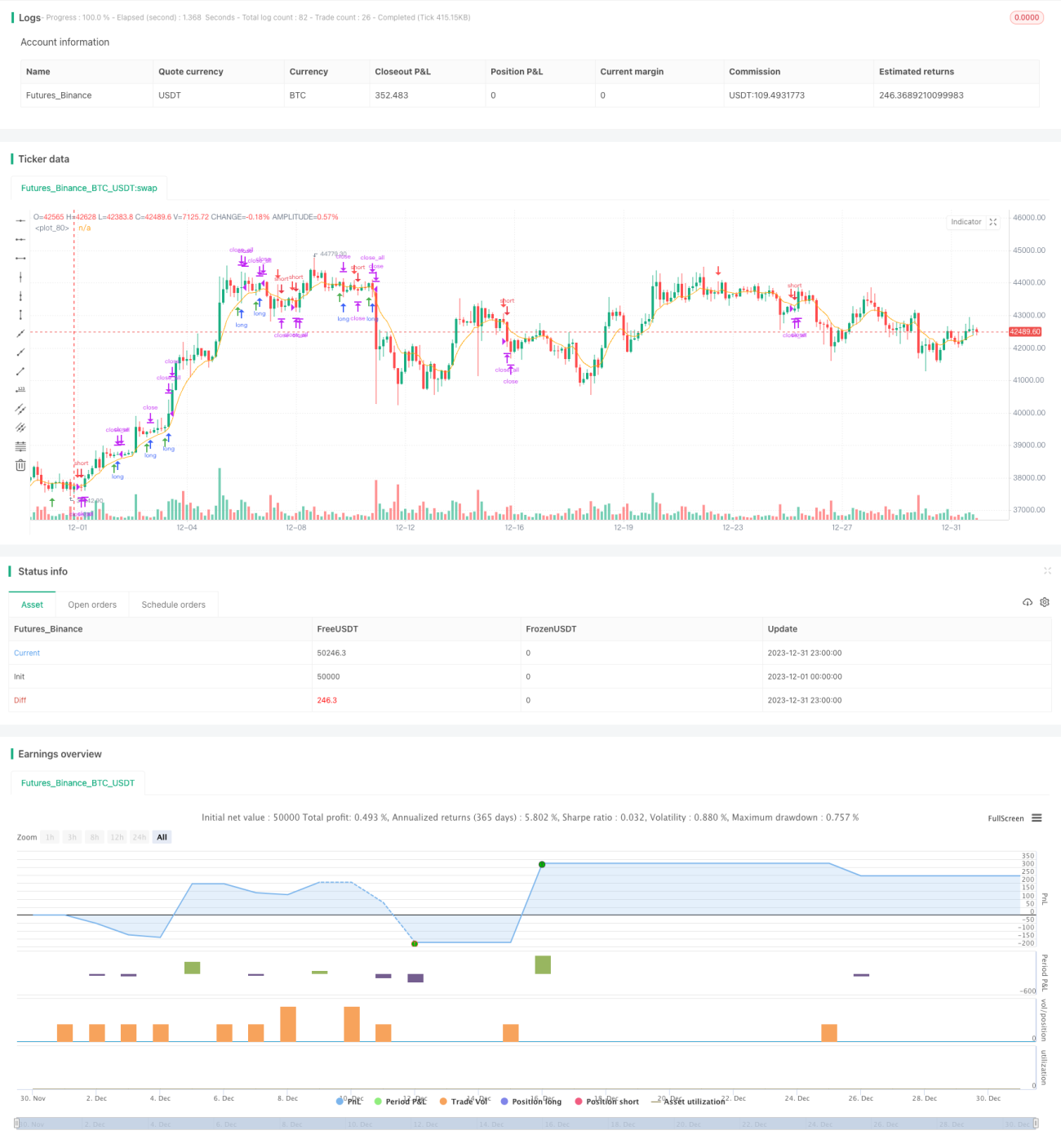

Estrategia de reversión de seguimiento de tendencia a corto plazo

Resumen

La estrategia de reversión de seguimiento de tendencia es una estrategia de trading de tendencia a corto plazo basada en futuros NQ en gráficos de 15 minutos. Identifica oportunidades de trading mediante el filtrado de tendencias y el reconocimiento de patrones de reversión. Esta estrategia es simple y efectiva, adecuada para traders activos de corto plazo.

