Estrategia avanzada de Súper Tendencia

Resumen

La estrategia avanzada de supertendencia es una optimización y mejora de la clásica estrategia de supertendencia. Combina la acción del precio, la volatilidad y múltiples indicadores técnicos para mejorar la calidad de las señales, reducir el ruido y capturar con mayor precisión los cambios de tendencia del mercado.

Principio de la Estrategia

El núcleo de la estrategia avanzada de supertendencia es la línea de supertendencia. Se calcula a partir del rango verdadero y el impulso del precio para determinar los posibles cambios y tendencias de precio. Cuando el precio está por encima de la línea de supertendencia, indica una tendencia alcista; por el contrario, indica una tendencia bajista.

A diferencia del indicador de supertendencia clásico que solo considera el precio de cierre y el rango verdadero, la estrategia avanzada también incorpora múltiples dimensiones como el volumen, el oscilador de impulso y datos fundamentales para verificar la fiabilidad de las señales. Este enfoque multivariable asegura que las señales de trading generadas sean más precisas y fiables, y menos propensas a verse afectadas por el ruido del mercado.

Análisis de Ventajas

Las principales ventajas de la estrategia avanzada de supertendencia son:

-

Mayor precisión en la identificación de la dirección del mercado y filtrado de falsas rupturas. Esta estrategia espera a que múltiples factores e indicadores coincidan antes de generar una señal de trading, lo que puede aumentar significativamente la tasa de acierto.

-

Reducción de la interferencia del ruido del mercado. Al utilizar filtros combinados, se puede eliminar una gran cantidad de datos de mercado irrelevantes, haciendo que el juicio sea más claro.

-

Optimización de la gestión de riesgos. Las señales de trading claras ayudan a los operadores a planificar mejor los puntos de stop-loss y take-profit, ofreciendo así un mejor control del riesgo.

-

Alta adaptabilidad. Además de identificar tendencias, esta estrategia se puede combinar con otras herramientas técnicas para construir un sistema de trading completo y eficiente.

Análisis de Riesgos

La estrategia avanzada de supertendencia también presenta los siguientes riesgos principales:

-

Riesgo de configuración de parámetros. Una combinación incorrecta de parámetros de indicadores puede provocar que la estrategia falle o genere demasiadas señales erróneas.

-

Riesgo de error en la identificación de tendencias. Ninguna estrategia puede evitar por completo el riesgo de error en el juicio; un cambio inesperado de la tendencia puede generar pérdidas.

-

Riesgo de sobreoptimización. Cuando los parámetros se ajustan con una precisión excesiva, se vuelven demasiado dependientes de los datos históricos y no logran adaptarse a los cambios del mercado.

-

Riesgo de costos de trading. Al aumentar la frecuencia de las operaciones, los costos de trading, como comisiones y deslizamientos, también aumentan significativamente.

Soluciones correspondientes:

-

Optimizar la configuración de parámetros y realizar pruebas retrospectivas periódicas para verificar su robustez.

-

Establecer stop-loss y take-profit para controlar las pérdidas por operación.

-

Evitar la sobreoptimización y mantener la capacidad de generalización de los parámetros.

-

Calcular la relación riesgo-beneficio de las señales y controlar los costos de trading.

Direcciones de Optimización

La estrategia avanzada de supertendencia puede optimizarse desde los siguientes aspectos:

-

Ajustar los parámetros según los diferentes mercados para que se adapten mejor a las características de cada uno. Por ejemplo, en mercados volátiles se puede acortar el período de cálculo.

-

Agregar un mecanismo de filtrado adaptativo. Cuando el mercado entre en un estado específico, ajustar automáticamente los parámetros del indicador o desactivar ciertos filtros.

-

Explorar métodos de aprendizaje automático, utilizando redes neuronales y otros modelos de entrenamiento para optimizar dinámicamente los parámetros.

-

Combinar indicadores de sentimiento e información de noticias, aprovechando datos no estructurados para mejorar el rendimiento.

-

Añadir una función de dimensionamiento de la posición objetivo. Cuando la tasa de acierto es alta, se puede aumentar la posición para obtener mayores ganancias.

