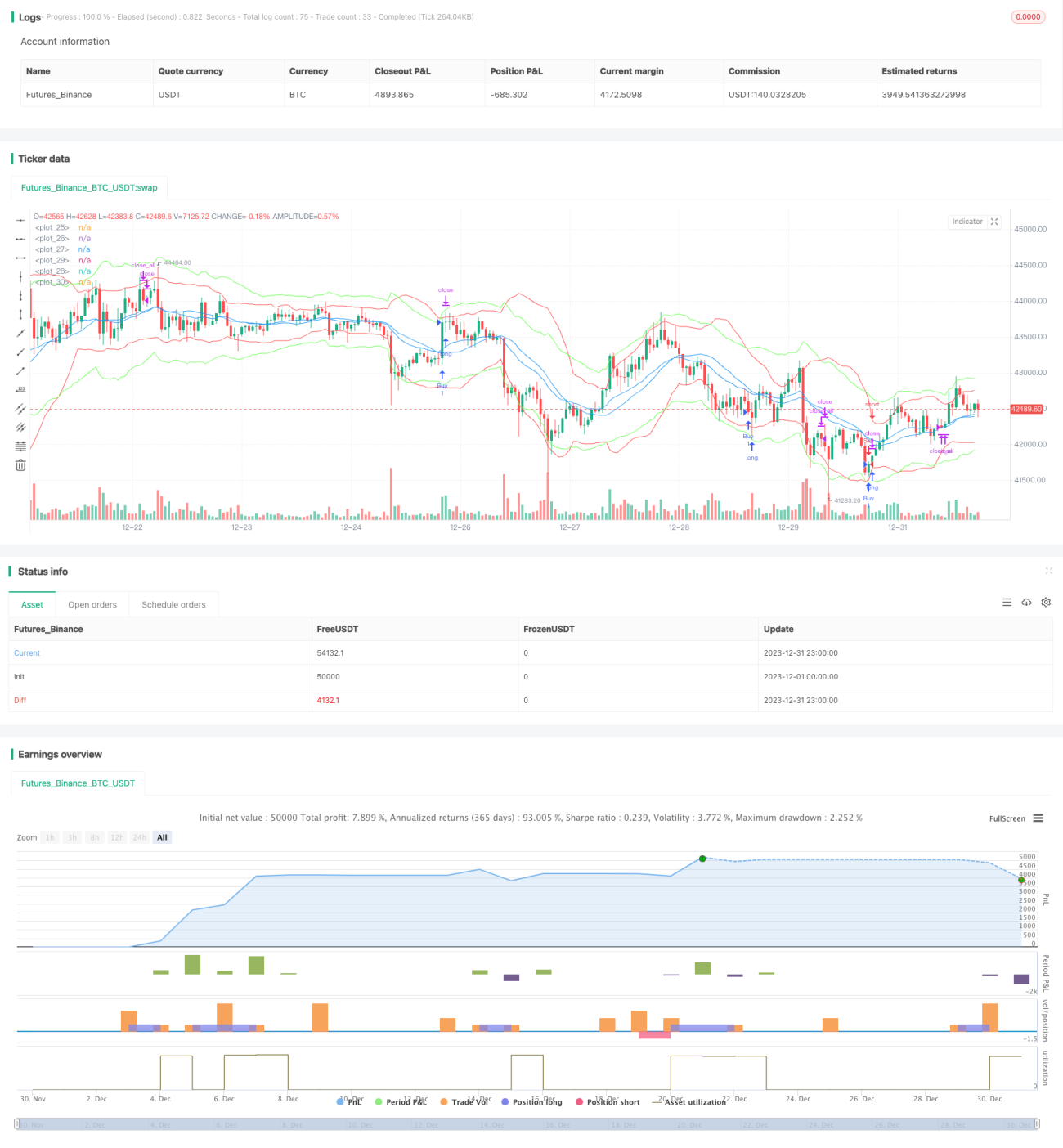

Estrategia de tendencia progresiva BB KC

Resumen

Esta estrategia combina las Bandas de Bollinger y el indicador Keltner para identificar tendencias del mercado. Las Bandas de Bollinger son una herramienta de análisis técnico que define canales basados en el rango de fluctuación del precio; el indicador Keltner combina la volatilidad del precio con la tendencia para determinar niveles de soporte o resistencia. La estrategia utiliza las ventajas de ambos indicadores, buscando oportunidades de compra o venta cuando se produce un cruce dorado entre las Bandas de Bollinger y las líneas de Keltner, y verifica las señales con el volumen de negociación. Esto permite identificar eficazmente el inicio de una tendencia y minimizar las señales falsas.

Principio de la estrategia

- Se calculan la banda media, superior e inferior de Bollinger con un período de 20, y el ancho de banda se define mediante 2 veces la desviación estándar.

- Se calculan la banda media, superior e inferior de Keltner con un período de 20, y el ancho de banda se define mediante 2,2 veces el rango verdadero promedio.

- Cuando la banda superior de Keltner cruza por encima de la banda superior de Bollinger y el volumen es mayor que el promedio de 10 períodos, se abre una posición larga.

- Cuando la banda inferior de Keltner cruza por debajo de la banda inferior de Bollinger y el volumen es mayor que el promedio de 10 períodos, se abre una posición corta.

- Si la posición no se cierra después de 20 velas desde la apertura, se fuerza el cierre con take profit o stop loss.

- Se establece un stop loss del 1,5% para posiciones largas y del -1,5% para posiciones cortas; además, se utiliza un trailing stop del 2% para largas y del -2% para cortas.

Esta estrategia se basa principalmente en las Bandas de Bollinger para determinar el rango y la fuerza de la volatilidad, y utiliza el indicador Keltner como verificación complementaria. La combinación de dos indicadores con parámetros diferentes pero de naturaleza similar mejora la precisión de las señales, y la inclusión del volumen reduce eficazmente las señales falsas.

