Estrategia de trading a corto plazo con ruptura de momentum

Resumen

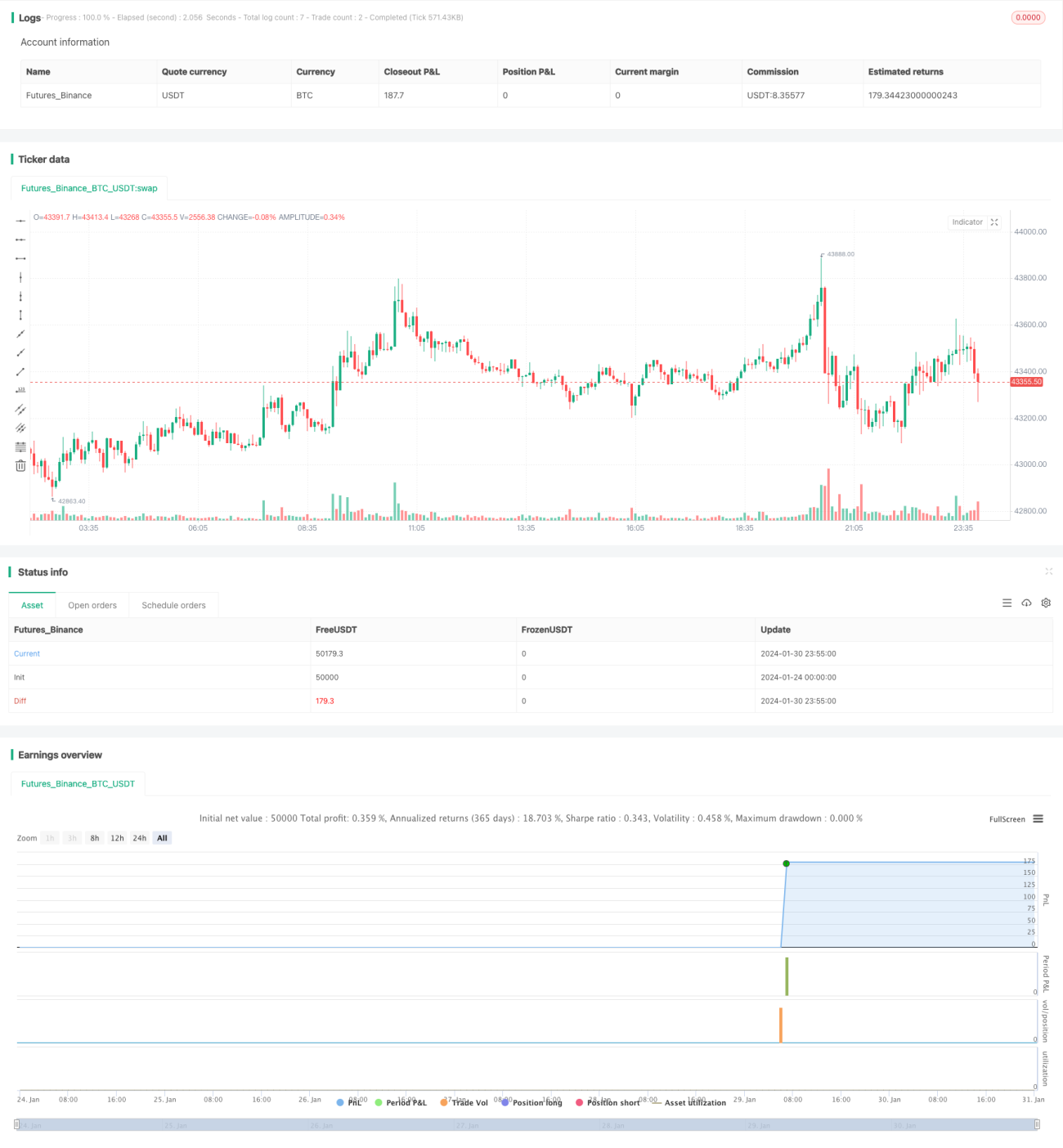

Esta estrategia sigue los datos de trading de SPY y combina señales de múltiples indicadores técnicos como medias móviles, MACD y RSI para juzgar con precisión la tendencia a corto plazo y tomar decisiones de compra/venta, con el objetivo de obtener beneficios en operaciones a corto plazo.

Principio de la estrategia

La lógica central de esta estrategia se basa en los siguientes indicadores técnicos para determinar la tendencia a corto plazo y los momentos de entrada:

- Los cruces dorados y de muerte de las medias móviles exponenciales (EMA) de 5 y 13 días se utilizan para determinar los cambios en la tendencia alcista o bajista.

- El indicador MACD evalúa si existe un impulso alcista.

- El indicador ADX determina si hay una tendencia establecida.

- El indicador RSI mide la fuerza de la tendencia.

Optimizando los parámetros de estos indicadores, se identifican los puntos clave de cambio de tendencia. Cuando se cumplen 5 de 6 condiciones, se muestra una señal blanca con las indicaciones L o S. Cuando se cumplen las seis condiciones por completo, se muestra una señal en forma de triángulo dorado (△) al cierre de esa vela.

Condiciones para la señal de compra:

EMA de 5 días > EMA de 13 días, y línea MACD < 0.5, y ADX > 20, y pendiente del MACD > 0, y línea de señal > -0.1, y RSI > 40.

Condiciones para la señal de venta:

EMA de 5 días < EMA de 13 días, y línea MACD > -0.5, y ADX > 20, y línea de señal < 0, y pendiente del MACD < 0, y RSI < 60.

Análisis de ventajas

Esta estrategia presenta las siguientes ventajas:

- Al combinar múltiples señales de indicadores, ofrece una alta precisión en el juicio.

- Mediante la optimización de parámetros, se logra un equilibrio entre sensibilidad y precisión.

- Las señales son claras y simples, con una baja barrera de entrada para operar.

- Adecuada para operaciones a corto plazo, alineada con el perfil de riesgo de la mayoría de los inversores.

- Considera las necesidades de la operativa en tiempo real, evitando la alta volatilidad al final de la sesión.

Análisis de riesgos

Esta estrategia también conlleva los siguientes riesgos:

- Una configuración inadecuada de parámetros puede provocar juicios erróneos. Se requiere prueba y optimización continuas.

- Al operar un solo activo, no se puede diversificar el riesgo entre sectores y clases de activos.

- Riesgo de comisiones y deslizamiento debido a la alta frecuencia de operaciones.

- No poder abrir posiciones al final de la sesión puede hacer que se pierdan algunas oportunidades.

Direcciones de optimización

Se puede continuar optimizando esta estrategia desde las siguientes dimensiones:

- Probar modificaciones en la configuración de parámetros para mejorar la precisión de los juicios.

- Añadir indicadores de stop-loss para controlar las pérdidas por operación.

- Optimizar el horario de apertura de posiciones, filtrando los periodos de alta volatilidad al final de la sesión.

- Incluir otros activos como objetivo de la estrategia.

- Incorporar algoritmos de aprendizaje automático para mejorar la capacidad de adaptación de los parámetros.

Conclusión

Esta estrategia sigue los datos de SPY y combina indicadores técnicos como medias móviles, MACD y RSI para determinar las tendencias a corto plazo. Ofrece una alta frecuencia de operaciones y un bajo drawdown, lo que la hace muy adecuada para el trading a corto plazo. Se puede seguir optimizando desde múltiples dimensiones, con un amplio margen de mejora.

/*backtest

start: 2024-01-24 00:00:00

end: 2024-01-31 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="SPY 1 Minute Day Trader", overlay=true)

//This script has been created to take into account how the following variables impact trend for SPY 1 Minute- 1