Estrategia de medias móviles paralelas y medias móviles de respuesta al impulso infinita

Resumen

Esta es una estrategia cuantitativa que combina el uso de medias móviles, medias móviles de respuesta infinita (IIR) y medias móviles lineales adaptativas (ALMA). La estrategia cuenta con múltiples combinaciones de indicadores que pueden proporcionar señales de trading abundantes para los operadores.

Principio de la estrategia

La estrategia se compone principalmente de las siguientes partes:

-

Utilizar en paralelo la media móvil simple (SMA), ALMA y IIR, detectando las señales de cruce entre ellas como momentos de entrada en las operaciones.

-

Utilizar tres IIR de diferentes períodos, midiendo la distancia entre ellas para determinar si el precio se encuentra en un estado de compresión. El estado de compresión indica una disminución de la volatilidad, lo que a menudo presagia un movimiento significativo del precio.

-

Evaluar la pendiente de las IIR; cuando la pendiente sube, se muestra en verde, y cuando baja, en azul. Esto permite visualizar intuitivamente la tendencia de las IIR.

-

Calcular si la distancia entre las SMA se está ampliando; de ser así, se marca de forma especial como expansión en "abanico", lo que generalmente indica que el precio ha entrado en una fase de tendencia.

-

Combinar las señales de sobrecompra y sobreventa del índice de fuerza relativa (RSI) para complementar las señales de trading.

Mediante la combinación de las partes anteriores, la estrategia puede proporcionar señales de entrada, juicio y salida relativamente completas y enriquecidas.

Análisis de ventajas de la estrategia

La mayor ventaja de esta estrategia radica en la combinación completa y rica de indicadores, que considera tanto el juicio de tendencia como la volatilidad y el estado de sobrecompra/sobreventa, ofreciendo una referencia multidimensional para la toma de decisiones de trading.

Otra ventaja es que los parámetros e indicadores son fáciles de ajustar y optimizar, permitiendo a los usuarios habilitar los indicadores y parámetros relevantes según sus necesidades.

Desde el punto de vista de la gestión de riesgos, la estrategia presta atención tanto a las medias rápidas como a las lentas, lo que puede reducir la probabilidad de señales falsas causadas por oscilaciones de precios.

Análisis de riesgos

Los principales riesgos de esta estrategia son:

-

Demasiada complejidad, que puede provocar conflictos entre indicadores; bajo ciertas combinaciones de parámetros, podría generar sobreajuste.

-

Al utilizar múltiples sistemas de medias móviles, aún es posible sufrir pérdidas significativas durante cambios bruscos del mercado (como eventos económicos importantes).

-

Un backtesting insuficiente puede implicar cierto riesgo de sesgo de supervivencia en la práctica real.

Durante la aplicación, debemos prestar atención a la gestión de riesgos, ajustar adecuadamente el tamaño de las posiciones y realizar múltiples backtests en períodos de tiempo más largos y conjuntos de datos más amplios para garantizar la efectividad práctica de la estrategia.

Direcciones de optimización de la estrategia

Dado que la combinación de indicadores de esta estrategia es relativamente compleja y tiene muchos parámetros, se puede optimizar desde los siguientes aspectos:

-

Simplificar la selección de indicadores, eliminando aquellos con baja correlación o conflictivos.

-

Optimizar la selección de las medias IIR, eligiendo longitudes que se adapten mejor a las características del mercado.

-

Optimizar la combinación de medias rápidas y lentas para mejorar la estabilidad de las señales de cruce.

-

Incorporar modelos de aprendizaje automático como ayuda para el juicio, mejorando la capacidad adaptativa de la estrategia.

-

Optimizar la correlación con índices globales para aumentar la tasa de acierto en la determinación de tendencias.

Conclusión

Mediante la combinación flexible y optimización de indicadores, esta estrategia puede reflejar de manera completa el estado del mercado, ofreciendo un soporte multidimensional para la toma de decisiones de trading. Sin embargo, también existen ciertos riesgos de sobreajuste en la práctica. Debemos seguir optimizando y ajustando la estrategia en la práctica para adaptarnos a los cambios del mercado.

