Estrategia de seguimiento de tendencia basada en la media móvil SSL

Resumen

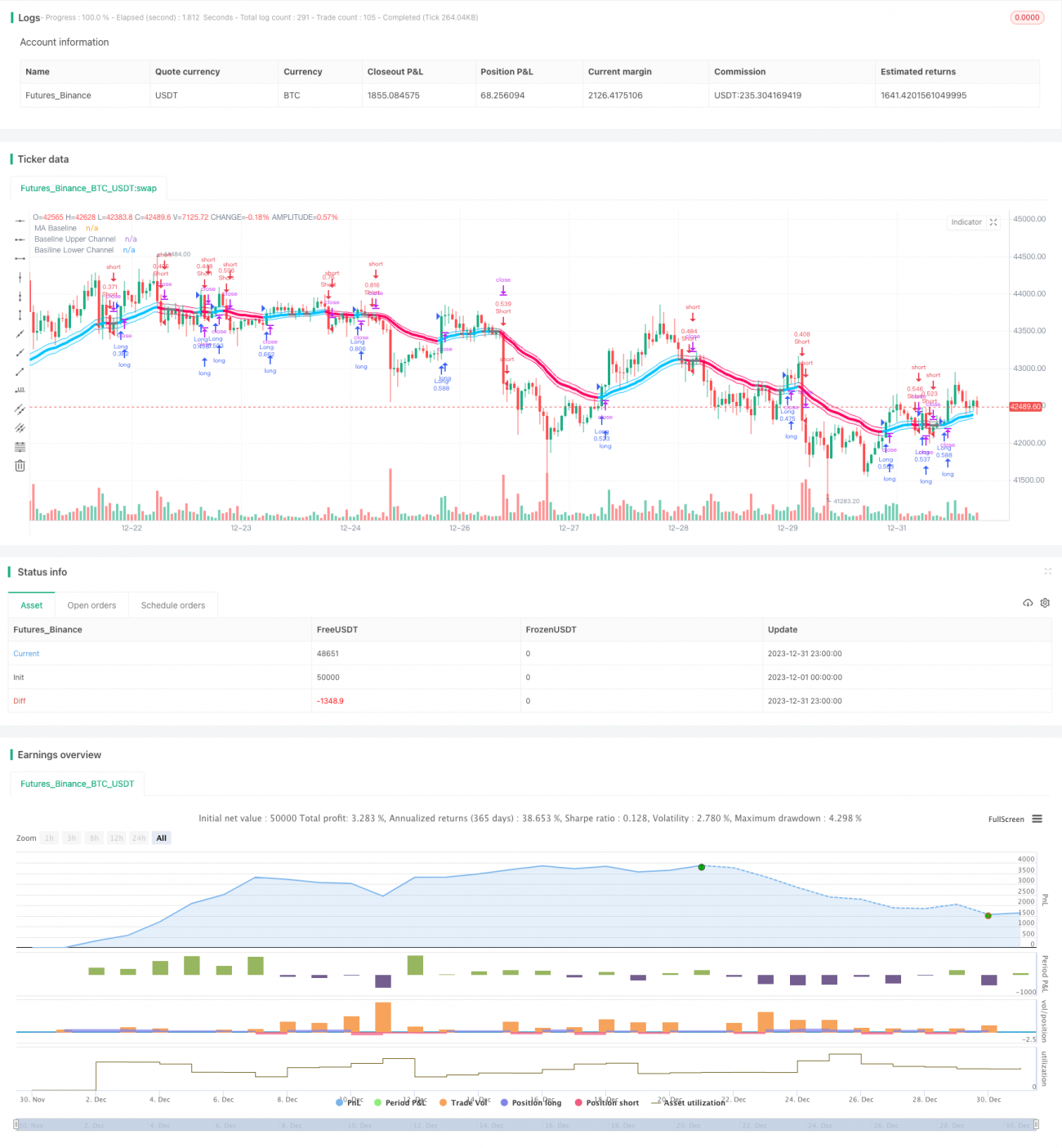

Esta estrategia utiliza el indicador de canal SSL para determinar la tendencia del mercado y realiza un seguimiento de tendencia basándose en una media móvil como referencia. Es adecuada para marcos temporales de 4 horas y diario en el mediano y largo plazo.

Principio de la Estrategia

-

El canal SSL está compuesto por la media móvil de Keltner y la amplitud real. Puede determinar la dirección de la tendencia del mercado. Cuando el precio supera la banda superior, es una señal alcista; cuando rompe la banda inferior, es una señal bajista.

-

La estrategia utiliza indicadores de media móvil como la EMA para calcular una línea de base. Esta línea de base puede filtrar algunas falsas rupturas.

-

La estrategia abre una posición larga cuando el precio supera la banda superior del SSL, y una posición corta cuando rompe la banda inferior. En una tendencia alcista, persigue las subidas y vende en las caídas; en una tendencia bajista, busca comprar en el fondo.

-

Los métodos de stop loss incluyen stop loss porcentual, stop loss basado en ATR y stop loss basado en el mínimo/máximo retrospectivo. El take profit es un múltiplo del stop loss. Los parámetros específicos son determinados por el usuario.

Análisis de Ventajas

-

El canal SSL determina la dirección de la tendencia con precisión, reduciendo las señales falsas. Combinado con la media móvil como base para la entrada, evita comprar en la parte superior y vender en la inferior.

-

Permite seleccionar de forma flexible diferentes tipos de medias móviles, adaptándose a una amplia variedad de condiciones de mercado.

-

Los métodos de stop loss son flexibles y diversos, permitiendo controlar el riesgo. El múltiplo de take profit también se puede ajustar de manera flexible para satisfacer diferentes preferencias.

-

Puede operar tanto en largo como en corto simultáneamente, aprovechando plenamente las oportunidades bidireccionales del mercado.

Análisis de Riesgos

-

Todos los indicadores de media móvil tienen rezago, lo que puede provocar una acumulación de pérdidas.

-

En mercados laterales, una ruptura de las bandas puede revertirse rápidamente, atrapando al operador.

-

Los stop losses basados en ATR y en retrospectiva pueden ser demasiado amplios en caso de rupturas anómalas, aumentando las pérdidas.

Medidas para abordar los riesgos:

- Ajustar adecuadamente los parámetros de la media móvil, o elegir otros tipos de medias móviles.

- Aumentar el margen del stop loss y realizar el corte a tiempo.

- Agregar un factor multiplicador al ATR o ajustar el período de retrospectiva.

Direcciones de Optimización

- Probar más tipos de indicadores de media móvil para encontrar los parámetros óptimos.

- Optimizar los parámetros del período ATR para el stop loss.

- Probar diferentes parámetros de múltiplo de stop loss.

- Probar diferentes coeficientes de riesgo para el take profit.

Conclusión

Esta estrategia combina el canal SSL para determinar la tendencia y los indicadores de media móvil para confirmar la entrada, logrando un seguimiento efectivo de la tendencia. Proporciona métodos flexibles de stop loss y take profit, obteniendo mayores rendimientos mientras controla el riesgo. Mediante pruebas continuas y optimización de parámetros, se puede lograr un mejor rendimiento en las operaciones. Es una estrategia eficaz que merece un seguimiento a largo plazo y su implementación.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Thanks to @kevinmck100 for opensource strategy template and @Mihkel00 for SSL Hybrid

// @fpemehd

// @version=5- 1