Estrategia de trailing stop-loss inteligente

Descripción general

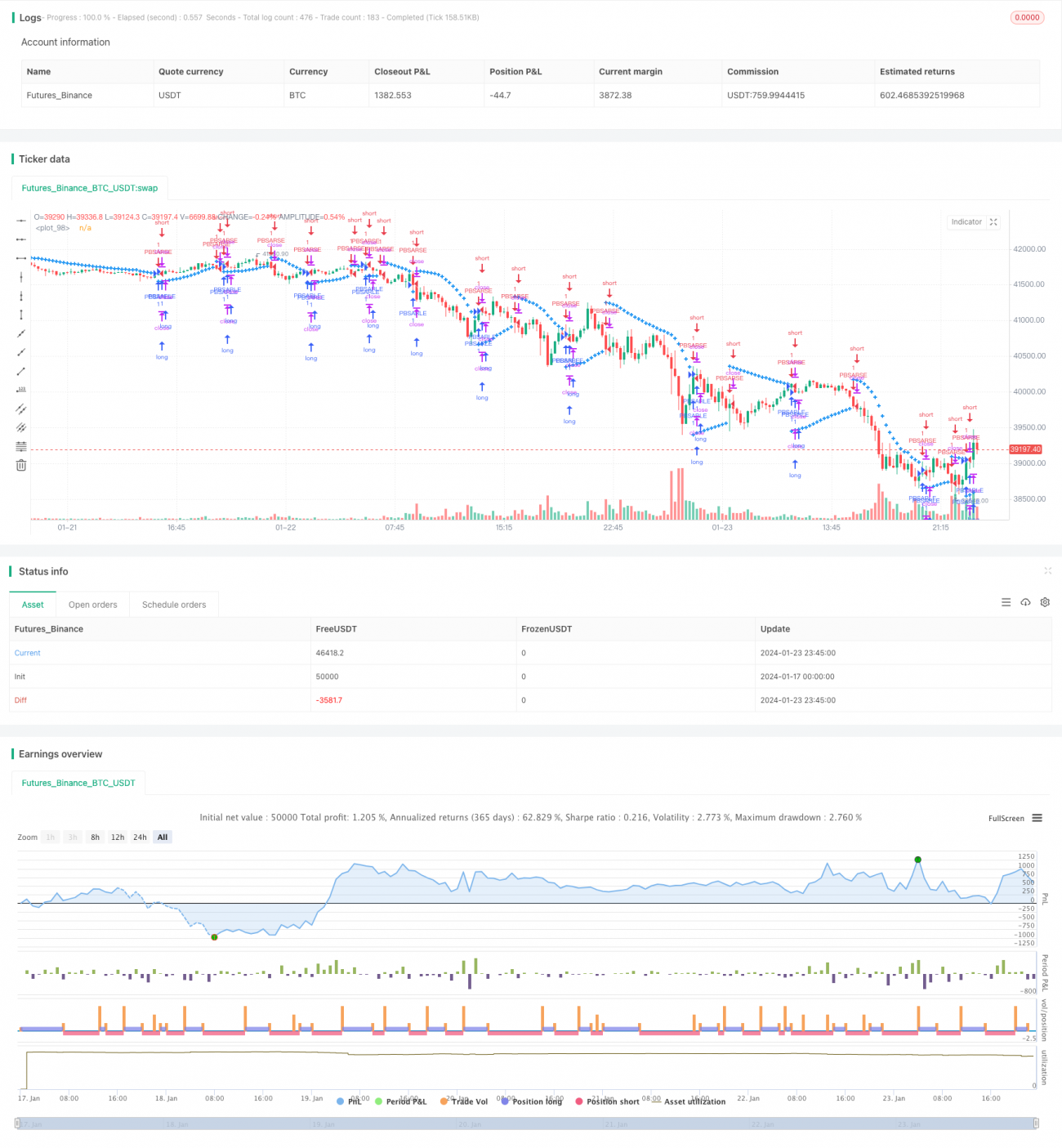

La Estrategia de Stop Loss Trailing Inteligente (Intelligent Trailing Stop Loss Strategy) es una estrategia que ajusta automáticamente el nivel de stop loss en función de los cambios de precio. Combina la lógica del indicador SAR y, cuando el precio alcanza un nuevo máximo o mínimo, ajusta la línea de stop loss de forma dinámica para controlar la máxima reducción.

