Estrategia de ganancias a corto plazo basada en el patrón V del RSI

Resumen

Esta estrategia se basa en la formación en V del indicador RSI, combinada con el filtro de la media móvil EMA, para formar una estrategia de ganancias a corto plazo relativamente confiable. Puede capturar las oportunidades de rebote de precios en la zona de sobreventa, y mediante la señal de formación en V del RSI, realiza compras precisas, con el objetivo de obtener ganancias a corto plazo.

Principios de la estrategia

- Utilizar que la media móvil de 20 días esté por encima de la media móvil de 50 días como condición para posiciones largas a largo plazo.

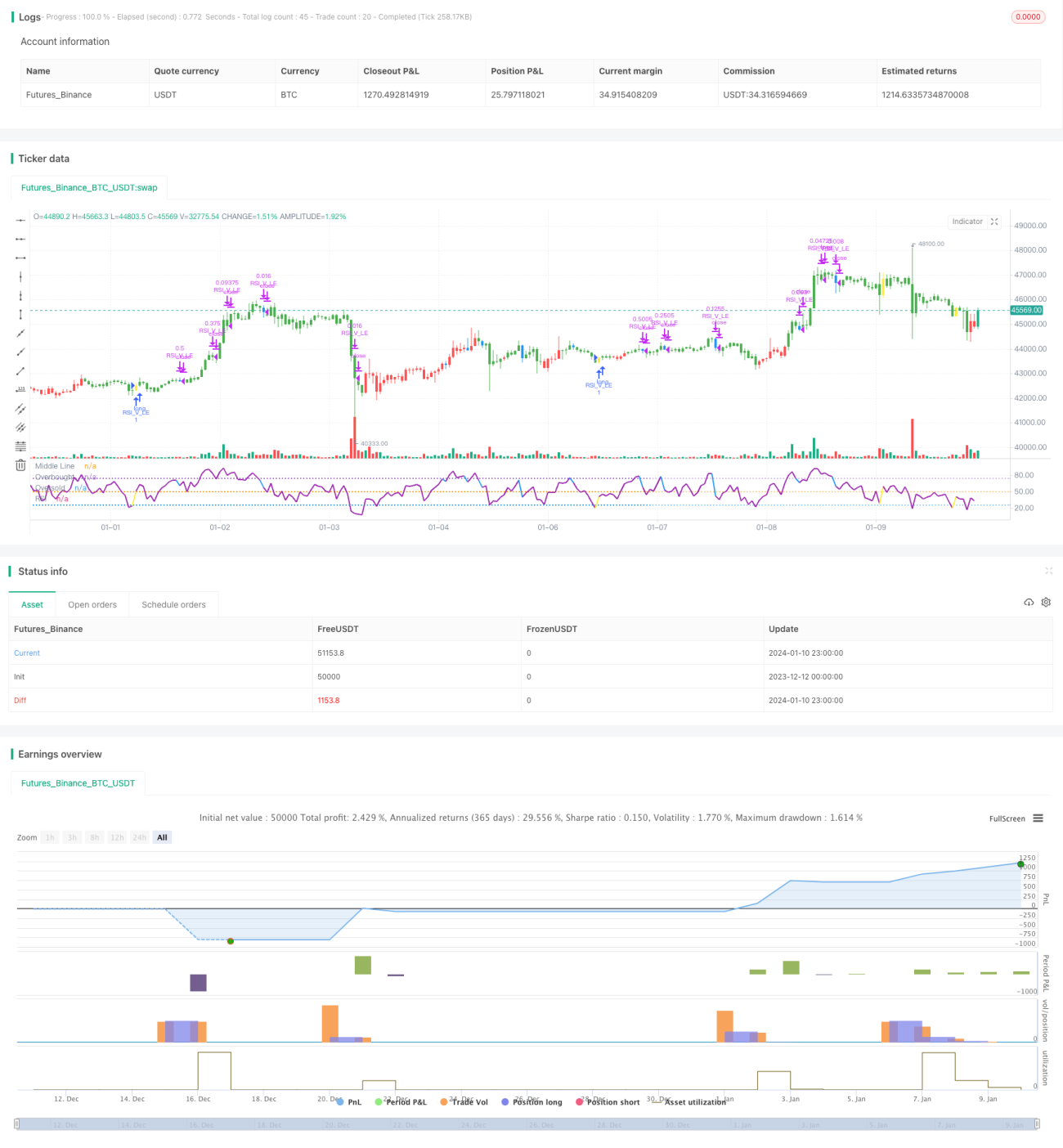

- El RSI forma una formación en V, lo que indica una oportunidad de rebote de sobreventa.

- El mínimo de la vela anterior es menor que el mínimo de las dos velas anteriores.

- El RSI de la vela actual es superior al RSI de las dos velas anteriores.

- El RSI cruza por encima de 30 como señal de finalización de la formación en V, se abre una posición larga.

- El stop loss se sitúa por debajo del 8% del precio de entrada.

- El RSI cruza por encima de 70, se inicia tzinfo de la posición, el stop loss se mueve al precio de entrada.

- El RSI cruza por encima de 90, se inicia tzinfo de 3/4 de la posición.

- El RSI cruza por debajo de 10 / se activa el stop loss, se cierra toda la posición.

Análisis de ventajas

- Utilizar la media móvil EMA para determinar la tendencia principal, evitando operar en contra de la tendencia.

- La formación en V del RSI identifica oportunidades de rebote en la zona de sobreventa, capturando tendencias de reversión.

- Múltiples mecanismos de stop loss para controlar el riesgo.

Análisis de riesgos

- En un mercado con una fuerte tendencia bajista, es posible que el stop loss no funcione, causando pérdidas significativas.

- Las señales de la formación en V del RSI pueden ser erróneas, lo que provoca pérdidas innecesarias.

Direcciones de optimización

- Optimizar los parámetros del RSI para encontrar formaciones en V más confiables.

- Combinar con otros indicadores para evaluar la fiabilidad de las señales de reversión.

- Optimizar la estrategia de stop loss, para evitar ser demasiado agresivo y al mismo tiempo detener las pérdidas a tiempo.

Resumen

Esta estrategia integra el filtro de la media móvil EMA y la identificación de la formación en V del RSI, formando un conjunto de estrategias de trading a corto plazo relativamente confiables. Puede aprovechar eficazmente las oportunidades de rebote en la zona de sobreventa y lograr ganancias a corto plazo. Mediante la optimización continua de parámetros y modelos, y la mejora de los mecanismos de stop loss, esta estrategia puede mejorar aún más su estabilidad y rentabilidad. Abre otra puerta a las ganancias a corto plazo para los traders cuantitativos.

- 1