Estrategia de RSI lento con sobrecompra/sobreventa

Resumen

La estrategia de sobrecompra y sobreventa con RSI lento reduce la volatilidad de la curva RSI al extender el período de retroceso del RSI, abriendo así nuevas oportunidades de trading. Esta estrategia también es aplicable a otros indicadores técnicos como el MACD.

Principio de la estrategia

La idea central de esta estrategia es extender la longitud del período de retroceso del RSI, por defecto 500 períodos, y luego suavizar la curva RSI mediante una SMA (media móvil simple) con un período predeterminado de 250. Esto reduce significativamente la volatilidad de la curva RSI, ralentiza la velocidad de reacción del RSI y, por lo tanto, genera nuevas oportunidades de trading.

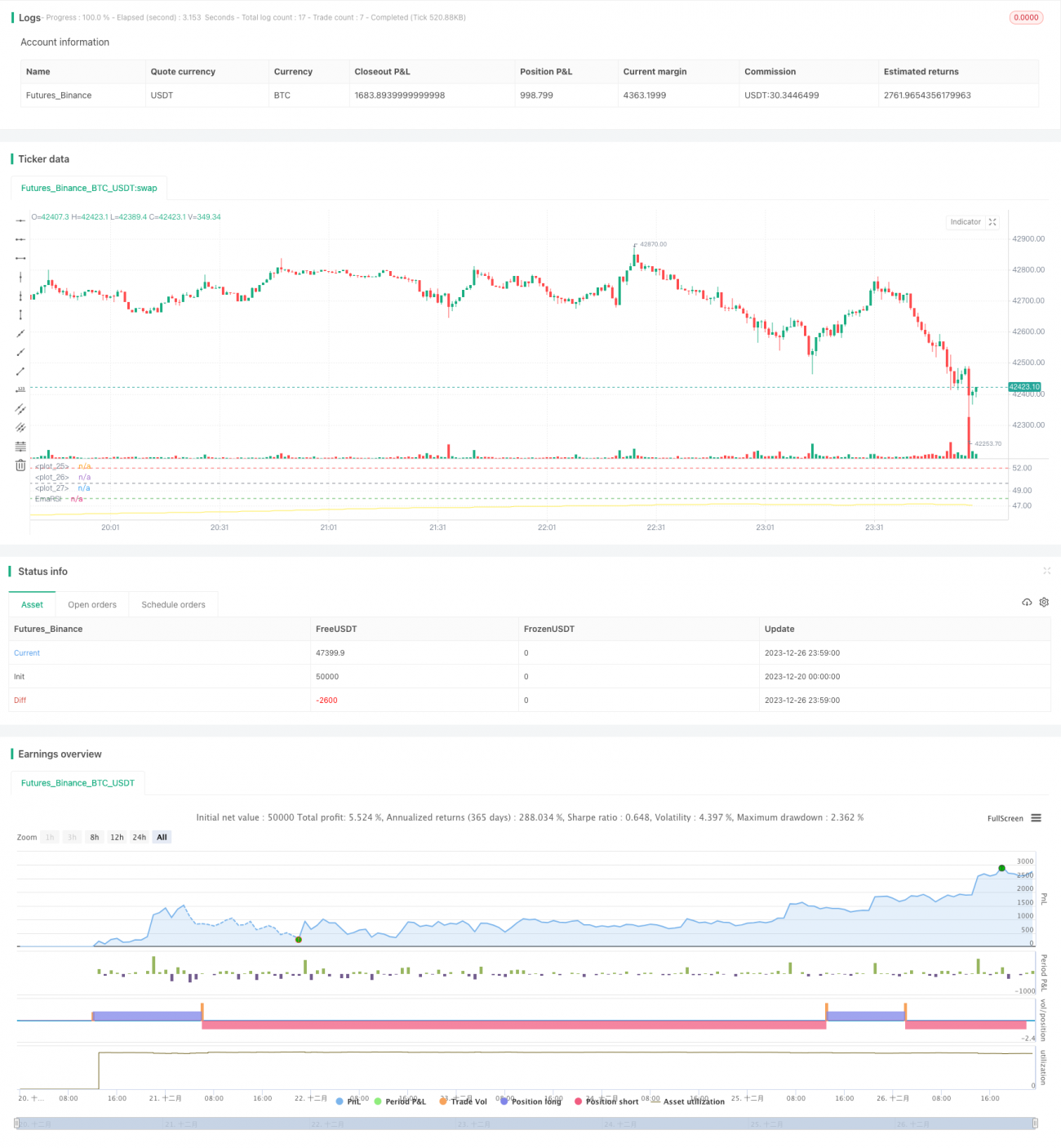

Un período de retroceso demasiado largo disminuye la volatilidad de la curva RSI, por lo que también es necesario ajustar el criterio para determinar sobrecompra y sobreventa. La estrategia establece líneas personalizadas de sobrecompra en 52 y de sobreventa en 48. Cuando el RSI ponderado rompe la línea de sobreventa desde abajo, se genera una señal de compra (largo); cuando rompe la línea de sobrecompra desde arriba, se genera una señal de venta (corto).

Ventajas de la estrategia

- Alto nivel de innovación: abre nuevas perspectivas de trading al extender el período.

- Puede reducir significativamente las señales falsas y mejorar la estabilidad.

- Permite personalizar los umbrales de sobrecompra y sobreventa para adaptarse a diferentes mercados.

- Permite agregar posiciones gradualmente para aumentar la rentabilidad.

Riesgos de la estrategia

- Un período demasiado largo puede hacer perder oportunidades a corto plazo.

- Requiere paciencia para esperar la aparición de puntos de entrada.

- Un ajuste inadecuado de los umbrales de sobrecompra y sobreventa puede aumentar las pérdidas.

- Existe el riesgo de ser objeto de arbitraje.

Soluciones:

- Acortar adecuadamente el período para aumentar la frecuencia de las operaciones.

- Adoptar un enfoque de construcción de posiciones por lotes para diversificar el riesgo.

- Optimizar los parámetros de umbral para adaptarse a diferentes entornos de mercado.

- Establecer puntos de stop-loss para evitar pérdidas excesivas.

Direcciones de optimización de la estrategia

- Optimizar los parámetros del RSI para encontrar la combinación de períodos más adecuada.

- Probar diferentes parámetros de período de suavizado de la SMA.

- Optimizar los parámetros de sobrecompra y sobreventa para ajustarlos a diferentes mercados.

- Agregar una estrategia de stop-loss para controlar las pérdidas por operación.

Conclusión

La estrategia de sobrecompra y sobreventa con RSI lento, al extender el período y utilizar medias móviles para suprimir la volatilidad, logra abrir con éxito nuevas perspectivas de trading. Con una optimización de parámetros y un control de riesgos adecuados, esta estrategia tiene el potencial de obtener rendimientos excedentes estables y eficientes. En general, la estrategia posee una gran innovación y valor práctico.

/*backtest

start: 2023-12-20 00:00:00

end: 2023-12-27 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// Wilder was a very influential man when it comes to TA. However, I'm one to always try to think outside the box.

// While Wilder recommended that the RSI be used only with a 14 bar lookback period, I on the other hand think there is a lot to learn from RSI if one simply slows down the lookback period

// Same applies for MACD.- 1