Principio de la estrategia

El núcleo de esta estrategia consiste en ajustar automáticamente el nivel de stop loss según el indicador SAR. En concreto, define 4 variables:

- EP: punto extremo

- SAR: nivel de stop loss actual

- AF: factor de aceleración, que controla la amplitud del ajuste del stop loss

- Señal de tendencia alcista: indica si la tendencia actual es alcista o bajista

En una tendencia alcista, el stop loss se eleva continuamente para seguir el aumento del precio; cuando el precio gira a la baja, el stop loss se mantiene sin cambios hasta que la tendencia vuelve a ser alcista.

La amplitud del ajuste del stop loss se controla mediante el factor de aceleración AF. El AF aumenta cuando se logra fijar un nuevo punto de stop loss, lo que amplía la magnitud del siguiente ajuste.

Ventajas de la estrategia

La mayor ventaja de esta estrategia es que puede ajustar inteligentemente el nivel de stop loss según la volatilidad del mercado, garantizando suficiente margen de beneficio y minimizando al mismo tiempo la máxima reducción. En comparación con los métodos tradicionales de stop loss estático, captura mejor las tendencias de los precios.

En concreto, presenta las siguientes ventajas:

- Reducción de la máxima reducción: el ajuste inteligente del stop loss permite salir antes de que la tendencia se revierta, protegiendo al máximo los beneficios ya obtenidos.

- Captura de tendencias: el stop loss se ajusta a medida que se alcanzan nuevos máximos o mínimos, siguiendo automáticamente la tendencia del precio.

- Parámetros personalizables: el usuario puede definir el valor del paso del AF y su valor inicial según su tolerancia al riesgo, controlando la sensibilidad del ajuste del stop loss.

Análisis de riesgos

La estrategia también presenta algunos riesgos que deben tenerse en cuenta:

- Demasiada sensibilidad: si el paso del AF es demasiado grande o el valor inicial demasiado pequeño, la línea de stop loss será excesivamente sensible, pudiendo activarse por ruido de mercado a corto plazo.

- Oportunidades perdidas: una activación demasiado temprana del stop loss puede provocar la pérdida de oportunidades de ganancias posteriores si el precio continúa subiendo.

- Selección de parámetros: un ajuste incorrecto de los parámetros también afecta la eficacia de la estrategia; es necesario adaptarlos a los diferentes mercados.

Direcciones de optimización

La estrategia puede optimizarse en los siguientes aspectos:

- Combinación con otros indicadores: se puede pausar el ajuste del stop loss cuando un indicador de marco temporal superior emite una señal, evitando un stop loss prematuro antes de una reversión de tendencia.

- Inclusión de un módulo de parámetros adaptativos: se puede utilizar un algoritmo de aprendizaje automático para optimizar automáticamente los parámetros basándose en datos históricos.

- Stop loss multinivel: se pueden establecer múltiples líneas de stop loss para seguir las fluctuaciones del mercado en diferentes amplitudes.

Resumen

La Estrategia de Stop Loss Trailing Inteligente simula la lógica de funcionamiento del indicador SAR, ajustando en tiempo real la posición del stop loss. Protege los beneficios al mismo tiempo que minimiza la posibilidad de perder oportunidades. Maximiza el valor inherente de la función de stop loss.

En comparación con las estrategias tradicionales de stop loss fijo, esta estrategia se adapta mejor y de forma más flexible a los cambios del mercado. Mediante la personalización de parámetros, cada usuario puede elegir el modo de stop loss más adecuado a su tolerancia al riesgo.

Por supuesto, la estrategia también deja margen para la optimización de parámetros y puede mejorar su rendimiento al combinarla con otros indicadores. En general, encuentra un punto de equilibrio más inteligente entre el stop loss y la toma de ganancias para los inversores.

/*backtest

start: 2024-01-17 00:00:00

end: 2024-01-24 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Lucid SAR Strategy", shorttitle="Lucid SAR Strategy", overlay=true)

// Full credit to Sawcruhteez, Lucid Investment Strategies LLC and Casey Bowman.- 1