Estrategia de la teoría Chan de doble media móvil

Resumen

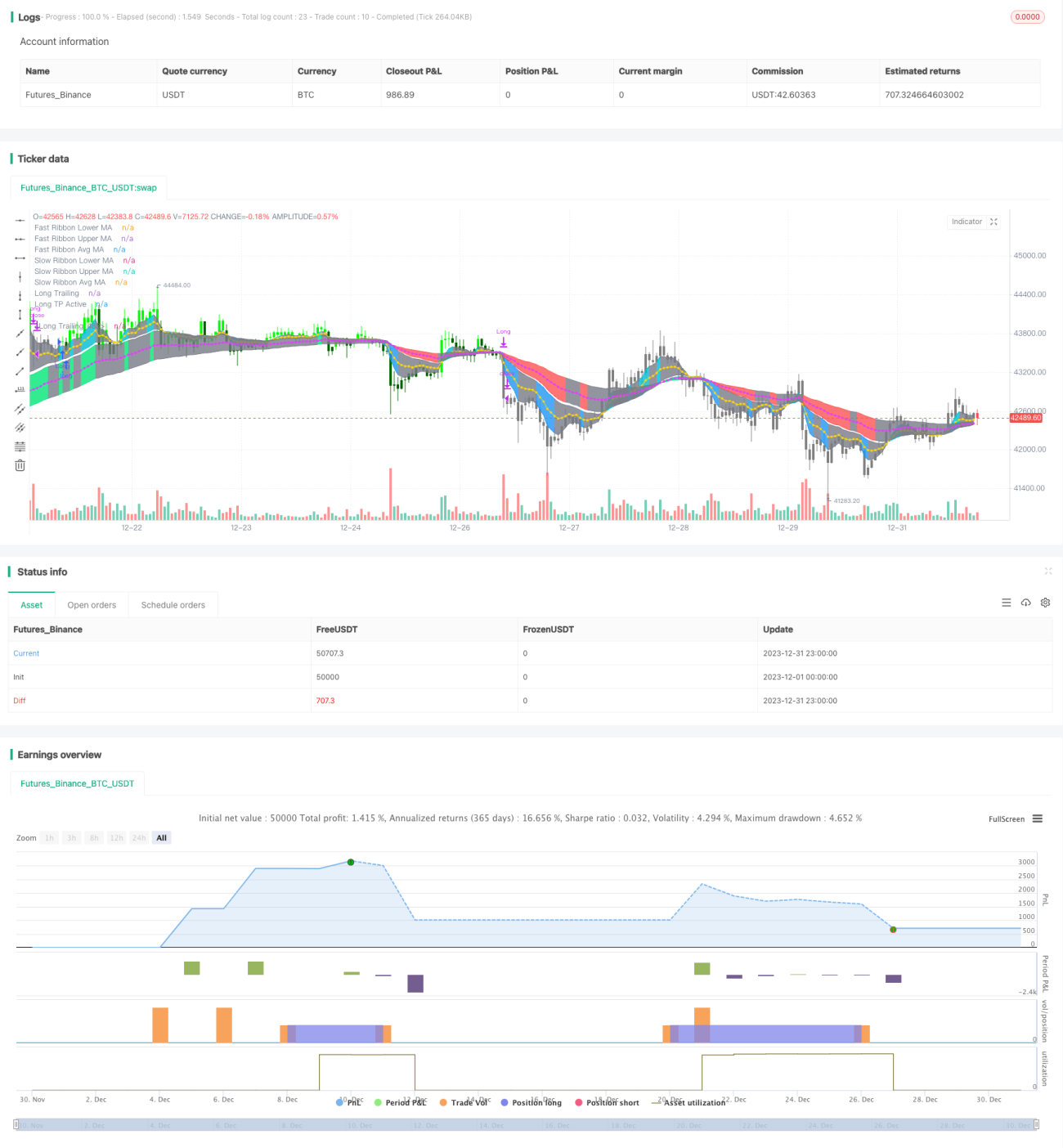

La estrategia de teoría de la envolvente de doble media móvil es una estrategia de seguimiento de tendencia. Calcula dos grupos de medias móviles para construir un grupo rápido y un grupo lento, y combina la relación entre el precio y las medias móviles para determinar la dirección de la tendencia.

