Estrategia de relación de medias móviles en cadena con doble filtro de tendencia

Resumen

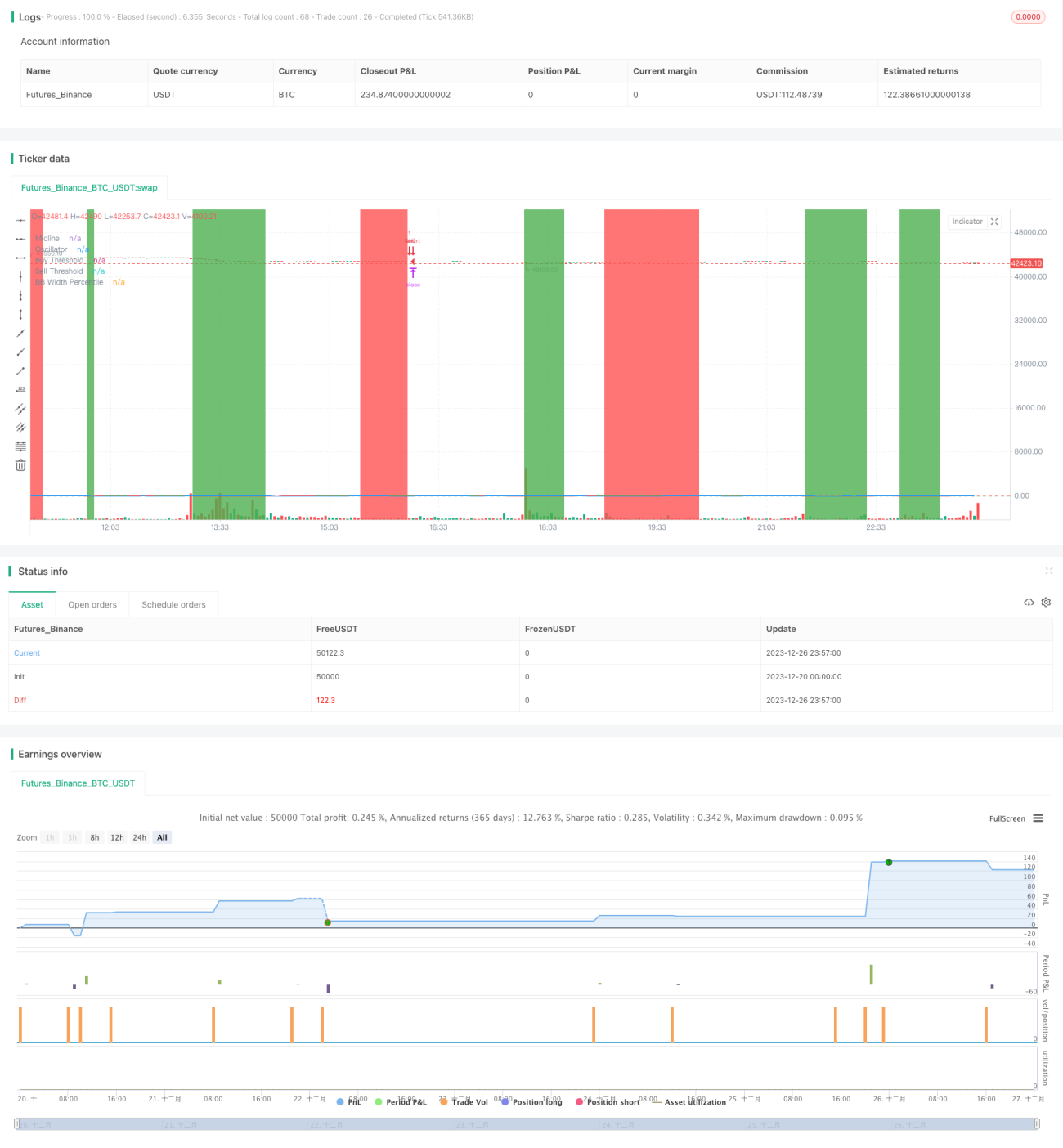

Esta estrategia se basa en el indicador de relación de medias móviles dobles, combinado con un filtro de Bandas de Bollinger y un indicador de tendencia dual, empleando un mecanismo de salida en cadena para seguir la tendencia. La estrategia tiene como objetivo identificar la dirección de la tendencia a medio y largo plazo utilizando el indicador de relación de medias móviles, seleccionar puntos de entrada óptimos cuando la tendencia es clara, y establecer mecanismos de salida con take profit y stop loss para asegurar ganancias y reducir pérdidas.

