Estrategia de trading de regresión de media móvil bidireccional

Resumen

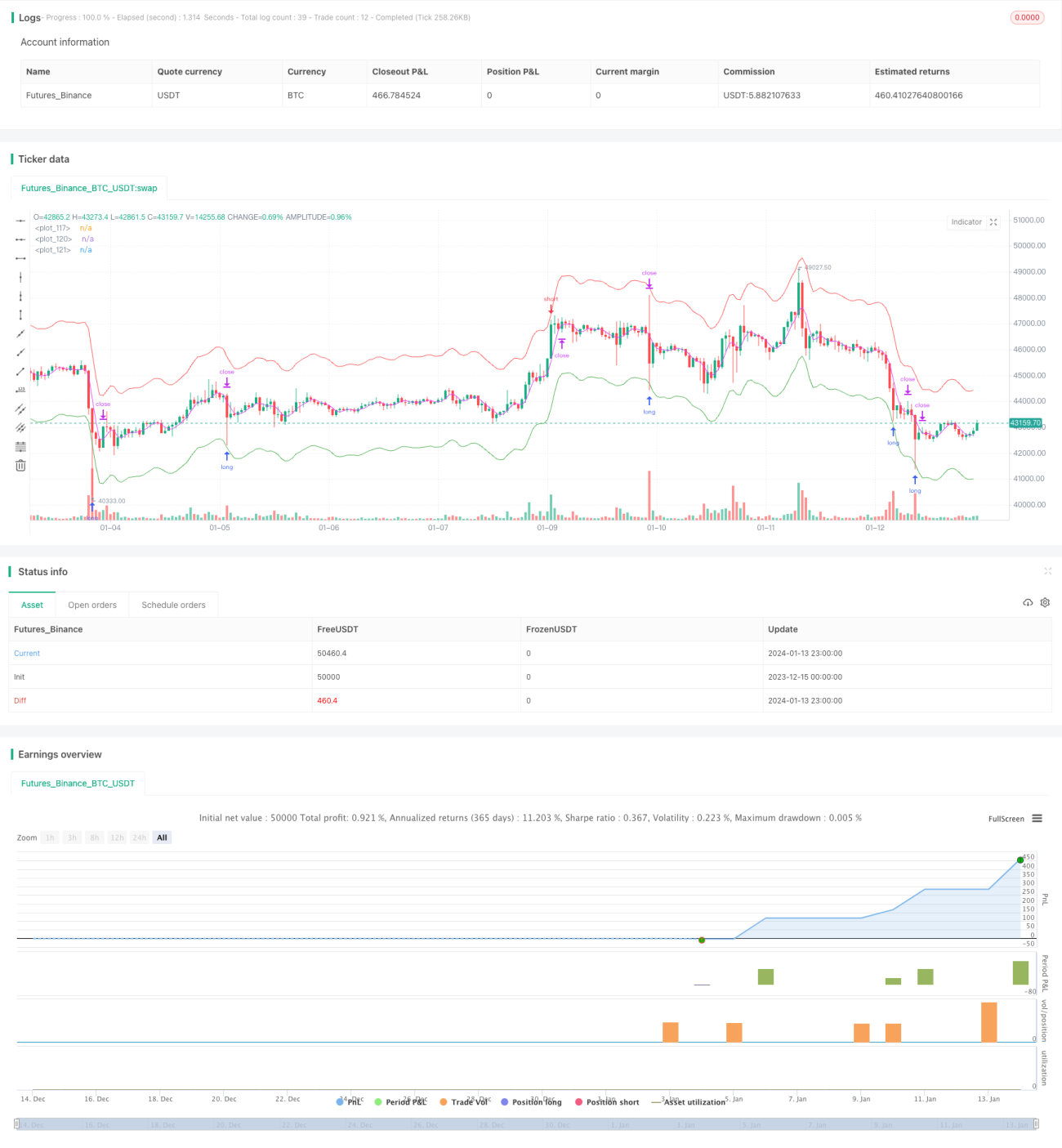

La Estrategia de Trading de Reversión a la Media con Medias Móviles Bidireccionales (Bidirectional Moving Average Reversion Trading Strategy) es una estrategia de trading cuantitativa que se basa en el principio de reversión a la media del precio. Esta estrategia utiliza múltiples grupos de medias móviles para capturar oportunidades de reversión del precio. Cuando el precio se desvía de la media móvil en un cierto margen, se abre una posición, y cuando el precio regresa a la media móvil, se cierra la posición para obtener ganancias.

