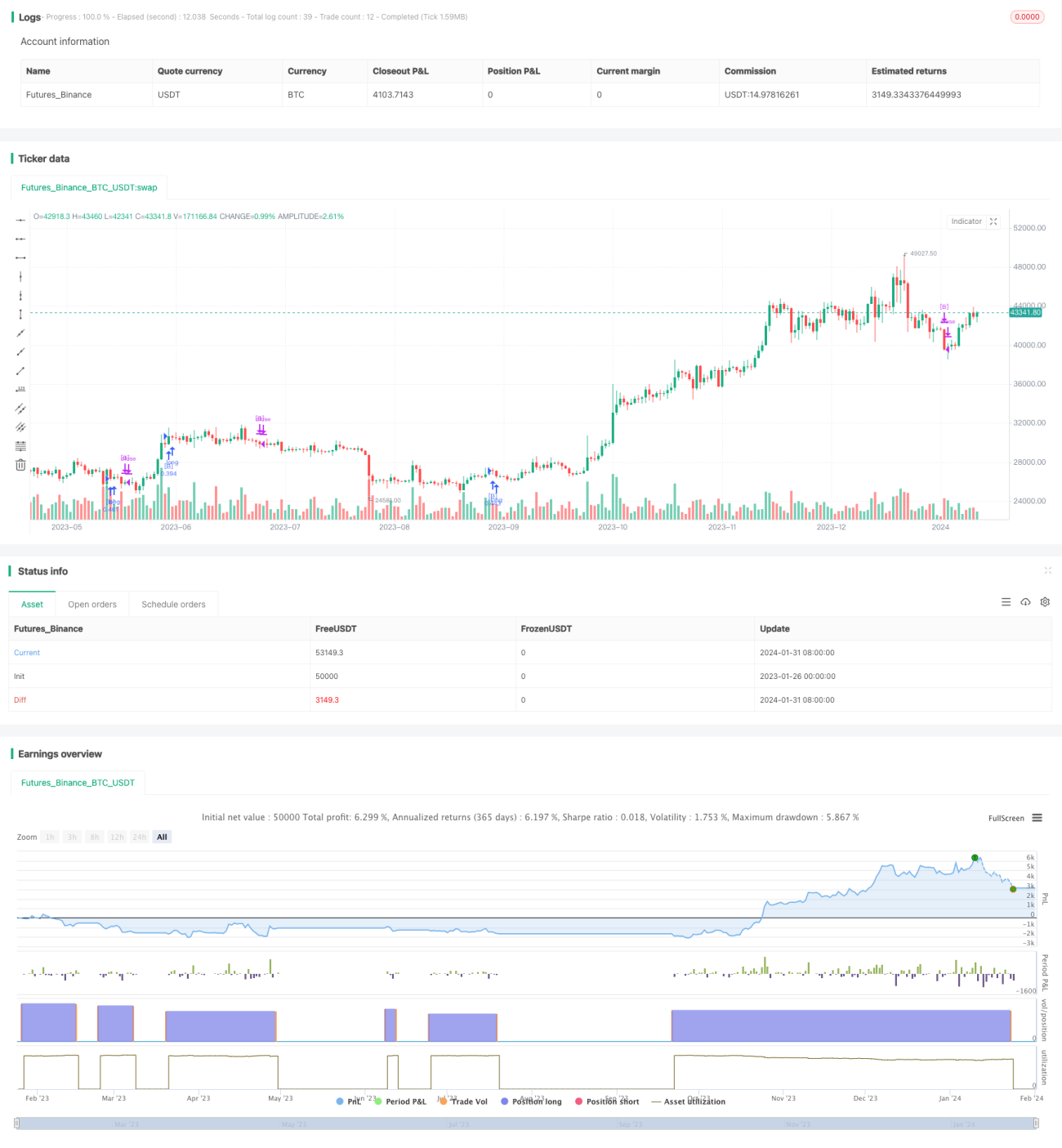

Estrategia de reversión a largo plazo basada en doble media móvil

Resumen

Esta estrategia utiliza principalmente el cruce dorado y el cruce de la muerte formados por las medias móviles simples de 14 y 28 días para realizar operaciones de reversión. Cuando la media rápida supera al alza la media lenta desde abajo, indica que la tendencia del mercado comienza a revertirse, y se puede abrir una posición larga. Cuando la media rápida cruza a la baja la media lenta desde arriba, indica que la tendencia del mercado comienza a revertirse, y se puede abrir una posición corta.