Principio de la estrategia

- Calcular la media móvil rápida (período 10) y la media móvil lenta (período 50), y calcular su relación, denominada relación de precio de media móvil. Esta relación puede identificar eficazmente los cambios en la tendencia de precio a medio y largo plazo.

- Convertir la relación de precio de media móvil en un percentil, es decir, la fortaleza relativa de la relación actual durante un período de tiempo pasado. Este percentil se define como el oscilador.

- Cuando el oscilador cruza por encima del umbral de compra establecido (10) se genera una señal de compra, y cuando cruza por debajo del umbral de venta (90) se genera una señal de venta, para seguir la tendencia.

- Combinar el indicador de ancho de las Bandas de Bollinger para filtrar las señales de trading, operando solo cuando las bandas se estrechan.

- Utilizar un indicador de tendencia dual como filtro: solo se generan señales de compra cuando el precio está en un canal de tendencia alcista, y solo señales de venta cuando está en un canal de tendencia bajista, evitando operar en contra de la tendencia.

- Establecer un mecanismo de salida en cadena que incluye take profit, stop loss y salidas combinadas, permitiendo predefinir múltiples condiciones de salida y priorizando la salida que maximiza las ganancias.

Ventajas de la estrategia

- El mecanismo de filtro de tendencia dual permite juzgar de manera confiable la dirección de la tendencia principal, evitando operar en contra de la tendencia.

- El indicador de relación de medias móviles es más eficaz que una sola media móvil para detectar cambios de tendencia.

- El indicador de ancho de las Bandas de Bollinger puede identificar eficazmente períodos de baja volatilidad del mercado, donde las señales de trading son más fiables.

- El mecanismo de salida en cadena estabiliza las ganancias y maximiza las utilidades totales.

Riesgos y soluciones

- En mercados laterales sin una tendencia clara, pueden aparecer múltiples señales falsas y reversiones. La solución es combinarlo con el filtro de ancho de las Bandas de Bollinger, operando solo cuando se estrechan.

- Cuando ocurre una reversión clara de tendencia, las medias móviles pueden retrasarse y no detectar la reversión de inmediato. La solución es acortar adecuadamente los períodos de las medias móviles.

- Cuando el mercado presenta gaps, el stop loss puede ser alcanzado instantáneamente, causando pérdidas mayores. La solución es ajustar los parámetros del stop loss para que sean más flexibles.

Direcciones de optimización de la estrategia

- Optimización de parámetros. Se pueden realizar pruebas exhaustivas de los períodos de medias móviles, puntos de compra/venta del oscilador, parámetros de las Bandas de Bollinger y parámetros del filtro de tendencia para encontrar la mejor combinación.

- Incorporar otros indicadores. Se puede considerar agregar indicadores que detecten reversiones de tendencia, como el estocástico (KD) o el MACD, para mejorar la precisión de la estrategia.

- Aprendizaje automático. Se pueden recopilar datos históricos y entrenar modelos mediante algoritmos de aprendizaje automático para optimizar dinámicamente los parámetros, logrando un ajuste adaptativo de los mismos.

Conclusión

Esta estrategia combina el indicador de relación de medias móviles dobles y las Bandas de Bollinger para determinar la dirección de la tendencia a medio y largo plazo. Tras confirmar la tendencia, busca el mejor punto de entrada y establece un mecanismo de salida en cadena para asegurar ganancias, ofreciendo alta fiabilidad y resultados evidentes. La estrategia puede mejorarse aún más mediante la optimización de parámetros, la incorporación de otros indicadores auxiliares y el aprendizaje automático para aumentar la rentabilidad.

- 1