Estrategia de trading de oscilación basada en dos medias móviles

Resumen

Esta estrategia es una estrategia de trading de rango basada en dos medias móviles. Utiliza el cruce de una media móvil rápida y una media móvil lenta como señales de compra y venta. Cuando la media móvil rápida cruza por encima de la media móvil lenta desde abajo, se genera una señal de compra; cuando la media móvil rápida cruza por debajo de la media móvil lenta desde arriba, se genera una señal de venta. La estrategia es adecuada para mercados laterales, permitiendo capturar las fluctuaciones de precios a corto plazo para obtener ganancias.

Principio de la Estrategia

La estrategia utiliza un RMA de longitud 6 como media móvil rápida y un HMA de longitud 4 como media móvil lenta. A través del cruce de la línea rápida y la línea lenta, se juzga la tendencia del precio y se generan señales de trading.

Cuando la línea rápida cruza por encima de la línea lenta desde abajo, indica que el precio ha pasado de caer a subir a corto plazo, siendo un momento de cambio de posiciones. Por lo tanto, la estrategia genera una señal de compra en ese momento. Cuando la línea rápida cruza por debajo de la línea lenta desde arriba, indica que el precio ha pasado de subir a caer a corto plazo, siendo también un momento de cambio de posiciones, generando así una señal de venta.

Además, la estrategia también detecta el juicio de tendencia a largo plazo para evitar operar en contra de la tendencia. Solo cuando el juicio de tendencia a largo plazo también respalda la señal, se generan señales reales de compra y venta.

Ventajas de la Estrategia

Esta estrategia tiene las siguientes ventajas:

- Utiliza el cruce de dos medias móviles para identificar eficazmente los puntos de reversión del precio a corto plazo.

- La combinación de longitudes de la línea rápida y la línea lenta es razonable, generando señales de trading más precisas.

- Combina el juicio de tendencia a corto y largo plazo, filtrando la mayoría de las señales de ruido.

- Implementa lógica de stop-loss y take-profit, permitiendo gestionar el riesgo de forma proactiva.

- Fácil de entender e implementar, adecuada para principiantes en trading cuantitativo.

Riesgos y Soluciones

Esta estrategia también presenta algunos riesgos:

- La estrategia de dos medias móviles puede generar múltiples ganancias pequeñas pero una pérdida grande en una sola operación. La solución es ajustar adecuadamente los niveles de stop-loss y take-profit.

- En mercados laterales, las señales de trading pueden ser frecuentes, lo que puede provocar un exceso de operaciones. La solución es relajar adecuadamente las condiciones de trading para reducir el número de transacciones.

- Los parámetros de la estrategia son propensos a un sobreajuste, por lo que el rendimiento en operaciones reales puede no ser óptimo. La solución es realizar pruebas de robustez de los parámetros.

- La estrategia tiene un rendimiento deficiente en mercados con tendencia. La solución es agregar un módulo de juicio de tendencia o combinarla con estrategias de tendencia.

Direcciones de Optimización

Las posibles mejoras de esta estrategia incluyen:

- Actualizar los indicadores de media móvil, utilizando filtros adaptativos como el filtro de Kalman.

- Agregar un módulo de aprendizaje automático para entrenar la identificación de puntos de compra y venta mediante IA.

- Incorporar un módulo de gestión de capital para automatizar el control de riesgos.

- Combinar con factores de alta frecuencia para encontrar señales de trading más fuertes.

- Arbitraje entre múltiples instrumentos y mercados.

Conclusión

En general, esta estrategia de rango con dos medias móviles es una estrategia de trading cuantitativo típica y práctica. Tiene una fuerte adaptabilidad y los principiantes pueden aprender mucho sobre el desarrollo de estrategias a partir de ella. Al mismo tiempo, tiene un amplio margen de mejora, pudiendo optimizarse aún más mediante la combinación de más técnicas cuantitativas para obtener mejores resultados.

