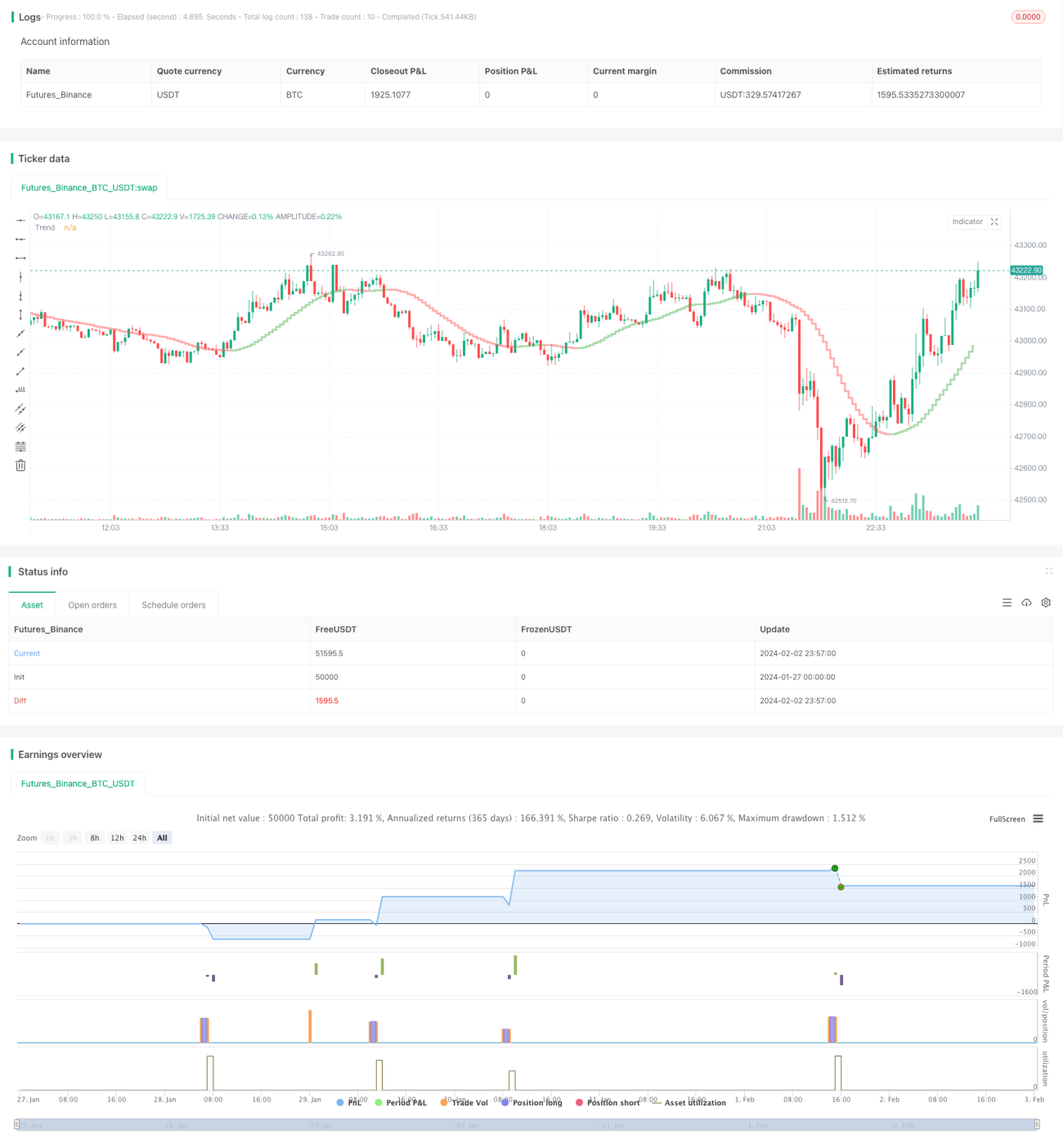

Estrategia de Ripple basada en el indicador Coral Trend en el intervalo de backtesting

Resumen

Esta estrategia utiliza el indicador Coral Trend de LazyBear para determinar la dirección de la tendencia de precios, identificando las reversiones en la dirección de dicho indicador para detectar posibles puntos de entrada. Para filtrar falsas rupturas, la estrategia emplea una combinación del indicador ADX o del histograma de fuerza absoluta (Absolute Strength Histogram) y el indicador de volumen HawkEye como confirmación, logrando entradas más fiables.

El mecanismo de salida establece niveles de stop loss y take profit basados en el precio máximo/mínimo de las últimas N velas, multiplicado por una relación riesgo-recompensa configurable.

