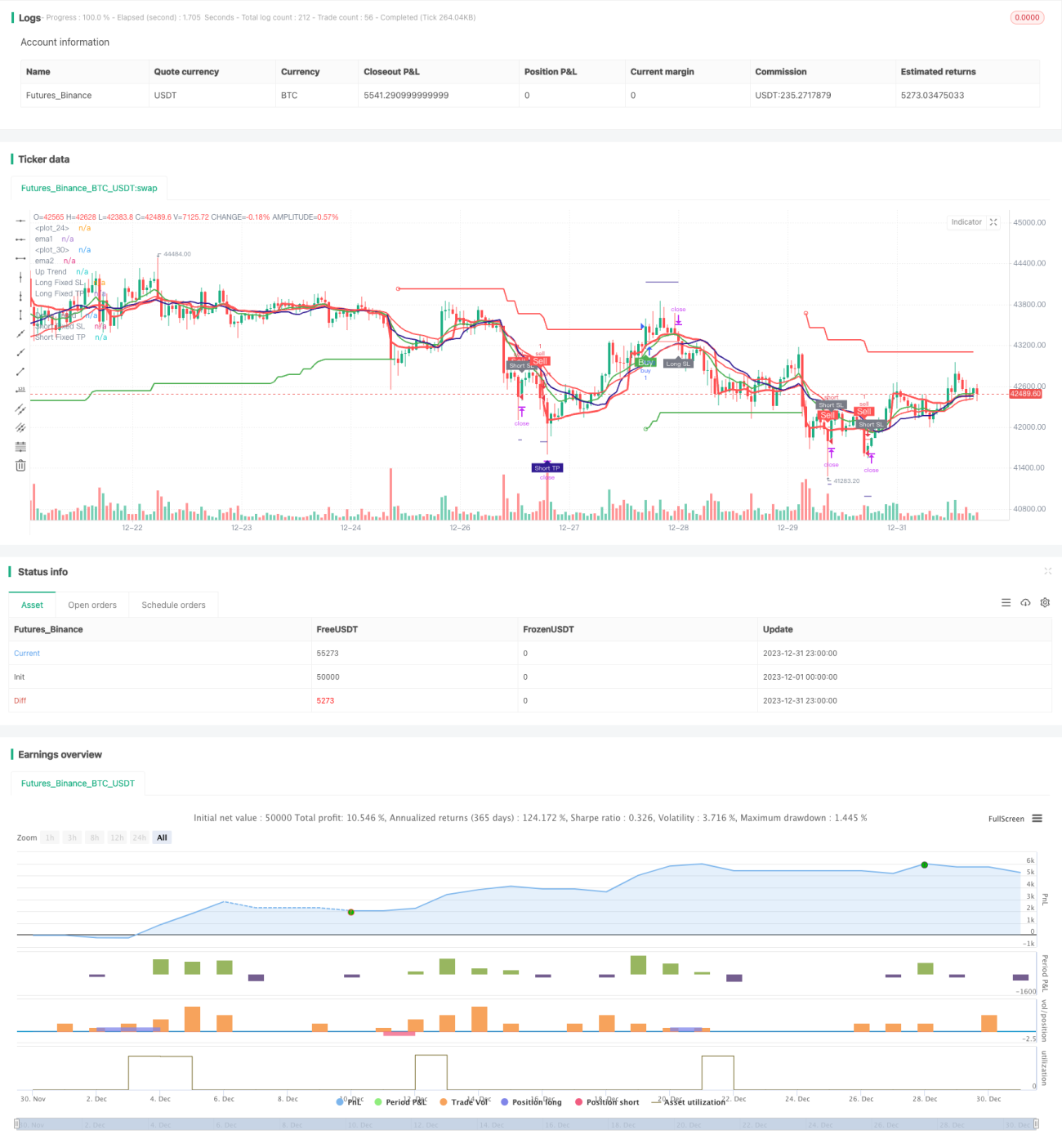

Una estrategia de trading cuantitativo que utiliza múltiples indicadores técnicos

Resumen

Esta estrategia es una estrategia de trading cuantitativo que utiliza múltiples indicadores técnicos. Principalmente emplea el cruce de medias móviles EMA, el indicador SuperTrend, el RSI, el MACD y otros indicadores en combinación para generar señales de trading.