Cuando la media rápida cruza por encima de la media lenta, es una señal alcista. Cuando la media rápida cruza por debajo de la media lenta, es una señal bajista. Esta estrategia combina la dirección de las medias rápidas y lentas, así como condiciones como el número de velas de ruptura del precio, para determinar los momentos específicos de entrada y salida.

Principio de la Estrategia

La estrategia de la teoría de la envolvente de doble media móvil calcula dos grupos de medias móviles que representan los criterios de juicio de corto y largo plazo, respectivamente. Específicamente, la estrategia define:

- Grupo de media rápida, que incluye la banda inferior rápida y la banda superior rápida, representando la tendencia de corto plazo.

- Grupo de media lenta, que incluye la banda inferior lenta y la banda superior lenta, representando la tendencia de largo plazo.

La estrategia utiliza la relación de precios entre el grupo rápido y el grupo lento para determinar la validez de las tendencias de corto y largo plazo, así como los momentos específicos de entrada y salida.

Condiciones de entrada:

- Cuando la banda superior rápida cruza al alza la banda superior lenta durante 2 velas o más, es una entrada larga.

- Cuando la banda inferior rápida cruza a la baja la banda inferior lenta durante 2 velas o más, es una entrada corta.

Condiciones de salida:

- Durante la posición larga, cuando la media rápida cruza por debajo de la media lenta, es una salida larga.

- Durante la posición corta, cuando la media rápida cruza por encima de la media lenta, es una salida corta.

Además, la estrategia incorpora funciones de take profit, stop loss y trailing stop para controlar el riesgo.

Análisis de Ventajas

Las principales ventajas de la estrategia de la teoría de la envolvente de doble media móvil son:

- Al juzgar mediante la doble media móvil, puede filtrar eficazmente el ruido del mercado y fijar la dirección de la tendencia.

- Combinando la relación entre las medias rápidas/lentas y el precio, la fiabilidad de las señales es relativamente alta.

- Las reglas de la estrategia son simples y claras, fáciles de entender e implementar, adecuadas para el trading cuantitativo.

- Incorpora medidas de control de riesgo como take profit, stop loss y trailing stop, que pueden controlar efectivamente el riesgo de las operaciones.

Análisis de Riesgos

La estrategia de la teoría de la envolvente de doble media móvil también presenta ciertos riesgos, principalmente reflejados en:

- En mercados laterales, puede generar señales falsas, provocando operaciones innecesarias.

- El sistema de medias móviles reacciona lentamente ante eventos repentinos (como noticias importantes positivas/negativas), lo que puede provocar grandes pérdidas.

- El trailing stop puede ser superado en condiciones específicas del mercado, ampliando las pérdidas.

Para controlar los riesgos anteriores, se puede mejorar optimizando los parámetros de las medias móviles o combinando otros indicadores de filtrado.

Direcciones de Optimización

La estrategia de la teoría de la envolvente de doble media móvil puede optimizarse desde las siguientes dimensiones:

- Optimizar los parámetros de las medias móviles, ajustando los períodos para adaptarse a diferentes ciclos del mercado.

- Añadir filtros de otros indicadores para formar una estrategia combinada de múltiples indicadores, mejorando la precisión de las señales.

- Optimizar la configuración de stop loss y take profit, estableciendo umbrales de retroceso para controlar la pérdida máxima.

- Introducir modelos de aprendizaje automático para predecir la tendencia, ayudando a determinar el momento de entrada.

Resumen

En general, la estrategia de la teoría de la envolvente de doble media móvil es una estrategia de seguimiento de tendencia muy práctica. Sus reglas de juicio son simples, la lógica es clara, controla el riesgo mediante el sistema de doble media móvil, y tiene una sólida base teórica. Los próximos pasos pueden incluir mejoras en la optimización de parámetros, control de riesgos y otros aspectos para mejorar aún más la rentabilidad y estabilidad de la estrategia.

- 1