Conclusión

La estrategia avanzada de supertendencia optimiza y mejora el clásico indicador de supertendencia al introducir múltiples filtros e indicadores de confirmación, permitiendo identificar con mayor precisión la dirección del mercado y mejorar la calidad de las señales. En comparación con un solo indicador, esta estrategia ofrece un plan de trading más robusto, completo y eficiente. Sin embargo, también es necesario estar alerta ante el riesgo de un ajuste inadecuado de parámetros y errores de juicio, tomando las medidas adecuadas de control de riesgos. Mediante una optimización continua y su uso conjunto con otras herramientas, la estrategia avanzada de supertendencia tiene un gran potencial de aplicación.

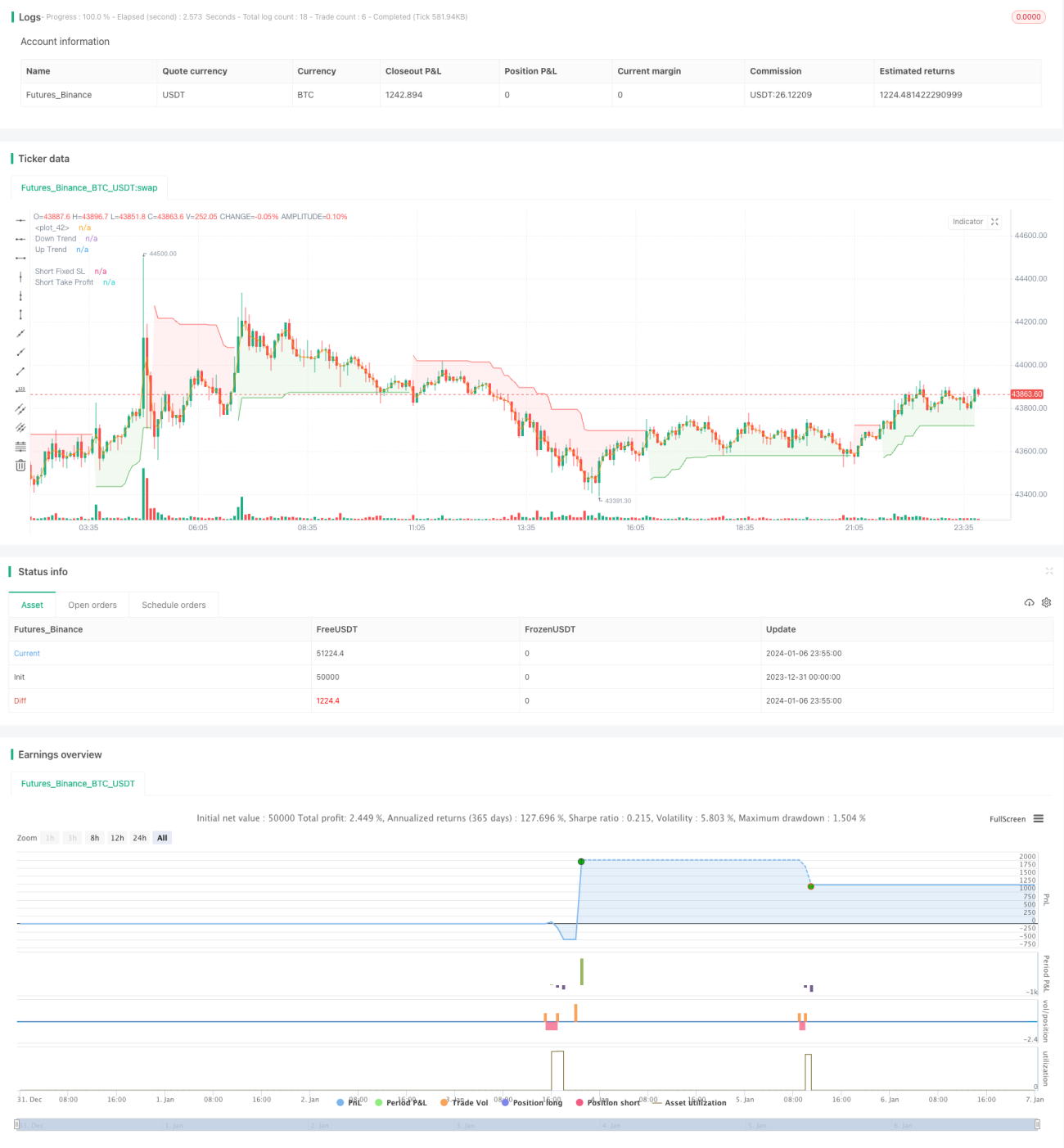

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-07 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © JS_TechTrading

//@version=5- 1