Principio de la Estrategia

Tras determinar la dirección de la tendencia principal mediante el indicador Coral Trend, cuando el color del indicador se mantiene sin cambios, se produce un pequeño retroceso (pullback) en dirección opuesta al precio. Si al finalizar ese retroceso el precio retoma la dirección principal señalada por Coral Trend, se considera un buen momento de entrada.

Las condiciones de entrada incluyen:

-

La dirección del indicador Coral Trend coincide con la dirección de la operación (alcista = verde, bajista = rojo).

-

Desde la última vez que el precio superó completamente el indicador Coral Trend (el máximo de la última vela superó la línea Coral Trend), ha habido al menos 1 vela cuyo mínimo está completamente por encima de la línea Coral Trend (para operaciones alcistas) o cuyo máximo está completamente por debajo de la línea Coral Trend (para operaciones bajistas).

-

Se produce un pequeño retroceso en dirección opuesta, durante el cual el precio de cierre se mantiene siempre en el lado opuesto de Coral Trend.

-

Al finalizar el retroceso, el precio de cierre regresa a la dirección principal indicada por Coral Trend.

Las condiciones anteriores son las principales. Además, la estrategia utiliza el indicador ADX o la combinación del histograma de fuerza absoluta y el volumen HawkEye como confirmación de entrada.

El indicador ADX requiere que su valor sea > 20 y que la última vela haya subido. Además, el orden de las líneas DI verde y roja debe coincidir con la dirección de la operación.

El histograma de fuerza absoluta (Absolute Strength Histogram) requiere que su color coincida con la dirección de la operación (alcista = azul, bajista = rojo). El volumen HawkEye requiere que su color coincida con la dirección de la operación (alcista = verde, bajista = rojo).

El mecanismo de salida utiliza el precio máximo o mínimo de las últimas N velas multiplicado por la relación riesgo-recompensa para establecer los niveles de stop loss y take profit. Tanto el valor de N como la relación riesgo-recompensa son configurables mediante parámetros.

Análisis de Ventajas

La mayor ventaja de esta estrategia es que, tras determinar la dirección de la tendencia principal con el indicador Coral Trend, identifica oportunidades de entrada al detectar sus reversiones, evitando seguir la corriente en mercados sin tendencia. Además, el uso de indicadores de confirmación permite filtrar muchas falsas rupturas, mejorando así la tasa de éxito de las entradas.

Por otro lado, la estrategia ofrece un mecanismo completo de control de riesgos, que incluye la configuración del ancho del stop loss y el control del porcentaje de exposición al riesgo, de modo que incluso si una operación individual resulta en pérdidas, el impacto en el capital total no es severo.

Análisis de Riesgos

El mayor riesgo de esta estrategia radica en que, al basar las entradas en indicadores, puede generar la ilusión de que una configuración de parámetros por sí sola puede generar ganancias automáticas. En realidad, la optimización de parámetros y la configuración de reglas deben combinarse con las leyes subyacentes de los movimientos de precios, evaluando de forma intuitiva la relación entre los indicadores y el precio, para así definir una configuración más adecuada al estilo de negociación y al activo.

Además, el ajuste de los niveles de stop loss y take profit también debe ser adecuado: un multiplicador de take profit demasiado grande puede impedir salir con ganancias, mientras que un stop loss demasiado ajustado conlleva un riesgo excesivo. Esto debe establecerse en función de la volatilidad del activo y la tolerancia al riesgo personal.

Direcciones de Optimización

Las posibles áreas de mejora de esta estrategia incluyen:

-

Ajustar los parámetros del indicador Coral Trend para que reaccione de manera más sensible a los movimientos de precios de diferentes activos.

-

Probar diferentes indicadores o combinaciones de confirmación, como KDJ, MACD, etc., para obtener señales de entrada más precisas.

-

Ajustar el cálculo de los niveles de stop loss y take profit según la volatilidad de cada activo, logrando un mejor control del riesgo.

-

Incorporar un módulo de gestión de capital que permita ajustar el tamaño de las órdenes en función del número de posiciones, controlando eficazmente las pérdidas totales.

-

Añadir un módulo de control del horario de negociación, para que la estrategia opere solo en periodos específicos, evitando pérdidas durante momentos de alta volatilidad.

Conclusión

Esta estrategia utiliza primero el indicador Coral Trend para determinar la tendencia de precios a mediano y largo plazo. Luego, mediante la identificación de sus reversiones y el filtrado de falsas rupturas con señales de confirmación, construye una estrategia de seguimiento de tendencia relativamente fiable. Además, la sólida configuración de control de riesgos permite que la estrategia opere a largo plazo con estabilidad en el capital. Mediante una mayor optimización de parámetros y módulos, se espera que esta estrategia pueda adaptarse a más activos, ofreciendo una mejor estabilidad y rentabilidad.

- 1