Principio de la estrategia

El funcionamiento de esta estrategia se basa principalmente en los siguientes puntos:

-

Utiliza una EMA de 8 períodos como el principal filtro de tendencia. Por encima de la EMA se considera alcista; por debajo, bajista.

-

Identifica patrones específicos de velas de reversión como señales de entrada, incluyendo una señal alcista de una vela larga alcista seguida de una vela corta bajista, y una señal bajista de una vela larga bajista seguida de una vela corta alcista. Estos patrones sugieren que la tendencia puede estar comenzando a revertirse.

-

El punto de entrada se sitúa cerca del máximo o mínimo de la vela de reversión, y el stop loss se sitúa en el máximo o mínimo de la propia vela de reversión, logrando una relación riesgo-beneficio eficiente.

-

Utiliza la relación entre los cuerpos de las velas para determinar la validez de la señal de reversión, como que el precio de apertura de una vela bajista esté por encima del cuerpo de la vela anterior, o que el cuerpo esté completamente contenido, para filtrar el ruido.

-

Opera solo en períodos de cotización específicos, evitando períodos especiales como los cambios de contrato principales del mercado, para prevenir pérdidas innecesarias debido a movimientos anormales del mercado.

Análisis de ventajas

Esta estrategia tiene las siguientes ventajas principales:

-

Las señales de la estrategia son simples y efectivas, fáciles de entender e implementar.

-

Se basa en el juicio de tendencia y reversión, evitando ser atrapado tanto en mercados alcistas como bajistas.

-

El control de riesgos es adecuado, con un stop loss razonable que favorece la gestión del capital.

-

Requiere poca cantidad de datos, adecuada para varios tipos de software y plataformas.

-

La frecuencia de trading es relativamente alta, adecuada para inversores que prefieren el trading activo de corto plazo.

Riesgos y contramedidas

Esta estrategia también tiene algunos riesgos, principalmente:

-

Oportunidades insuficientes de patrones de reversión, con pocas señales. Se pueden relajar las reglas de juicio de reversión de manera apropiada.

-

Problemas ocasionales de falsas rupturas. Se pueden agregar más indicadores de filtro para un juicio conjunto.

-

Inestabilidad en sesiones nocturnas y horarios no principales. Se puede configurar para operar solo durante la sesión estadounidense.

-

Espacio limitado de optimización de parámetros. Se pueden probar técnicas como el aprendizaje automático para encontrar mejores parámetros.

Direcciones de optimización

Esta estrategia tiene cierto margen de mejora, principalmente en:

-

Probar parámetros de EMA de períodos más largos para mejorar el juicio de tendencia.

-

Agregar índices bursátiles principales como indicador adicional de filtro de tendencia.

-

Utilizar técnicas como el aprendizaje automático para optimizar automáticamente los puntos de entrada y stop loss.

-

Incorporar un mecanismo de ajuste dinámico del tamaño de posición y stop loss basado en la volatilidad.

-

Probar el arbitraje entre múltiples instrumentos para diversificar aún más el riesgo sistémico de un solo instrumento.

Conclusión

En general, la estrategia de reversión de seguimiento de tendencia es una idea de trading de corto plazo muy práctica, con parámetros simples y fácil de poner en práctica. Permite un buen control del riesgo personal, adecuada para traders activos de corto plazo en foros de inversión. Esta estrategia tiene cierto margen de optimización, y con una inversión adecuada en I+D, puede incluso adaptarse para su operación programática por parte de capitales de mediano y largo plazo, mostrando un buen potencial de desarrollo.

- 1