Principio de la estrategia

La lógica central de trading de esta estrategia se basa en los siguientes aspectos:

-

Cruce de medias móviles EMA: Se calculan la EMA rápida (EMA1) y la EMA lenta (EMA2). Cuando la rápida cruza por encima de la lenta, se genera una señal de compra; cuando la rápida cruza por debajo de la lenta, se genera una señal de venta.

-

Media móvil VWMA: Se calcula la media móvil VWMA. Cuando el precio de cierre cruza por encima de esta media, se considera una señal de compra; cuando la cruza por debajo, se considera una señal de venta.

-

Indicador SuperTrend: Se calculan las bandas superior e inferior del SuperTrend basadas en el ATR y el parámetro multiplier, determinando la dirección de la tendencia. En una tendencia alcista se genera una señal de compra; en una tendencia bajista, una señal de venta.

-

Indicador RSI: Se calcula el RSI. Cuando el RSI supera la línea de sobrecompra, se considera una señal de venta; cuando cae por debajo de la zona de sobreventa, se considera una señal de compra.

-

Indicador MACD: Se calculan la línea rápida, la línea lenta y la línea de señal del MACD. Cuando la línea rápida cruza por encima de la línea de señal, se genera una señal de compra; cuando la cruza por debajo, una señal de venta.

Una vez obtenidas las señales de trading de los múltiples indicadores anteriores, la estrategia utiliza la lógica "Y" (AND) para decidir: solo cuando varios indicadores emiten la señal simultáneamente se generan las señales finales de compra y venta.

Ventajas de la estrategia

Esta estrategia combina múltiples indicadores para evaluar el mercado, reduciendo eficazmente las señales falsas. Las principales ventajas incluyen:

-

Filtrado compuesto mediante múltiples indicadores, reduciendo señales erróneas de un solo indicador.

-

Combinación de indicadores de tendencia y osciladores, permitiendo obtener ganancias adicionales en mercados con tendencia.

-

Lógica de stop-loss completa, que controla eficazmente la pérdida máxima por operación.

-

Lógica de aumento de posición (martingala) que permite recuperar pérdidas tras una operación negativa mediante una mayor inversión.

Riesgos de la estrategia

Esta estrategia presenta principalmente los siguientes riesgos:

-

La combinación de múltiples indicadores puede ser demasiado conservadora, perdiendo algunas oportunidades de trading. Se puede simplificar la combinación de indicadores.

-

La lógica de aumento de posición (martingala) puede ampliar las pérdidas. Se deben establecer límites razonables al número de aumentos.

-

Un nivel de stop-loss mal ajustado puede provocar pérdidas innecesarias. Se debe implementar un stop-loss adaptativo.

-

Una configuración inadecuada de los parámetros de los indicadores puede generar demasiadas señales erróneas. Se deben optimizar los parámetros para obtener la mejor combinación.

Direcciones de optimización de la estrategia

Esta estrategia puede optimizarse aún más en los siguientes aspectos:

-

Evaluar el efecto de diferentes combinaciones de parámetros de los indicadores y seleccionar ponderaciones adecuadas.

-

Probar diferentes configuraciones de parámetros de los indicadores.

-

Añadir lógica de stop-loss adaptativo.

-

Incorporar un mecanismo dinámico de gestión de posiciones.

-

Utilizar métodos de aprendizaje automático para optimizar parámetros y modelos.

Conclusión

En general, esta estrategia es una estrategia de trading cuantitativo muy práctica. Integra las ventajas de múltiples indicadores técnicos clásicos, permitiendo una evaluación eficaz del mercado. Mediante la optimización de parámetros y la iteración del modelo, esta estrategia puede obtener mejores resultados de trading.

- 1