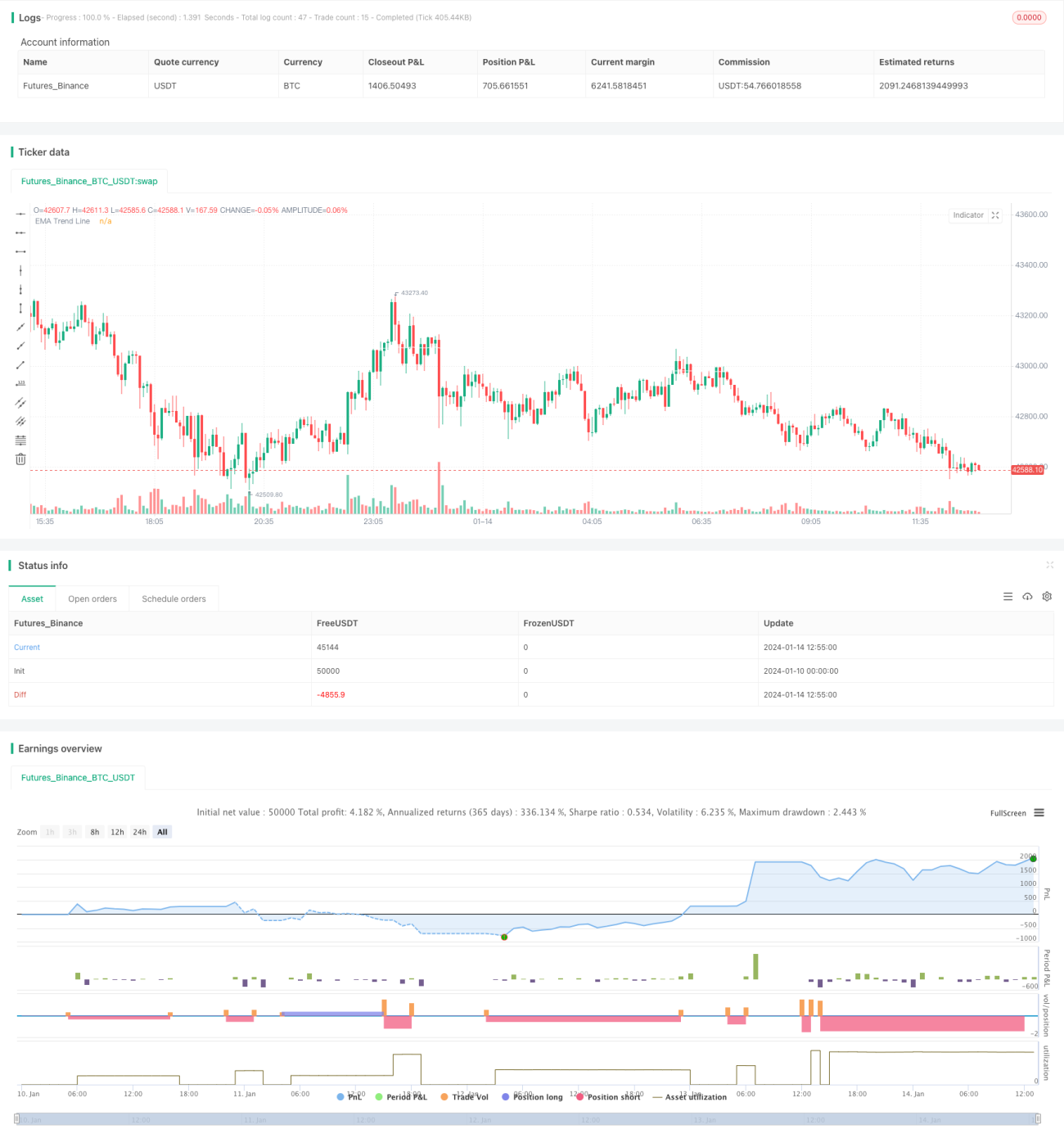

Estrategia de seguimiento de tendencia combinando doble EMA y RSI

Resumen

Esta estrategia combina el uso de doble EMA y el indicador RSI para identificar tendencias de precios y entrar en el mercado oportunamente cuando se produce un giro en la dirección de la tendencia. Específicamente, la estrategia utiliza una EMA de período más largo para determinar la dirección general de la tendencia, mientras que el RSI se emplea para identificar condiciones de sobrecompra y sobreventa a corto plazo. Cuando el precio retrocede en la dirección de la tendencia principal, se genera una señal de trading mediante el RSI, abriendo posiciones largas o cortas según la dirección de la tendencia.