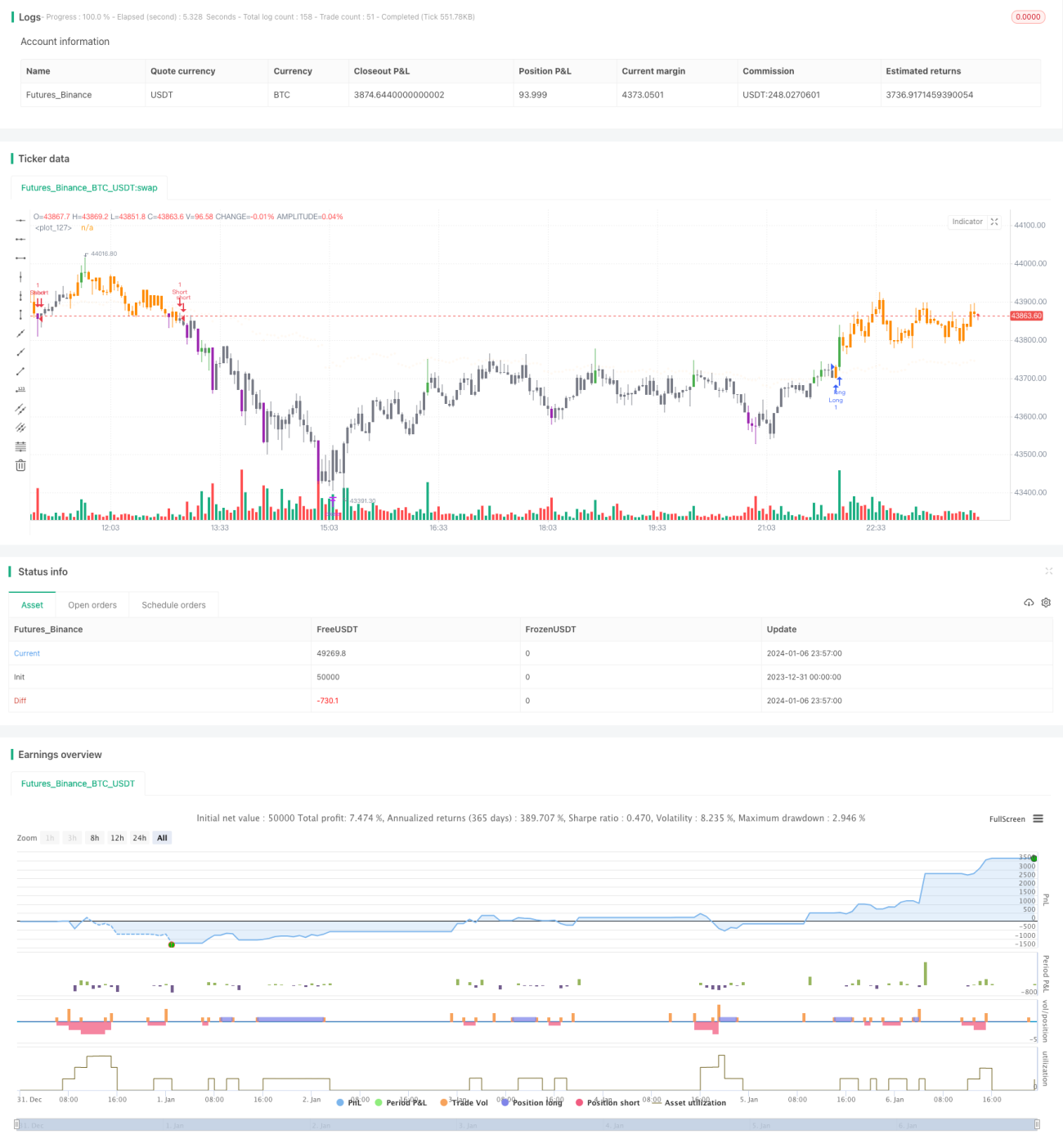

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-07 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © dc_analytics

// https://datacryptoanalytics.com/

- 1