Estrategia de seguimiento de tendencia paciente

Resumen

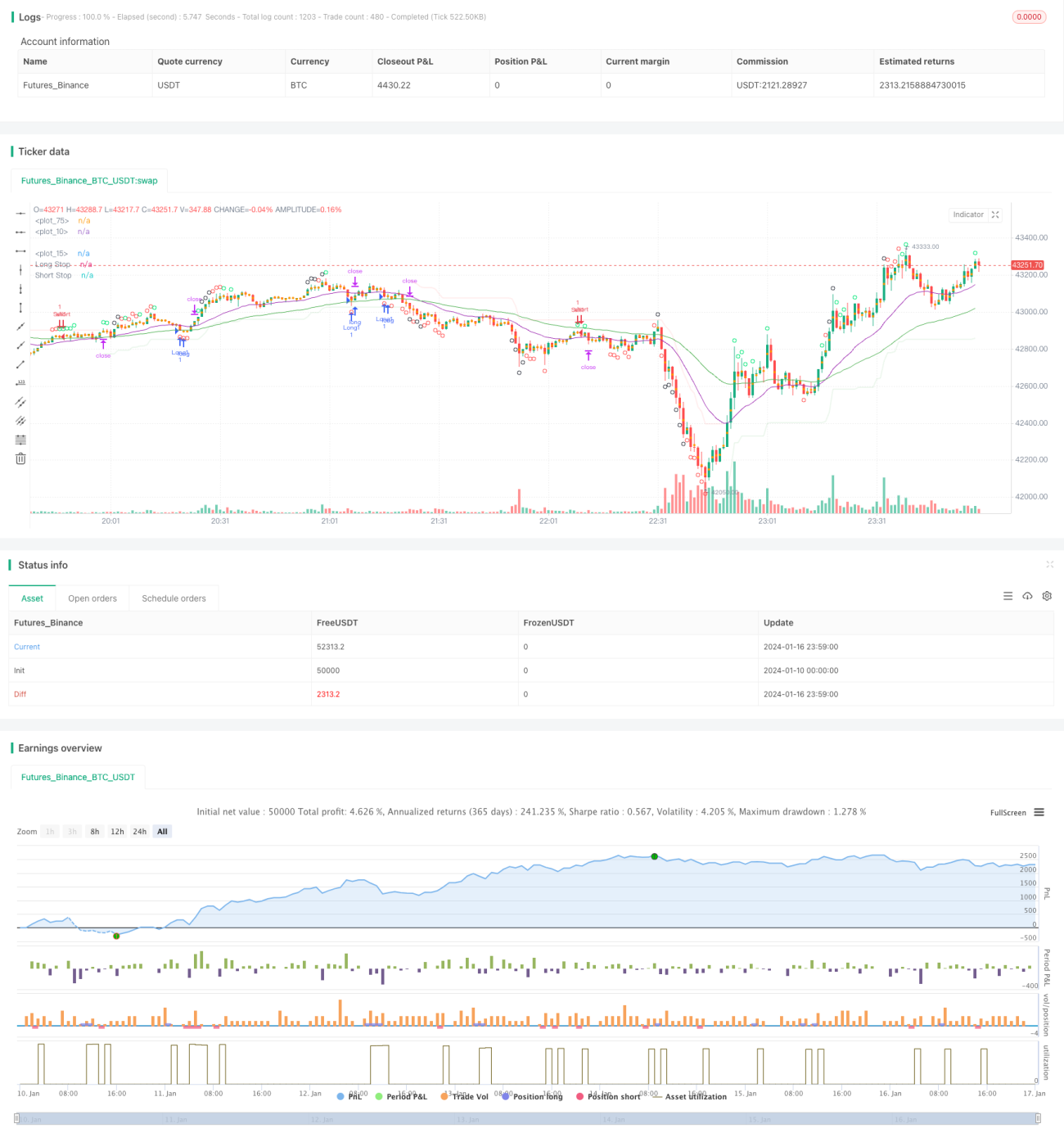

La estrategia de seguimiento de tendencia paciente es una estrategia de tipo seguidor de tendencia. Utiliza la combinación de indicadores de medias móviles para determinar la dirección de la tendencia y combina el indicador de sobrecompra/sobreventa CCI para generar señales de trading. La estrategia busca grandes tendencias y puede evitar eficazmente quedar atrapado en mercados laterales.

Principio de la estrategia

Esta estrategia utiliza la combinación de EMA de 21 y 55 periodos para determinar la dirección de la tendencia. Cuando la EMA de corto plazo está por encima de la EMA de largo plazo, se define como tendencia alcista; cuando la EMA de corto plazo está por debajo de la EMA de largo plazo, se define como tendencia bajista.

El indicador CCI se utiliza para determinar situaciones de sobrecompra/sobreventa. Cuando el CCI cruza al alza la línea de -100, es una señal de sobreventa en el suelo; cuando cruza a la baja la línea de 100, es una señal de sobrecompra en el techo. Según las diferentes líneas de sobrecompra/sobreventa del indicador CCI, la estrategia se divide en tres niveles de intensidad de señal de trading.

Cuando se determina una tendencia alcista, si el indicador CCI emite una señal fuerte de sobreventa en el suelo, se realiza una entrada larga. Cuando se determina una tendencia bajista, si el indicador CCI emite una señal fuerte de sobrecompra en el techo, se realiza una entrada corta.

El stop loss se establece con el indicador SuperTrend, y el beneficio objetivo se fija en un número fijo de puntos.

Análisis de ventajas

Las principales ventajas de esta estrategia son:

- Sigue las grandes tendencias, evitando quedar atrapado.

- El indicador CCI puede identificar eficazmente los puntos de reversión.

- El stop loss de SuperTrend está razonablemente configurado.

- Stop loss fijo y take profit fijo, riesgo controlable.

Análisis de riesgos

Los principales riesgos de esta estrategia son:

- Probabilidad de error en la determinación de la gran tendencia.

- Probabilidad de que el indicador CCI emita señales falsas.

- Probabilidad de que el stop loss sea demasiado ajustado o demasiado amplio, provocando pérdidas innecesarias.

- Probabilidad de que el take profit fijo no pueda seguir capturando ganancias de la tendencia de forma continua.

Para mitigar estos riesgos, podemos optimizar ajustando los parámetros de los periodos de EMA, los parámetros del CCI y los niveles de stop loss/take profit. También es necesario introducir más indicadores para verificar las señales de la estrategia.

Direcciones de optimización

Las principales direcciones de optimización de esta estrategia son:

- Probar más combinaciones de indicadores para encontrar mejores métodos de determinación de tendencia y verificación de señales.

- Utilizar stop loss y take profit dinámicos basados en ATR para seguir mejor la tendencia y controlar el riesgo.

- Introducir modelos de machine learning entrenados con datos históricos para determinar la probabilidad de la tendencia.

- Ajustar y optimizar los parámetros para diferentes instrumentos.

Resumen

La estrategia de seguimiento de tendencia paciente es, en general, una estrategia de seguimiento de tendencia muy práctica. Utiliza medias móviles para determinar la dirección de la gran tendencia, el indicador CCI para detectar señales de puntos de reversión, y el stop loss de SuperTrend está configurado de forma razonable. Mediante el ajuste de parámetros y la combinación de múltiples indicadores para su verificación, esta estrategia puede optimizarse aún más, y merece un seguimiento y verificación a largo plazo en operaciones reales.

- 1