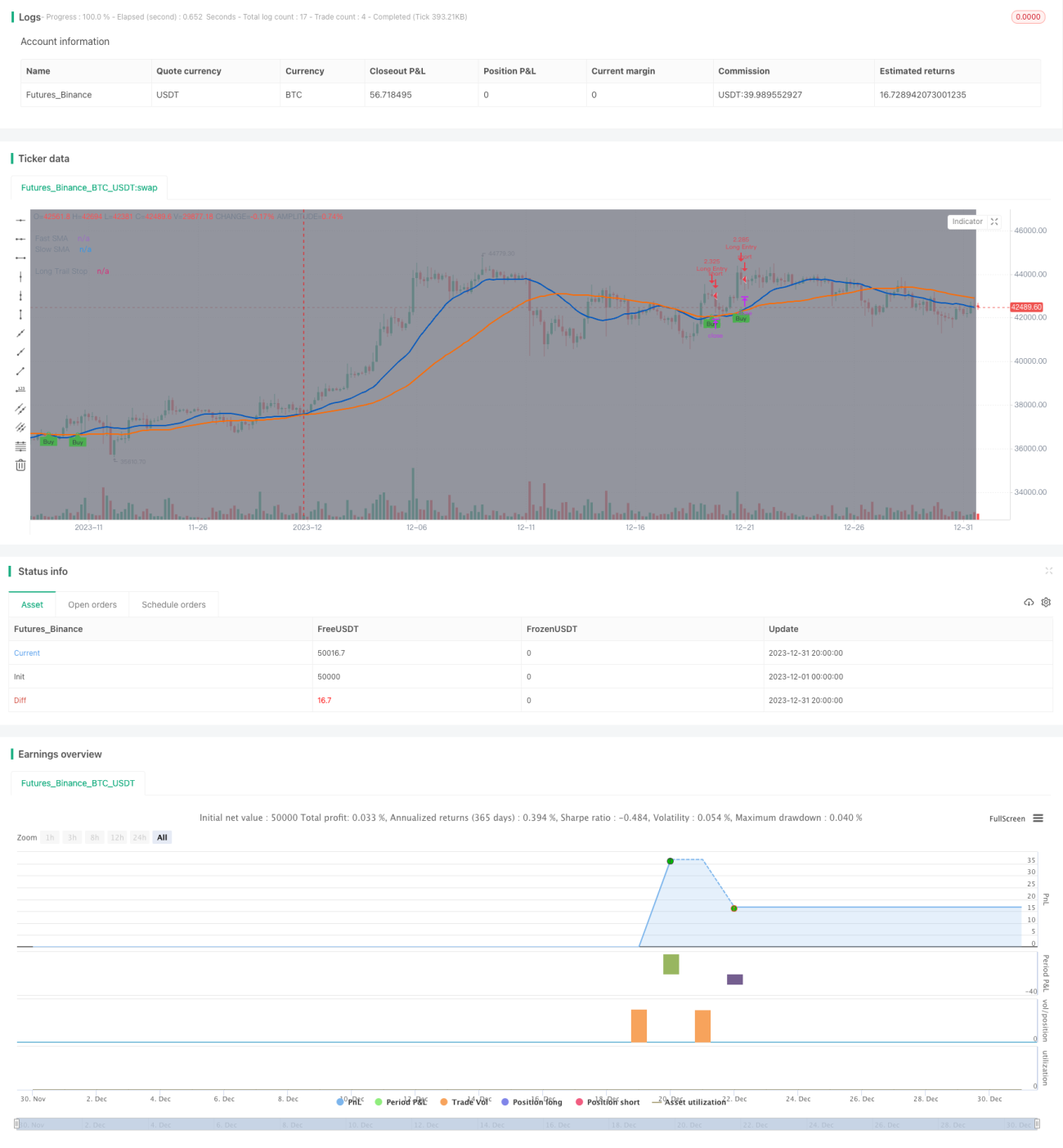

Estrategia de trailing stop dinámico

Resumen

Esta estrategia determina la tendencia calculando el cruce entre una media móvil rápida y una media móvil lenta. Cuando la media móvil rápida cruza por encima de la media móvil lenta, se abre una posición larga, y se establece una línea de stop loss dinámico para asegurar ganancias, saliendo cuando el precio varía un cierto porcentaje.