Debido a que utiliza medias móviles simples para juzgar los cambios en la tendencia del mercado, he denominado a esta estrategia "Estrategia de reversión de largo plazo basada en doble media móvil".

Principio de la estrategia

La lógica central de esta estrategia consiste en utilizar dos medias móviles simples de diferente período (14 y 28 días) para juzgar la tendencia del mercado. Las reglas específicas son las siguientes:

-

Se define la línea rápida como la media móvil simple de 14 días, y la línea lenta como la media móvil simple de 28 días.

-

Cuando la línea rápida supera al alza la línea lenta desde abajo, es una señal alcista, y se abre una posición larga.

-

Cuando la línea rápida cruza a la baja la línea lenta desde arriba, es una señal bajista, y se abre una posición corta.

-

Después de abrir una posición larga/corta, cuando la línea rápida vuelve a cruzar por debajo de la línea lenta, es una señal de cierre de la posición.

Esta estrategia también incorpora stop loss, take profit y trailing stop para la gestión de riesgos. Para las posiciones largas y cortas, se definen respectivamente el precio de stop loss de la posición larga, el precio de take profit de la posición larga, el precio de take profit de la posición corta y el precio de trailing stop de la posición larga. Estos parámetros se establecen en forma de porcentaje, lo que hace que la estrategia sea más flexible.

Análisis de ventajas

- La estrategia que utiliza dos medias móviles para juzgar la tendencia principal del mercado tiene un principio simple y claro, fácil de entender y verificar.

- Los períodos de las medias rápidas y lentas se establecen en 14 y 28 días, que representan las transiciones de tendencia a corto y mediano plazo, lo que permite detectar bien las oportunidades de reversión.

- La combinación de take profit, stop loss y trailing stop para controlar el riesgo permite asegurar las ganancias y evitar que las pérdidas se amplíen.

- Permite operar tanto en largo como en corto, satisfaciendo las necesidades de diferentes entornos de mercado.

Riesgos y mejoras

- El cruce de dos medias móviles tiene cierto retraso, pudiendo perderse el mejor momento de entrada.

- El cruce de medias de largo y corto plazo puede generar señales falsas; se debe evitar establecer períodos demasiado cortos para las medias.

- Una distancia de stop loss demasiado pequeña puede aumentar la probabilidad de que el stop sea alcanzado. Se debe establecer una distancia de stop loss adecuada según los diferentes instrumentos.

- Se pueden introducir más indicadores para combinarlos y mejorar la robustez de la estrategia. Por ejemplo, añadir Bandas de Bollinger para determinar la tendencia, o incorporar el MACD para verificar el momento de entrada.

Direcciones de optimización

- Probar diferentes combinaciones de parámetros de medias móviles para encontrar el período que mejor se adapte a las características del instrumento.

- Probar diferentes configuraciones de distancia de stop loss para encontrar la ubicación óptima de stop.

- Probar la incorporación de otros indicadores para optimizar y encontrar la combinación de parámetros que reduzca las señales falsas.

- Optimizar las reglas de gestión de posiciones para que las ganancias sean más sustanciales.

Resumen

En general, esta estrategia es una estrategia clásica basada en el cruce de dos medias móviles para determinar la reversión de la tendencia. Tiene la ventaja de un principio de operación simple y fácil de dominar; también presenta algunas direcciones que se pueden seguir optimizando en el futuro. En conjunto, la estrategia es relativamente madura tanto en principio como en operación, y constituye una excelente estrategia de introducción al trading cuantitativo.

- 1