Principio de la Estrategia

-

Se utiliza una EMA de 200 períodos para determinar la dirección general de la tendencia. Un cruce del precio por encima de la línea EMA indica una señal alcista, y por debajo, una señal bajista.

-

El parámetro del RSI se establece en 10 períodos. Un cruce del RSI por encima de 40 indica una señal de sobreventa, y por debajo de 60, una señal de sobrecompra.

-

Cuando la tendencia general es alcista (el precio está por encima de la línea EMA), si el RSI cruza por debajo de 40 (señal de sobreventa), se abre una posición larga.

-

Cuando la tendencia general es bajista (el precio está por debajo de la línea EMA), si el RSI cruza por encima de 60 (señal de sobrecompra), se abre una posición corta.

-

El stop loss se establece en 4 veces el ATR. El take profit se fija en 2 veces el stop loss, logrando una relación riesgo-recompensa de 2:1.

Análisis de Ventajas

La mayor ventaja de esta estrategia es que combina indicadores de tendencia y de reversión, permitiendo entrar en el mercado cuando se produce un retroceso dentro de la tendencia, lo que puede generar un buen rendimiento. Las ventajas específicas son:

-

El sistema de doble EMA permite determinar la dirección principal de la tendencia, lo que facilita el seguimiento de la tendencia del precio.

-

El RSI puede identificar condiciones de sobrecompra y sobreventa a corto plazo, ayudando a determinar el momento de entrada.

-

El stop loss se basa en el ATR, lo que permite ajustar la amplitud del stop loss según la volatilidad del mercado, favoreciendo el control del riesgo.

-

Al seguir estrictamente los principios del trading de tendencias, se reducen las operaciones innecesarias y se minimiza el riesgo sistémico.

Análisis de Riesgos

Los principales riesgos de esta estrategia son:

-

Durante períodos de tendencia lateral o debilitamiento, pueden generarse señales de trading erróneas. En estos casos, es necesario evaluar la situación con prudencia y entrar con cautela.

-

En condiciones extremas del mercado, el stop loss basado en ATR puede ser demasiado amplio o demasiado ajustado, por lo que requiere un ajuste dinámico. También se puede considerar reemplazarlo por otros métodos de stop loss.

-

La frecuencia de las señales de trading puede ser alta, por lo que se debe verificar si se ajusta a las preferencias de frecuencia de trading del operador.

-

Es necesario verificar si el parámetro del RSI es adecuado y realizar una optimización periódica de los parámetros.

Direcciones de Optimización

Las principales áreas de optimización de esta estrategia son:

-

Se puede probar la inclusión de otros indicadores de tendencia, como MACD, para ayudar a determinar la dirección de la tendencia.

-

Se pueden probar otros indicadores de reversión, como KDJ o Bandas de Bollinger, combinados con el RSI para buscar mejores señales de trading.

-

Se puede introducir algoritmos de aprendizaje automático para ajustar los parámetros de forma adaptativa y lograr un stop loss y take profit dinámicos.

-

Se pueden considerar factores adicionales como indicadores de sentimiento o noticias para mejorar la solidez general del sistema.

Resumen

En general, esta estrategia es un típico sistema de trading a corto plazo que combina el seguimiento de tendencia con indicadores de reversión. Utiliza la doble EMA para identificar la tendencia principal y aprovecha las características de reversión del RSI para capturar oportunidades de pullback dentro de la tendencia. En principio, la estrategia integra las ventajas de diferentes indicadores, formando un efecto complementario. Si se mejora posteriormente mediante optimización de parámetros, fusión de modelos, etc., el rendimiento de esta estrategia tiene un gran potencial de mejora.

- 1