Estrategia de ruptura de momentum con doble media móvil

Resumen

La estrategia de ruptura de impulso con doble media móvil (DMA) es una estrategia de trading cuantitativo que combina dos medias móviles y el indicador RSI. Esta estrategia calcula una media móvil rápida, una media móvil lenta y el RSI, estableciendo umbrales de sobrecompra y sobreventa para el indicador de impulso RSI. Cuando se produce un cruce dorado de las dos medias móviles, se abre una posición larga; cuando se produce un cruce de la muerte, se abre una posición corta, con el objetivo de capturar movimientos tendenciales del mercado.

Principio de la estrategia

La estrategia de ruptura de impulso con doble media móvil se basa principalmente en dos medias móviles y el RSI. Primero se calculan dos medias móviles, una rápida y otra lenta: la rápida es una media móvil ponderada de 10 períodos, y la lenta es una media móvil adaptativa lineal de 100 períodos. Luego se calcula el RSI de 14 períodos y se establecen los umbrales de sobrecompra y sobreventa. Cuando la media rápida cruza por encima de la lenta, se considera un mercado alcista; cuando la rápida cruza por debajo de la lenta, es un mercado bajista. Al determinar la dirección del mercado, también se requiere que el RSI supere el nivel de sobrecompra o esté por debajo del nivel de sobreventa, filtrando así eficazmente las falsas rupturas.

En concreto, cuando se identifica un mercado alcista y el RSI en ese momento supera el nivel de sobrecompra, se abre una posición larga; cuando se identifica un mercado bajista y el RSI está por debajo del nivel de sobreventa, se abre una posición corta. Una vez abierta la posición, se realiza una operación inversa cuando la señal de trading se revierte.

Ventajas de la estrategia

La estrategia de ruptura de impulso con doble media móvil combina dos medias móviles y el RSI, lo que permite identificar eficazmente las tendencias del mercado y utilizar el RSI para filtrar falsas rupturas, mejorando así la fiabilidad de las señales de trading. En comparación con un sistema de una sola media móvil, esta estrategia reduce significativamente la cantidad de operaciones no rentables. Además, la optimización de los parámetros del RSI aporta flexibilidad a la estrategia.

Riesgos de la estrategia

La estrategia de ruptura de impulso con doble media móvil también presenta ciertos riesgos. El sistema de dos medias móviles es muy sensible a los parámetros, por lo que es necesario probar cuidadosamente combinaciones de parámetros en diferentes mercados. Además, si los umbrales del RSI no se configuran adecuadamente, se pueden perder oportunidades de trading. Por último, un stop loss móvil agresivo puede ser superado en determinadas condiciones del mercado; por lo tanto, se debe ajustar el nivel de stop loss en función de los resultados del backtesting.

Optimización de la estrategia

La estrategia de ruptura de impulso con doble media móvil se puede optimizar en los siguientes aspectos:

- Optimizar los parámetros de las medias móviles rápida y lenta para encontrar la combinación óptima.

- Optimizar los parámetros del RSI ajustando los umbrales de sobrecompra y sobreventa.

- Incorporar un mecanismo de stop loss móvil adaptativo para controlar el riesgo.

- Añadir un módulo de optimización del tamaño de la posición para mejorar la eficiencia en el uso del capital.

Conclusión

La estrategia de ruptura de impulso con doble media móvil determina la dirección de la tendencia mediante un sistema de dos medias móviles y utiliza el RSI para filtrar señales, mejorando eficazmente las limitaciones de un sistema de una sola media móvil. Esta estrategia ofrece un amplio margen de optimización de parámetros y puede adaptarse dinámicamente, lo que la convierte en una excelente estrategia de seguimiento de tendencias.

