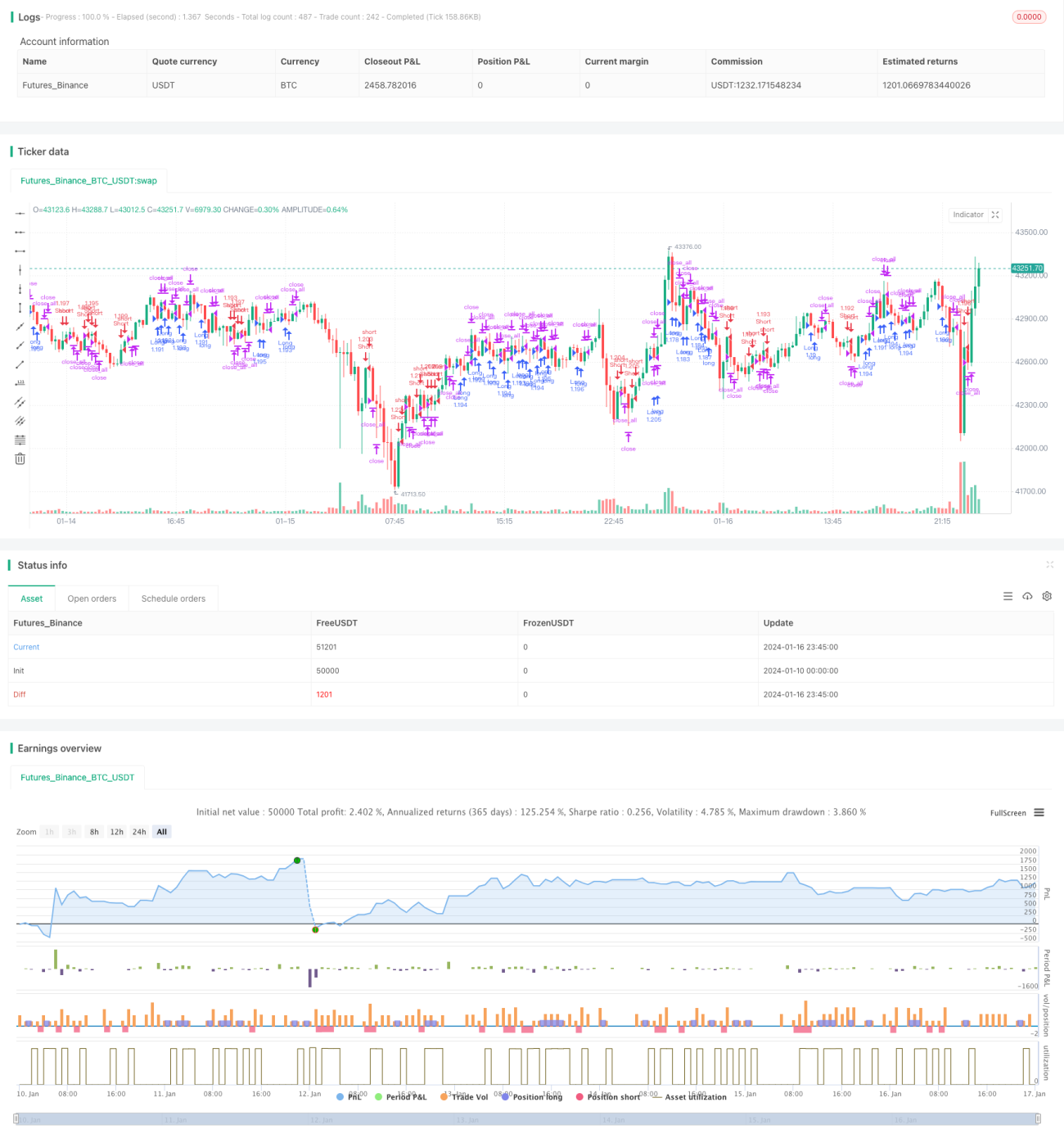

Estrategia de trading cuantitativa de ruptura de doble RSI

Resumen

La estrategia de ruptura doble RSI es una estrategia de trading cuantitativo que utiliza simultáneamente los indicadores RSI rápido y RSI lento para generar señales de trading. Esta estrategia forma señales de trading a través de la ruptura entre los dos indicadores RSI (rápido y lento), logrando así el seguimiento de las tendencias del mercado.

Principio de la estrategia

La estrategia utiliza dos indicadores RSI al mismo tiempo: un RSI rápido con período 2 y un RSI lento con período 14. Las señales de trading se generan a partir de la ruptura entre los dos indicadores RSI.

Cuando el RSI lento es mayor que 50 y el RSI rápido es menor que 50, se genera una señal de compra (largo). Cuando el RSI lento es menor que 50 y el RSI rápido es mayor que 50, se genera una señal de venta (corto). Después de abrir una posición larga o corta, si aparece una señal de stop loss (barra de vela roja cuando la posición larga está en pérdidas, o barra de vela verde cuando la posición corta está en pérdidas), se cierra la posición para detener la pérdida.

Análisis de ventajas

- Utiliza las características de sobrecompra y sobreventa del indicador RSI para generar señales, evitando comprar en máximos y vender en mínimos.

- La combinación de RSI rápido y lento permite seguir los cambios de tendencia del mercado, logrando entradas y salidas oportunas.

- Sigue tendencias de mediano y largo plazo, evitando interferencias del ruido del mercado a corto plazo.

- Control de riesgos adecuado, con un mecanismo de stop loss.

Riesgos y soluciones

- Riesgo de ruptura falsa. La solución es establecer parámetros adecuados para el RSI rápido y lento, asegurando rupturas reales.

- Riesgo por una colocación inadecuada del stop loss. La solución es fijar la distancia del stop loss de forma razonable según la volatilidad del mercado.

- Riesgo de pérdidas en espiral. La solución es no perseguir precios altos ni vender en mínimos, y seguir estrictamente las reglas de la estrategia para entradas y salidas.

Direcciones de optimización

La estrategia también se puede optimizar en los siguientes aspectos:

- Optimizar los parámetros del RSI rápido y lento para encontrar la mejor combinación.

- Incorporar otros indicadores en combinación para generar señales de trading más fiables.

- Establecer un stop loss dinámico, ajustando el punto de stop loss en tiempo real según la volatilidad del mercado.

Resumen

La estrategia de ruptura doble RSI utiliza los indicadores RSI rápido y lento para seguir los cambios de tendencia del mercado, generando señales de trading en zonas de sobrecompra y sobreventa, lo que permite evitar eficazmente comprar en máximos y vender en mínimos. Además, cuenta con un mecanismo de stop loss para controlar el riesgo. Esta estrategia es simple de operar y fácil de implementar, adecuada para el trading cuantitativo. Mediante la optimización de parámetros, la combinación de indicadores, etc., se puede mejorar aún más el factor de beneficio de la estrategia.

- 1