Estrategia Grid de Rango Oscilante con Beneficio

Resumen

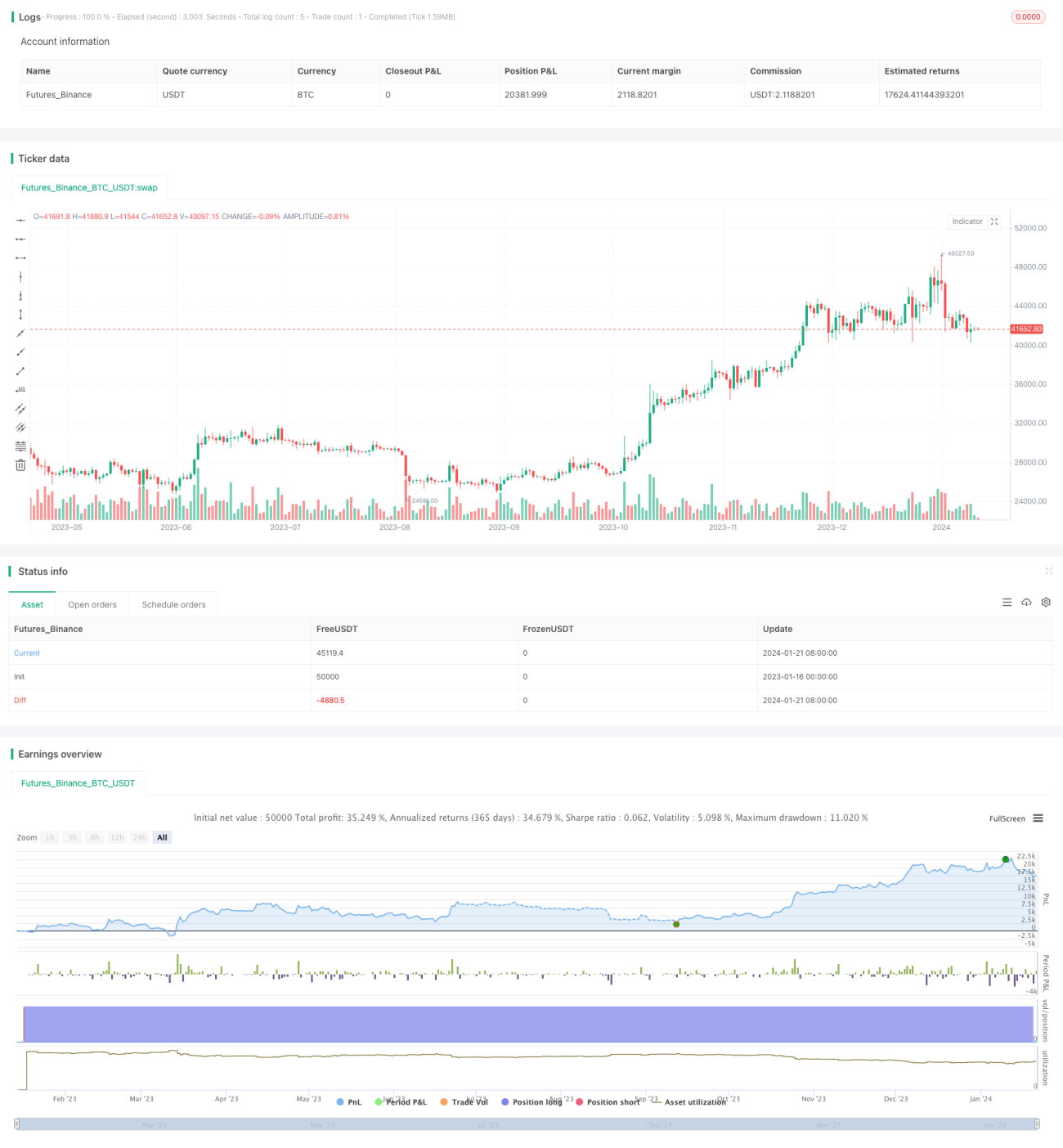

La estrategia Grid de Bandas de Ganancias por Oscilación es una estrategia de seguimiento de tendencia que establece automáticamente una cuadrícula basada en las fluctuaciones del precio, permitiendo obtener ganancias sostenidas durante los movimientos del precio.

Principio de la estrategia

El concepto central de esta estrategia es construir una cuadrícula de bandas de precios. Cuando el precio entra en diferentes bandas, se generan nuevas señales de trading. Por ejemplo, si el espaciado de la cuadrícula se establece en 500 USD, cuando el precio suba más de 500 USD se generará una nueva señal de compra.

Específicamente, la estrategia desplaza constantemente la cuadrícula siguiendo los nuevos máximos o mínimos del precio. En el código, definimos una variable re_grid para almacenar el nivel de cuadrícula actual. Cada vez que el precio supera este nivel en más del espaciado de cuadrícula establecido, se recalcula el siguiente nivel de cuadrícula.

De esta manera, cuando el precio experimenta fluctuaciones suficientemente grandes, se generan nuevas señales de trading, y podemos beneficiarnos tanto de posiciones largas como cortas. Cuando el precio comienza a moverse en dirección opuesta superando el espaciado de la cuadrícula, las posiciones originales se cierran con stop loss.

Análisis de ventajas

La mayor ventaja de esta estrategia es que puede seguir automáticamente la tendencia del precio y generar ganancias de forma continua. Mientras el precio mantenga fluctuaciones lo suficientemente grandes, el tamaño de nuestras posiciones aumentará y las ganancias serán cada vez mayores.

Además, al ajustar adecuadamente los parámetros de la cuadrícula, se puede controlar el riesgo de manera efectiva. Asimismo, combinarla con indicadores técnicos como la Nube Ichimoku para filtrar señales puede mejorar la estabilidad de la estrategia.

Análisis de riesgos

El principal riesgo de esta estrategia es que el precio pueda revertirse repentinamente, provocando un stop loss. En ese caso, las ganancias acumuladas anteriormente podrían reducirse o convertirse en pérdidas.

Para controlar este riesgo, podemos establecer líneas de stop loss, ajustar razonablemente los parámetros de la cuadrícula, seleccionar instrumentos con tendencias más fuertes y combinar múltiples indicadores técnicos para filtrar señales.

Direcciones de optimización

Podemos continuar optimizando esta estrategia desde los siguientes aspectos:

-

Optimizar los parámetros de la cuadrícula para encontrar la mejor combinación de espaciado, tamaño de posición, etc.

-

Agregar o ajustar mecanismos de stop loss para controlar mejor el riesgo.

-

Probar diferentes instrumentos de trading, seleccionando aquellos con mayor volatilidad y tendencias más claras.

-

Incorporar más indicadores técnicos para mejorar la estabilidad de la estrategia.

Conclusión

La estrategia Grid de Bandas de Ganancias por Oscilación, al establecer una cuadrícula de precios para seguir automáticamente la tendencia, puede generar ganancias sostenidas de manera efectiva. Sin embargo, también conlleva cierto riesgo de retroceso. Mediante la optimización de parámetros, el establecimiento de stops, la selección de instrumentos y otros métodos, se puede controlar eficazmente el riesgo y mejorar la estabilidad de la estrategia.

- 1