Principio de la estrategia

La estrategia utiliza el cruce dorado de la media móvil rápida y la media móvil lenta para identificar el inicio de una tendencia alcista. Específicamente, se calcula la media móvil simple del precio de cierre durante un período determinado, y se comparan los valores de la media rápida y la media lenta. Cuando la media rápida cruza por encima de la media lenta, se determina que ha comenzado una tendencia alcista, y se abre una posición larga.

Tras abrir la posición larga, la estrategia no establece un stop loss fijo, sino que utiliza una línea de stop loss dinámico para asegurar ganancias. Esta línea de stop loss se establece como: Precio máximo * (1 – porcentaje de stop loss establecido). De esta forma, la línea de stop loss se eleva a medida que el precio sube, y se sale cuando el precio cae un cierto porcentaje.

La ventaja de este método es que permite seguir la tendencia alcista sin límite, y puede asegurar ganancias mediante el stop loss una vez que se ha alcanzado un cierto nivel de beneficio.

Análisis de ventajas

Las principales ventajas de esta estrategia de stop loss dinámico son:

-

Permite seguir la tendencia alcista sin límite, sin perder grandes movimientos del mercado. Con un stop loss fijo es fácil ser detenido al inicio de una gran tendencia.

-

Permite asegurar ganancias estableciendo un porcentaje de stop loss. Si solo se sigue la tendencia sin stop loss, al final del movimiento podría haber pérdidas. Establecer un stop loss permite asegurar ganancias.

-

Es más flexible que un stop loss fijo. Un stop loss fijo solo puede establecer un precio, mientras que aquí el stop loss cambia según el precio máximo.

-

Menor riesgo de retroceso. Con un stop loss fijo, la distancia entre el precio de stop loss y el precio máximo es grande, y podría activarse durante una corrección normal. Aquí el stop loss está muy cerca del precio máximo, por lo que una corrección normal no lo activa.

Análisis de riesgos

Esta estrategia también presenta algunos riesgos:

-

El indicador para determinar la señal de entrada puede ser inestable y generar señales falsas.

-

El método de stop loss es único y no considera otros factores. El mercado podría sufrir cambios bruscos que dejen la estrategia ineficaz.

-

No hay límite de ganancias, se depende del stop loss. Si el stop loss falla, podrían ocurrir pérdidas significativas.

-

Los parámetros deben optimizarse. Períodos de la media móvil y otros parámetros deben ajustarse al óptimo.

Direcciones de optimización

La estrategia puede optimizarse en los siguientes aspectos:

-

Añadir más indicadores para confirmar la entrada y evitar señales falsas. Por ejemplo, incluir el volumen de operaciones.

-

Añadir un take profit. Cuando las ganancias alcancen un cierto porcentaje, cerrar la posición.

-

Aumentar la seguridad del stop loss. Cuando ocurran anomalías en el mercado, ajustar significativamente la distancia del stop loss.

-

Optimizar los parámetros según el instrumento y el período de negociación. Diferentes instrumentos y horarios requieren ajustes de parámetros.

-

Incorporar aprendizaje automático para ajustar dinámicamente los parámetros, permitiendo que el modelo optimice automáticamente los indicadores y el margen de stop loss.

Resumen

La idea general de esta estrategia es clara y razonable. Utilizar medias móviles rápidas y lentas para identificar la tendencia es un método clásico, y el uso de un stop loss dinámico permite asegurar ganancias y reducir el riesgo de manera efectiva. Sin embargo, estos indicadores y parámetros deben someterse a pruebas y optimización constantes para que la estrategia genere beneficios estables. También hay que protegerse contra el impacto de cambios bruscos del mercado, lo que requiere mejorar el marco general y agregar mecanismos de seguridad.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//

// ▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒

// ------------------------------------------------------------------------------ 1