Análisis de ventajas

- La combinación de las ventajas de las Bandas de Bollinger y el indicador Keltner mejora la precisión de las señales de trading.

- La incorporación del volumen reduce eficazmente las señales falsas generadas por movimientos laterales frecuentes del mercado.

- Los mecanismos de stop loss y trailing stop permiten un control efectivo del riesgo.

- El cierre forzado tras señales falsas permite detener pérdidas o asegurar ganancias rápidamente.

Análisis de riesgos

- Tanto las Bandas de Bollinger como el indicador Keltner se basan en medias móviles y cálculos de volatilidad, por lo que pueden generar señales erróneas en mercados laterales.

- No hay un mecanismo de capitalización compuesta, por lo que ser atrapado repetidamente puede generar pérdidas excesivas.

- Las señales de reversión son comunes, y ajustar los parámetros puede hacer que se pierdan oportunidades de tendencia.

Se puede ampliar el margen de stop loss o agregar indicadores auxiliares como MACD para filtrar señales y reducir el riesgo de señales falsas.

Direcciones de optimización

- Se pueden probar diferentes parámetros para evaluar su impacto en la rentabilidad, como ajustar la longitud de la media móvil o el múltiplo de la desviación estándar.

- Se pueden agregar otros indicadores para confirmar las señales, como el indicador KDJ o MACD como apoyo.

- Se pueden utilizar métodos de aprendizaje automático para optimizar automáticamente los parámetros.

Resumen

Esta estrategia utiliza de manera integral las Bandas de Bollinger y el indicador Keltner para identificar tendencias del mercado, complementadas con el volumen para verificar las señales. Mediante la optimización de parámetros y la incorporación de otros indicadores técnicos, se puede fortalecer aún más la estrategia para adaptarla a una gama más amplia de condiciones del mercado. En general, la estrategia es bastante factible y es una de las estrategias de trading cuantitativo fáciles de entender y ajustar.

- 1