Estrategia de combinación de medias móviles con reversión de momentum

Resumen

Esta estrategia combina la estrategia de reversión 123 y la estrategia de media móvil CMO para generar señales de compra y venta. La estrategia de reversión 123 utiliza el cierre de dos días consecutivos que forman nuevos máximos o mínimos, combinado con un oscilador estocástico para medir la fuerza de compra y venta del mercado, generando señales de trading. La estrategia de media móvil CMO utiliza el indicador CMO para evaluar el impulso del precio y generar señales de trading. La combinación de ambas estrategias da lugar a señales más fiables.

Principio de la Estrategia

La estrategia de reversión 123 genera señales de trading basándose en los siguientes principios:

- Cuando el precio de cierre sube durante dos días consecutivos y el oscilador estocástico de 9 periodos está por debajo de 50, se toma una posición larga.

- Cuando el precio de cierre baja durante dos días consecutivos y el oscilador estocástico de 9 periodos está por encima de 50, se toma una posición corta.

Esta estrategia identifica si el precio forma nuevos máximos o mínimos en el corto plazo y, combinada con el indicador estocástico de dirección alcista/bajista, genera señales de trading.

La estrategia de media móvil CMO genera señales de trading basándose en los siguientes principios:

- Calcular el valor CMO de 5, 10 y 20 periodos.

- Obtener su promedio.

- Cuando el CMO promedio supera 70, se toma una posición larga.

- Cuando el CMO promedio es inferior a -70, se toma una posición corta.

Esta estrategia evalúa la dirección del impulso del precio mediante el conjunto de valores CMO de diferentes periodos, generando señales de trading.

La estrategia combinada aplica una operación AND a las señales de ambas estrategias: solo cuando ambas señalan simultáneamente largo o corto, la estrategia combinada genera una señal real de trading.

Ventajas de la Estrategia

Esta estrategia presenta las siguientes ventajas:

- Las señales combinadas son más fiables y reducen las señales falsas.

- La estrategia de reversión 123 es adecuada para capturar tendencias tras ajustes a corto plazo.

- La estrategia de media móvil CMO evalúa el impulso del precio a nivel macro.

- Puede adaptarse a diferentes condiciones de mercado.

Análisis de Riesgos

Esta estrategia también presenta los siguientes riesgos:

- La estrategia de reversión 123 depende en gran medida de la formación de patrones de precio, que pueden fallar.

- El indicador CMO es sensible a la volatilidad del mercado y puede generar señales erróneas.

- Las señales de la estrategia combinada pueden ser demasiado conservadoras, perdiendo oportunidades de trading.

- Es necesario ajustar adecuadamente los parámetros para adaptarse a diferentes periodos y condiciones de mercado.

Las contramedidas incluyen:

- Optimizar las reglas de identificación de patrones de la estrategia de reversión.

- Añadir otros indicadores auxiliares a la estrategia de media móvil CMO.

- Evaluar el rendimiento de la estrategia en los últimos periodos y ajustar los parámetros dinámicamente.

Direcciones de Optimización

La estrategia puede optimizarse en los siguientes aspectos:

- Utilizar algoritmos de aprendizaje automático para optimizar automáticamente los pesos de la combinación.

- Incorporar un módulo de ajuste de parámetros adaptativo para optimizar dinámicamente los parámetros de la estrategia.

- Añadir un módulo de stop-loss para controlar eficazmente el riesgo.

- Evaluar la robustez de la estrategia y mejorar los algoritmos de reconocimiento de patrones.

- Combinar factores como la selección de sectores y fundamentales.

Conclusión

Esta estrategia combina dos estrategias complementarias, la reversión 123 y la media móvil CMO, formando una estrategia de trading combinada eficaz. Bajo la premisa de controlar el riesgo, puede generar rendimientos estables y superiores. Con la optimización continua de algoritmos y modelos, se espera que la rentabilidad y estabilidad de esta estrategia sigan mejorando.

