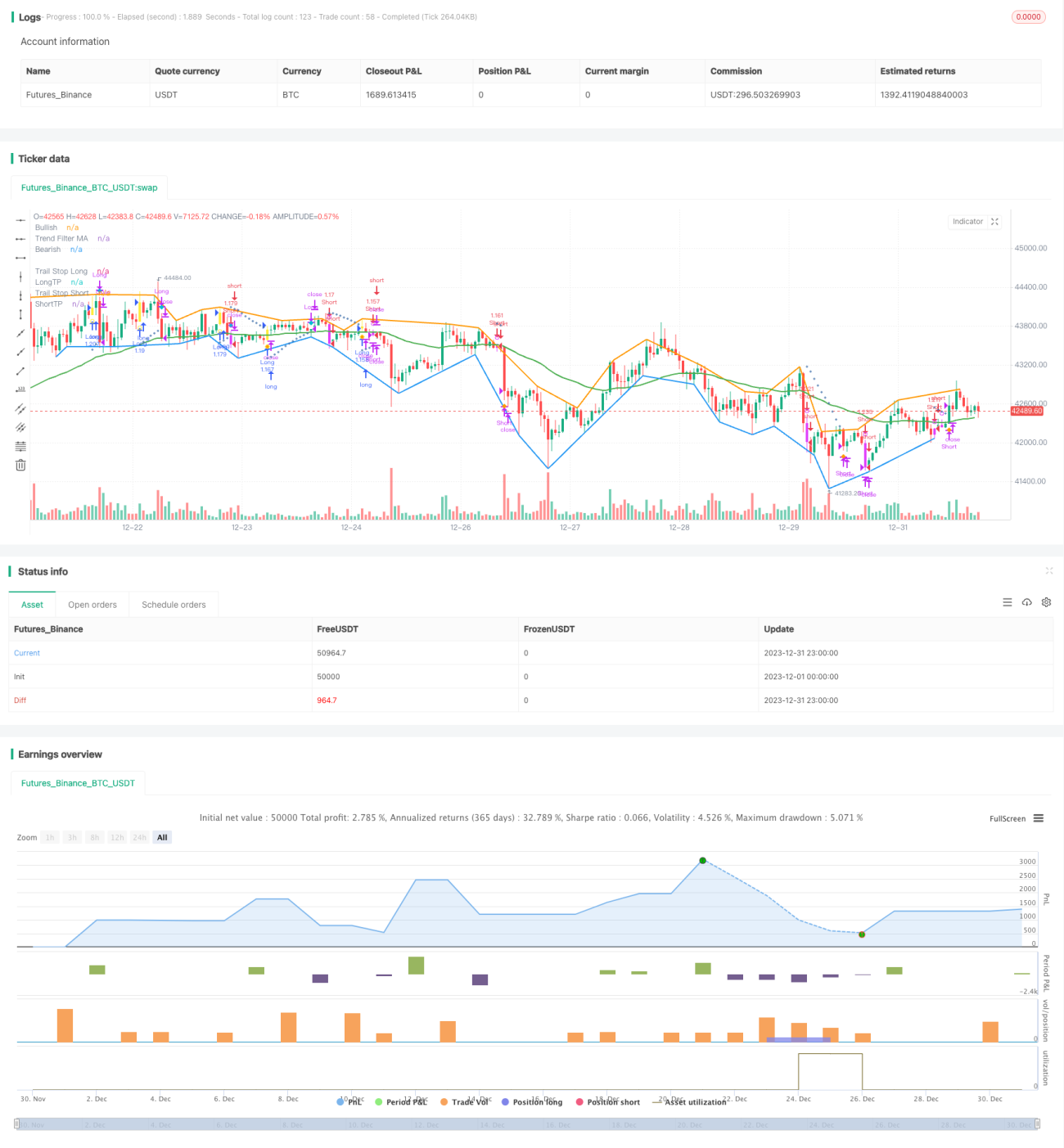

Estrategia de trading con MACD multiperíodo

Resumen

Esta estrategia se basa en el clásico indicador MACD, combinado con indicadores de juicio de tendencia, métodos de stop loss y take profit, formando un sistema de trading de seguimiento de tendencia relativamente completo. Puede usarse tanto para criptomonedas como para trading de divisas y acciones.

Principio de la estrategia

-

Juicio del indicador MACD

- La diferencia entre la EMA de periodo FASTLENGTH y la EMA de periodo SLOWLENGTH forma las barras MACD.

- La EMA de periodo MACDLENGTH suaviza las barras MACD para formar la línea MACD.

- La ruptura del eje 0 por parte de las barras MACD genera señales de compra y venta.

-

Juicio de tendencia

- ADX: Indicador de movimiento direccional promedio, determina si existe una tendencia.

- MA: Media móvil, el precio por encima o por debajo de la MA forma la tendencia.

- SAR: Parabólico SAR, el SAR se mueve por encima o por debajo del precio para determinar la tendencia.

-

Métodos de stop loss

- Stop loss porcentual basado en ATR: Se establece un stop loss porcentual según el factor ATR.

- Stop loss con SAR: El SAR actúa como stop loss tras la entrada.

-

Métodos de take profit

- Distancia fija de take profit basada en ATR: Se establece una distancia fija de take profit según el factor ATR.

- Take profit porcentual: Se establece una distancia porcentual de take profit.

-

Stop loss por tiempo

- Se puede configurar un stop loss después de un número específico de barras.

Análisis de ventajas

-

Múltiples juicios auxiliares

- La combinación de tendencia y soporte/resistencia reduce señales falsas.

- Stop loss con ATR/SAR ofrece un control de riesgos más completo.

-

Configuración flexible

- Se puede elegir si usar filtro de tendencia o no.

- Se puede elegir stop loss con ATR o SAR.

- Se puede elegir take profit con ATR o estándar.

- Parámetros configurables de forma flexible.

-

Proporciona análisis de divergencias

- Muestra divergencias positivas y negativas históricas.

- Proporciona indicaciones textuales.

-

Fácil optimización y ajuste

- La estrategia incluye numerosos parámetros configurables.

- Permite probar fácilmente diferentes combinaciones de variables.

Análisis de riesgos

-

Parámetros inadecuados pueden aumentar las pérdidas

- Una configuración incorrecta de ATR o SAR puede provocar un stop loss prematuro.

- Un ratio de take profit demasiado alto puede cerrar la operación antes de tiempo.

-

Riesgo de fallo en el juicio de tendencia

- Parámetros inadecuados en los indicadores de tendencia pueden llevar a juicios erróneos.

- Eventos imprevistos pueden invalidar el juicio de tendencia.

-

Riesgo del stop loss por tiempo

- Un stop loss por tiempo fijo conlleva riesgo de pérdida.

Direcciones de optimización

- Ajustar los parámetros de ATR y SAR para un stop loss más suave.

- Probar diferentes periodos de MA para optimizar el juicio de tendencia.

- Probar ajustes en el ratio de take profit para optimizar la rentabilidad.

- Combinar indicadores de volatilidad para optimizar parámetros.

Resumen

Esta estrategia considera múltiples aspectos como el juicio de tendencia, stop loss/take profit, identificación de divergencias, etc., formando un sistema de trading de criptomonedas relativamente completo. Combina las ventajas del indicador MACD, añade un filtro de tendencia para evitar operaciones erróneas, incorpora stop loss con ATR/SAR para un mejor control del riesgo, y la identificación de divergencias proporciona una referencia adicional. Los múltiples parámetros configurables facilitan las pruebas y optimizaciones. En general, esta estrategia sirve como un buen ejemplo para la investigación de estrategias de trading de criptomonedas.

- 1