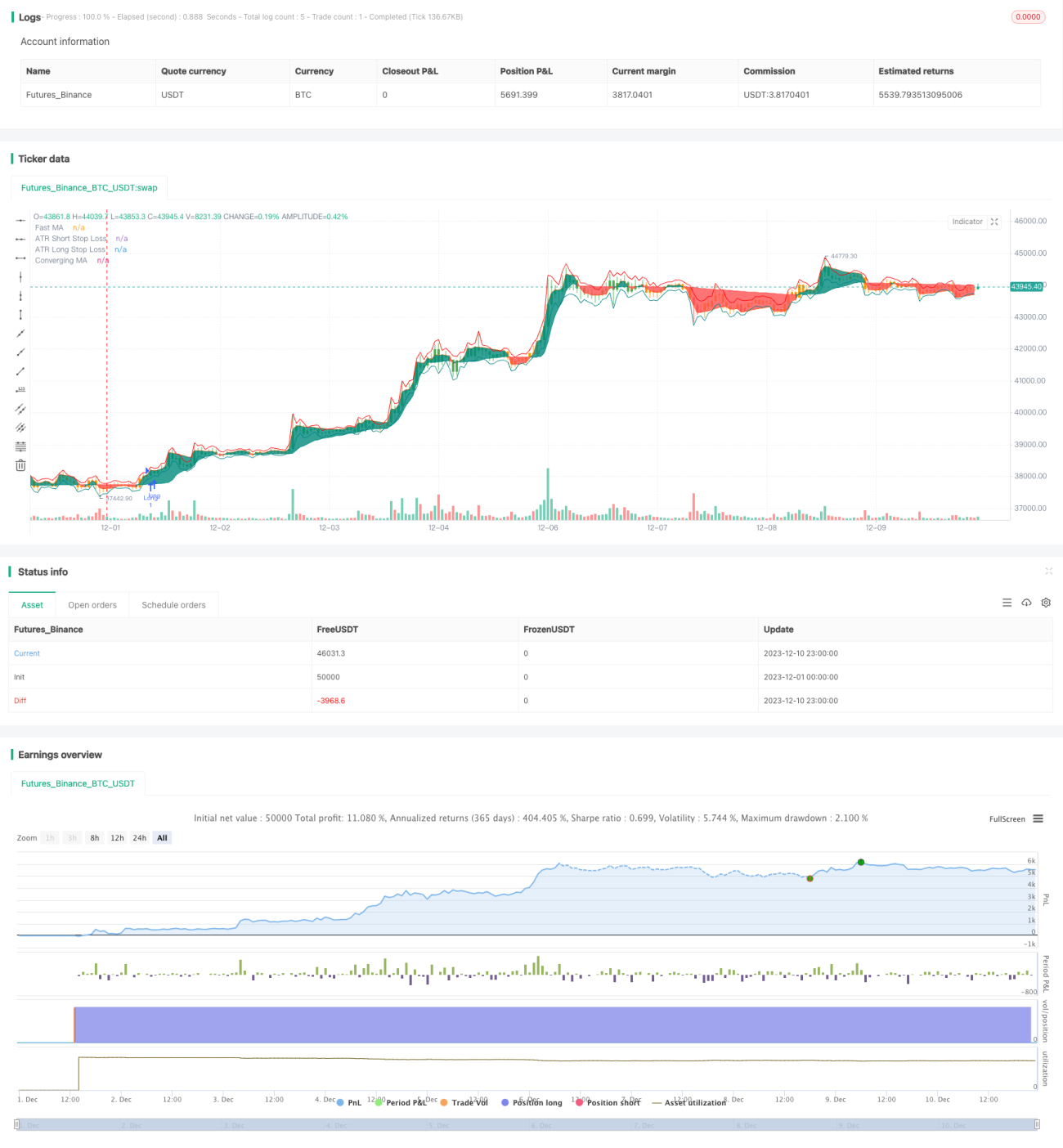

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-10 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) https://creativecommons.org/licenses/by-nc-sa/4.0/

// © Salman4sgd

//@version=5- 1