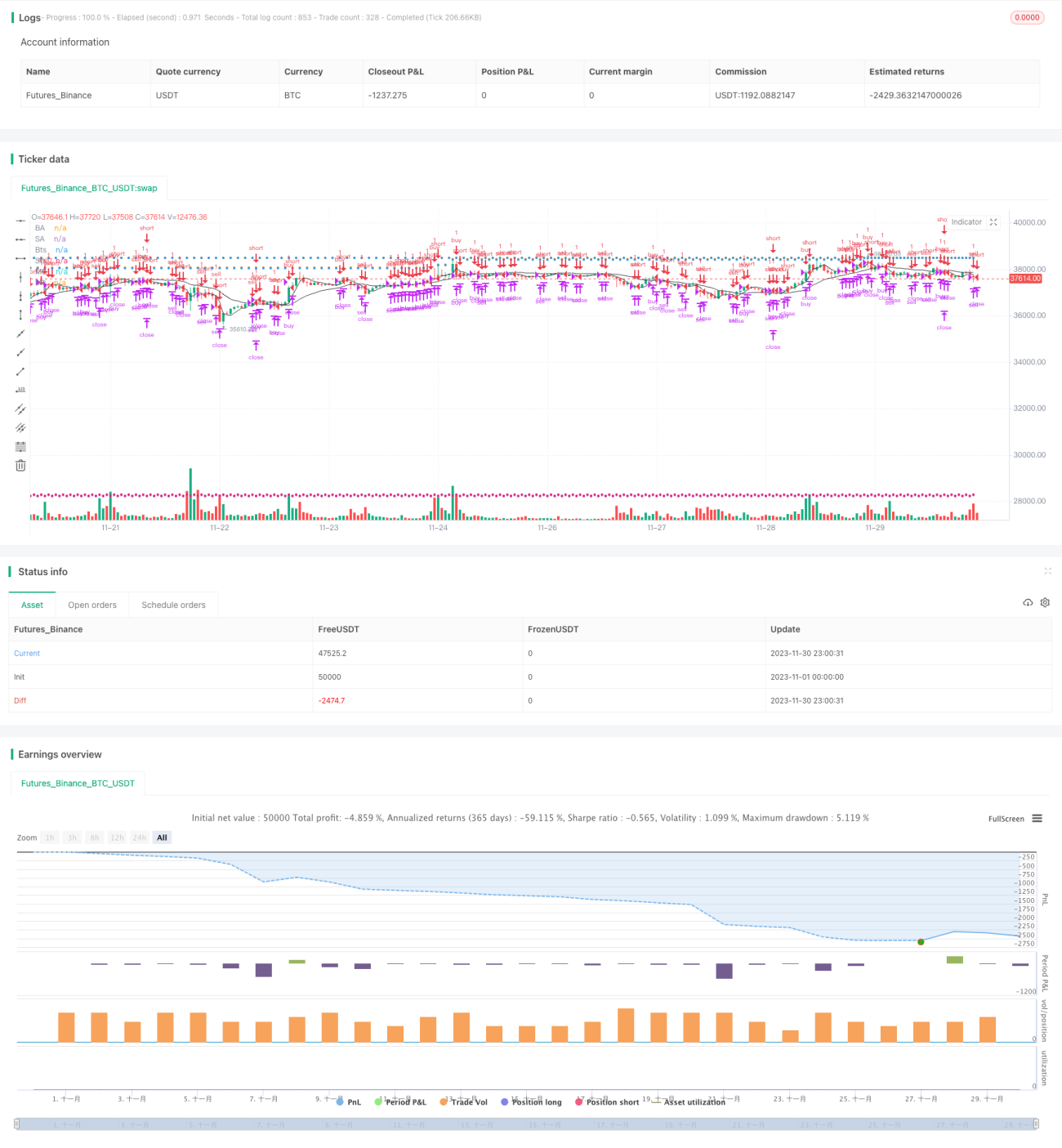

/*backtest

start: 2023-11-01 00:00:00

end: 2023-11-30 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

args: [["v_input_1",false]]

*/

//@version=2

strategy(title='[STRATEGY][RS]MicuRobert EMA cross V2', shorttitle='S', overlay=true)

USE_TRADESESSION = input(title='Use Trading Session?', type=bool, defval=true)- 1