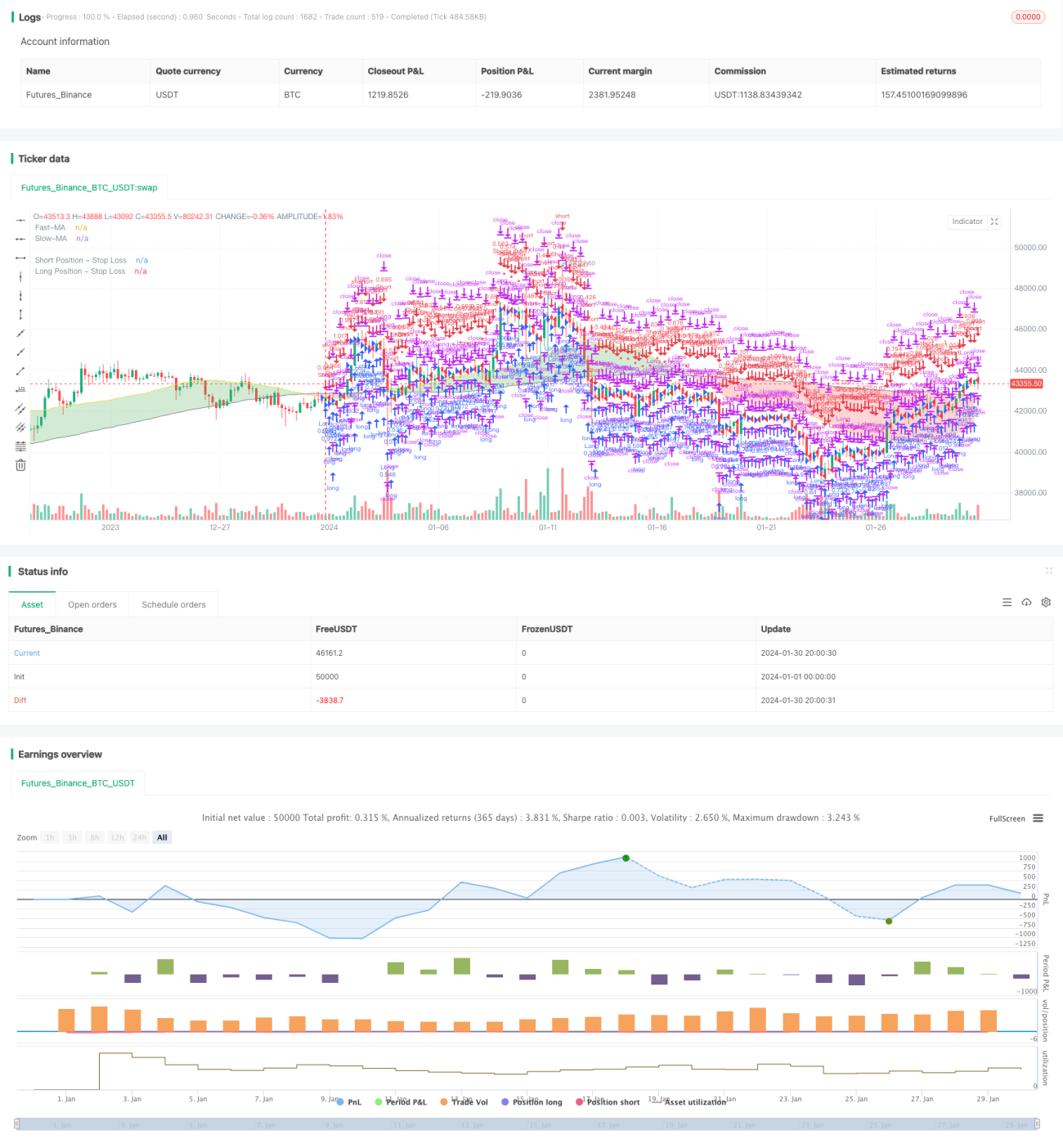

Estrategia de trading cuantitativa de doble media móvil

Resumen

Esta estrategia calcula medias móviles rápidas y lentas, combinadas con el indicador parabólico para tomar decisiones de compra y venta. Pertenece al tipo de estrategias de seguimiento de tendencia. Cuando la media móvil rápida cruza por encima de la lenta, se abre una posición larga; cuando la rápida cruza por debajo de la lenta, se abre una posición corta. Además, se utiliza el indicador parabólico para filtrar falsas rupturas.

Principio de la estrategia

- Calcular la media móvil rápida y la media móvil lenta. Los parámetros de las medias móviles se pueden personalizar.

- Comparar las dos medias móviles para determinar la dirección de la tendencia del mercado. Cuando la media móvil rápida cruza por encima de la lenta, se considera un mercado alcista; cuando la rápida cruza por debajo de la lenta, se considera un mercado bajista.

- Usar la relación entre el precio de cierre y las medias móviles como confirmación adicional. Solo cuando la rápida cruza por encima de la lenta y el precio de cierre está por encima de la rápida, se genera una señal de compra. Solo cuando la rápida cruza por debajo de la lenta y el precio de cierre está por debajo de la rápida, se genera una señal de venta.

- Usar el indicador parabólico para filtrar falsas rupturas. Solo cuando la rápida cruza por encima de la lenta, el precio de cierre está por encima de la rápida y el precio de la acción está por encima del parabólico, se genera finalmente la señal de compra; y viceversa.

- Establecer un stop loss basado en la pérdida máxima asumible. Calcular el precio de stop loss específico combinando el indicador ATR.

Ventajas de la estrategia

- Utiliza medias móviles para determinar la dirección de la tendencia del mercado, evitando operar con frecuencia en mercados laterales sin dirección clara.

- El doble filtro puede evitar eficazmente el problema común de las falsas rupturas.

- Combinada con una estrategia de stop loss, controla eficazmente la pérdida por operación.

Riesgos de la estrategia

- Las estrategias basadas en indicadores son propensas a generar señales falsas.

- No se considera el riesgo cambiario.

- Puede perder movimientos iniciales en direcciones opuestas.

Ante los problemas anteriores, se puede optimizar desde los siguientes aspectos:

- Optimizar los parámetros de las medias móviles para que se ajusten mejor al activo específico.

- Se puede combinar con otros indicadores o modelos para filtrar señales.

- Considerar la cobertura en tiempo real o la conversión automática de cuentas de corretaje para el riesgo cambiario.

Direcciones de optimización

- Optimizar los parámetros de las medias móviles para capturar mejor las tendencias.

- Añadir combinaciones de modelos para mejorar la precisión de las señales.

- Validar en múltiples marcos temporales para evitar quedar atrapado.

- Optimizar la estrategia de stop loss para mejorar la estabilidad de la estrategia.

Conclusión

Esta estrategia es una típica estrategia de seguimiento de tendencia basada en la combinación de dos medias móviles e indicadores. Determinando la tendencia del mercado mediante la comparación de direcciones de las medias móviles rápidas y lentas, y combinando múltiples filtros para evitar señales falsas, se generan señales de trading. Además, la estrategia cuenta con función de stop loss para controlar la pérdida por operación. La ventaja es que la lógica de la estrategia es simple y clara, fácil de entender e implementar, y se puede optimizar flexiblemente según sea necesario. La desventaja es que, como herramienta aproximada de juicio de tendencia, la precisión de las señales debe mejorarse, y se puede optimizar introduciendo modelos avanzados como el aprendizaje automático.

- 1