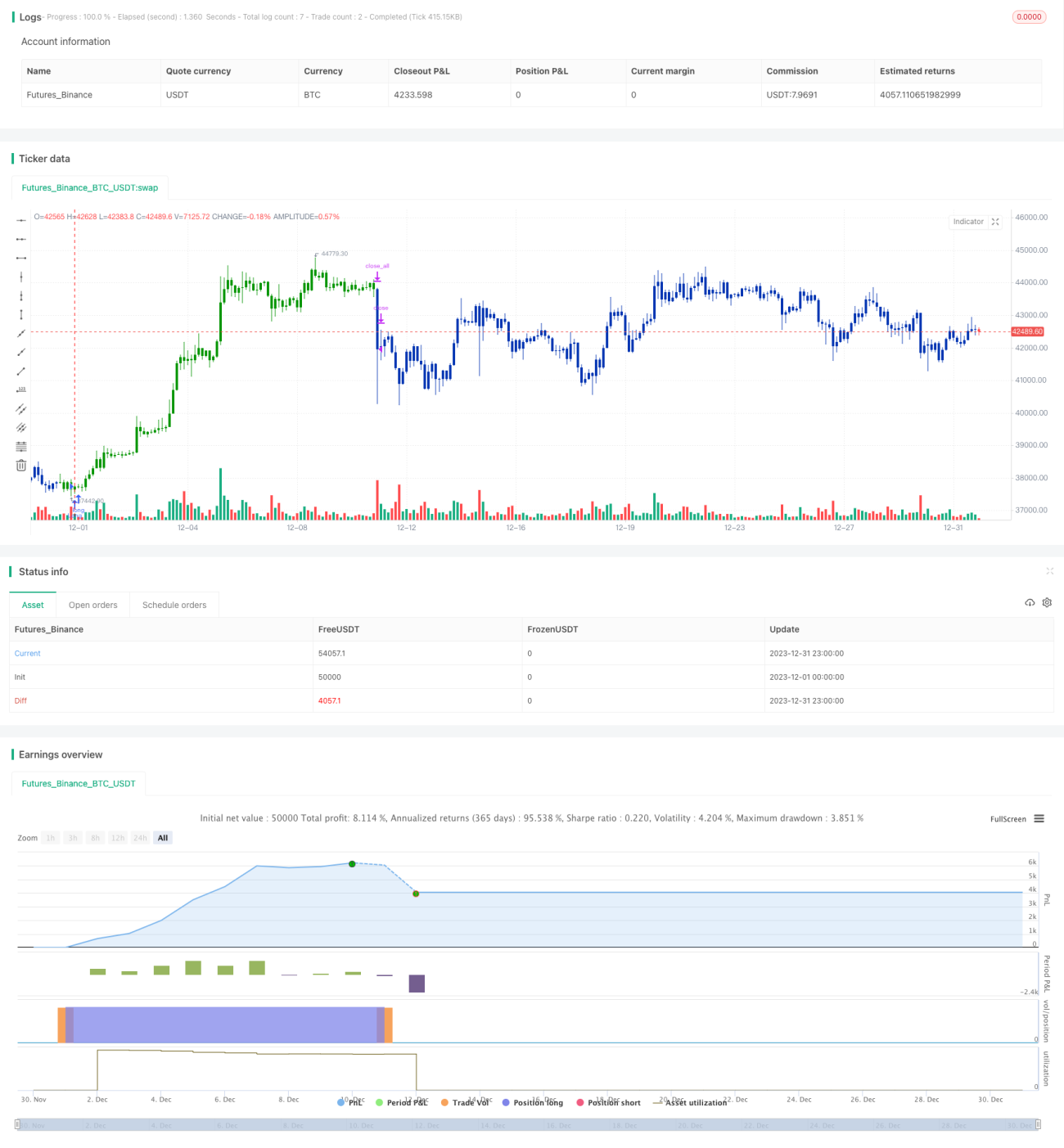

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 3h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 19/09/2019

// This is combo strategies for get a cumulative signal. - 1