Estrategia de seguimiento de tendencia del petróleo crudo basada en el indicador ADX

Resumen

Esta estrategia está adaptada de la estrategia gratuita de futuros de petróleo crudo de Kevin Davey. Utiliza el indicador ADX para evaluar la tendencia del mercado del petróleo crudo y combina el principio de ruptura de precios para implementar una estrategia de trading automático simple y práctica para el petróleo crudo.

Principio de la Estrategia

- Calcular el indicador ADX de 14 períodos.

- Cuando ADX > 10, se considera que el mercado tiene tendencia.

- Si el precio de cierre es más alto que el de hace 65 velas, indica una ruptura alcista, señal de posición larga.

- Si el precio de cierre es más bajo que el de hace 65 velas, indica una ruptura bajista, señal de posición corta.

- Después de entrar, se establecen stop loss y take profit.

La estrategia se basa principalmente en el ADX para determinar la tendencia y, en presencia de tendencia, genera señales de trading mediante la ruptura de precios en un período fijo. La lógica completa es muy simple y clara.

Análisis de Ventajas de la Estrategia

- Al usar ADX para identificar la tendencia, se evita perder oportunidades de tendencia.

- La ruptura de precios en un período fijo genera señales, con buenos resultados en backtesting.

- El código es intuitivo y simple, fácil de entender y modificar.

- Ha sido validado por Kevin Davey en trading real durante muchos años, sin sobreajuste.

Análisis de Riesgos de la Estrategia

- El ADX como indicador principal es sensible a la selección de parámetros y al período de ruptura.

- La ruptura de período fijo puede perder algunas oportunidades.

- Un mal ajuste de stop loss y take profit puede aumentar las pérdidas.

- Puede haber diferencias entre los resultados en backtesting y el trading real.

Direcciones de Optimización de la Estrategia

- Optimizar los parámetros del ADX y el período de ruptura.

- Agregar ajuste dinámico del tamaño de la posición.

- Mejorar continuamente la estrategia basándose en resultados de backtesting y validación en vivo.

- Introducir técnicas de machine learning y deep learning para la optimización de la estrategia.

Conclusión

En general, esta estrategia es una estrategia de trading de petróleo crudo muy práctica. Utiliza el ADX para determinar la tendencia de manera muy razonable, el principio de ruptura de precios es simple y efectivo, y los resultados del backtesting son buenos. Además, como estrategia gratuita y pública de Kevin Davey, tiene una alta fiabilidad en la práctica. Aunque la estrategia tiene margen de mejora, para principiantes y traders con poco capital, es una opción muy adecuada para comenzar y practicar.

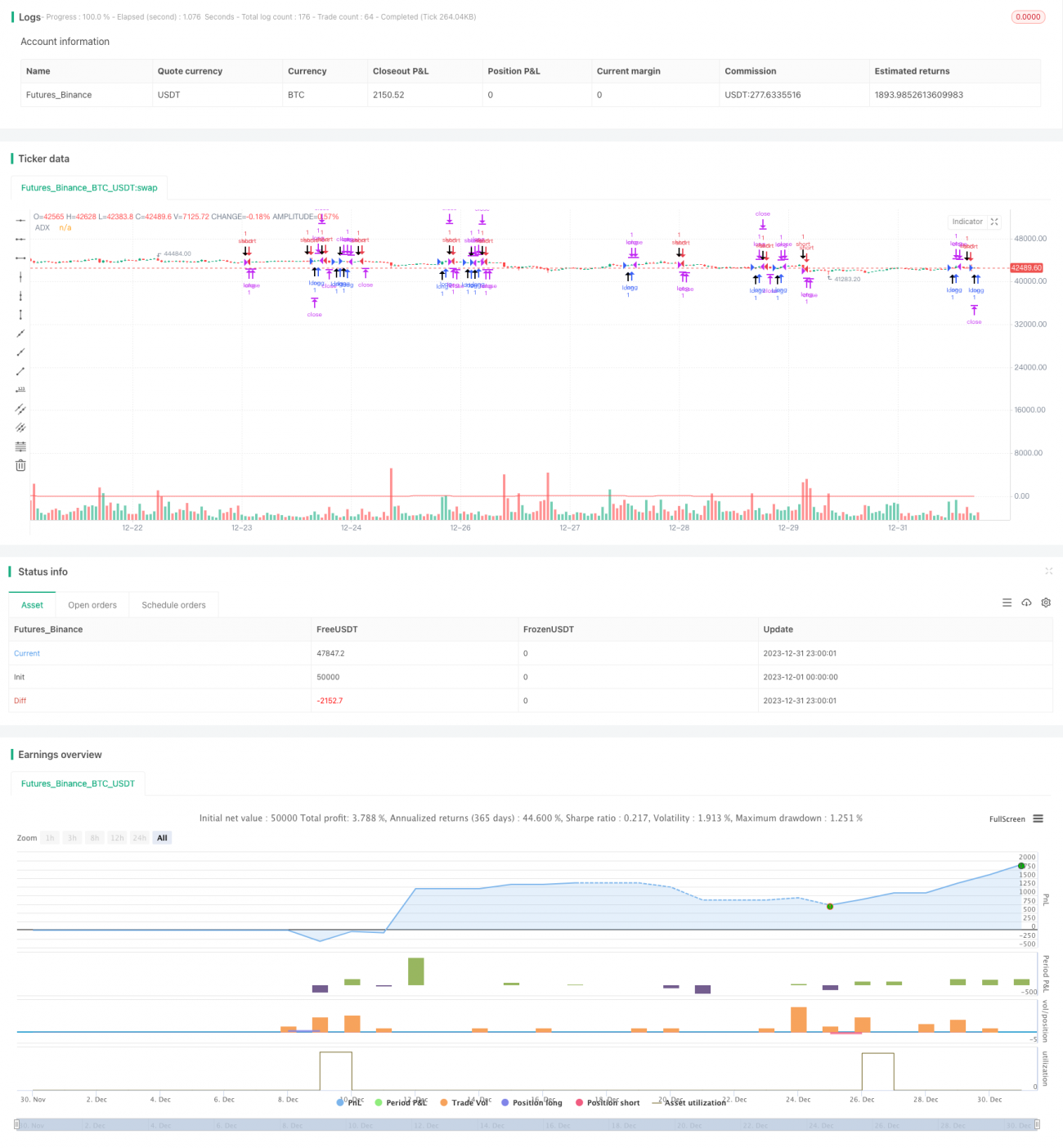

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// Strategy idea coded from EasyLanguage to Pinescript

//@version=5

strategy("Kevin Davey Crude free crude oil strategy", shorttitle="CO Fut", format=format.price, precision=2, overlay = true, calc_on_every_tick = true)

adxlen = input(14, title="ADX Smoothing")- 1