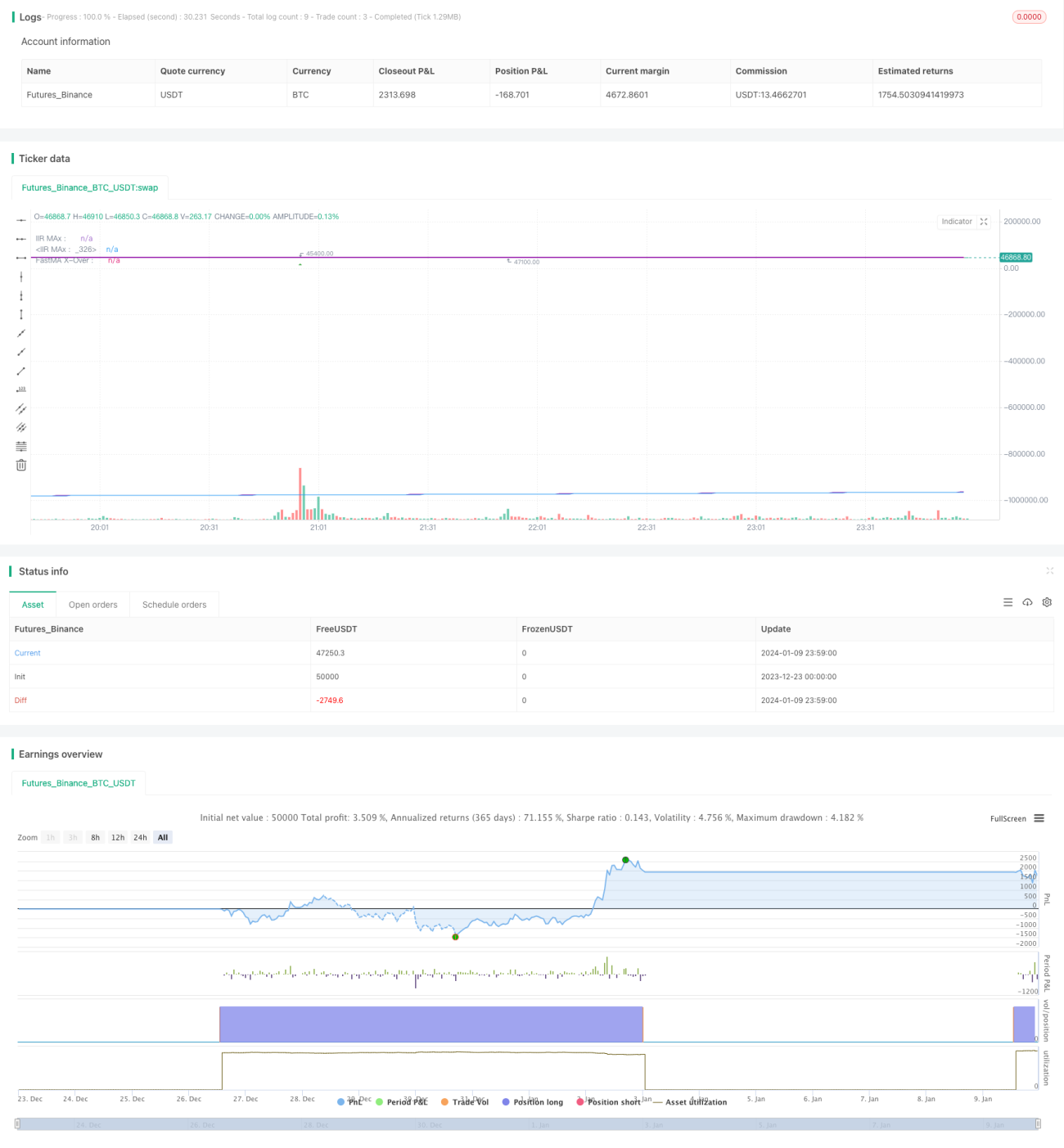

/*backtest

start: 2023-12-23 00:00:00

end: 2024-01-10 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//The plotchar UP/DOWN Arrows is the crossover of the fastest MA and fastest IIR MAs

//

//The dots at the bottom are the two simple averages crossing over

//- 1