Principio de la Estrategia

La estrategia se fundamenta principalmente en la teoría de reversión a la media del precio. Sostiene que el precio siempre fluctúa alrededor de un valor promedio, y cuando se desvía significativamente de este promedio, es más probable que regrese a la media. Específicamente, la estrategia configura tres grupos de medias móviles: la media móvil de apertura, la media móvil de cierre y la media móvil de límite. Cuando el precio toca la media móvil de apertura, se abre la posición larga o corta correspondiente. Cuando el precio toca la media móvil de cierre, se cierra la posición anterior. Finalmente, si el precio continúa moviéndose sin revertir, la media móvil de límite permite controlar las pérdidas.

Desde la lógica del código, la media móvil de apertura se compone de una línea larga y una línea corta, respectivamente para posiciones largas y cortas. El grado de desviación entre estas líneas y el precio determina el tamaño de la posición. Además, la media móvil de cierre es una línea independiente que determina el momento de cerrar la posición. Cuando el precio alcanza esta media móvil, la posición se cierra.

Análisis de Ventajas

Las ventajas principales de la estrategia de reversión a la media con medias móviles bidireccionales son:

- Captura reversiones del precio, adecuada para mercados laterales o en consolidación.

- Controla el riesgo mediante límites de pérdida.

- Parámetros personalizables, alta adaptabilidad.

- Fácil de entender, conveniente para la optimización de parámetros.

Esta estrategia es adecuada para instrumentos con baja volatilidad y rangos de precios reducidos, especialmente aquellos que entran en una fase de consolidación. Captura eficazmente las oportunidades de reversión temporal del precio. Además, sus medidas de control de riesgo son relativamente completas; incluso si el precio no revierte, las pérdidas se mantienen dentro de un cierto rango.

Análisis de Riesgos

La estrategia de reversión a la media con medias móviles bidireccionales también presenta algunos riesgos:

- Riesgo de comprar en techos y vender en suelos. Si el precio experimenta un movimiento brusco, la estrategia podría abrir posiciones continuamente y eventualmente provocar una liquidación forzada.

- Riesgo de alta volatilidad del precio. Si la amplitud de las oscilaciones del precio es demasiado grande, las posiciones podrían alcanzar el límite de pérdida y ser cerradas forzadamente.

- Riesgo de optimización de parámetros. La configuración de los parámetros de la estrategia tiene un impacto significativo en su rentabilidad; si los parámetros no se configuran adecuadamente, la probabilidad de obtener ganancias se reduce drásticamente.

Para mitigar estos riesgos, se pueden optimizar los siguientes aspectos:

- Aumentar las restricciones de apertura de posiciones para evitar aperturas demasiado frecuentes.

- Reducir adecuadamente el tamaño de las posiciones para prevenir el riesgo de liquidación forzada.

- Optimizar los períodos de las medias móviles, los parámetros de la línea de cierre, etc.

Direcciones de Optimización

La estrategia tiene un amplio margen de mejora, principalmente desde los siguientes ángulos:

- Agregar lógica de condiciones de apertura para evitar comprar en techos y vender en suelos durante tendencias.

- Incorporar lógica de reducción de tamaño de posición para mitigar el riesgo de grandes oscilaciones de precios.

- Probar diferentes tipos de indicadores de medias móviles para encontrar mejores combinaciones de parámetros.

- Utilizar métodos de aprendizaje automático para optimizar automáticamente los parámetros.

- Agregar una estrategia de stop loss automático para un mejor control del riesgo.

Conclusión

La Estrategia de Trading de Reversión a la Media con Medias Móviles Bidireccionales obtiene ganancias aprovechando las oportunidades de reversión del precio después de desviarse de la media móvil. Controla efectivamente el riesgo y puede generar mejores rendimientos mediante la optimización de parámetros. Aunque la estrategia también presenta ciertos riesgos, estos pueden gestionarse mejorando la lógica de apertura de posiciones, reduciendo el tamaño de las posiciones, entre otros métodos. Es simple y fácil de entender, lo que la hace digna de estudio y optimización por parte de los traders cuantitativos.

/*backtest

start: 2023-12-15 00:00:00

end: 2024-01-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title = "hamster-bot MRS 2", overlay = true, default_qty_type = strategy.percent_of_equity, initial_capital = 100, default_qty_value = 30, pyramiding = 1, commission_value = 0.1, backtest_fill_limits_assumption = 1)

info_options = "Options"

- 1