Estrategia cuantitativa de seguimiento de tendencia basada en el indicador Hull y el indicador LSMA

Resumen

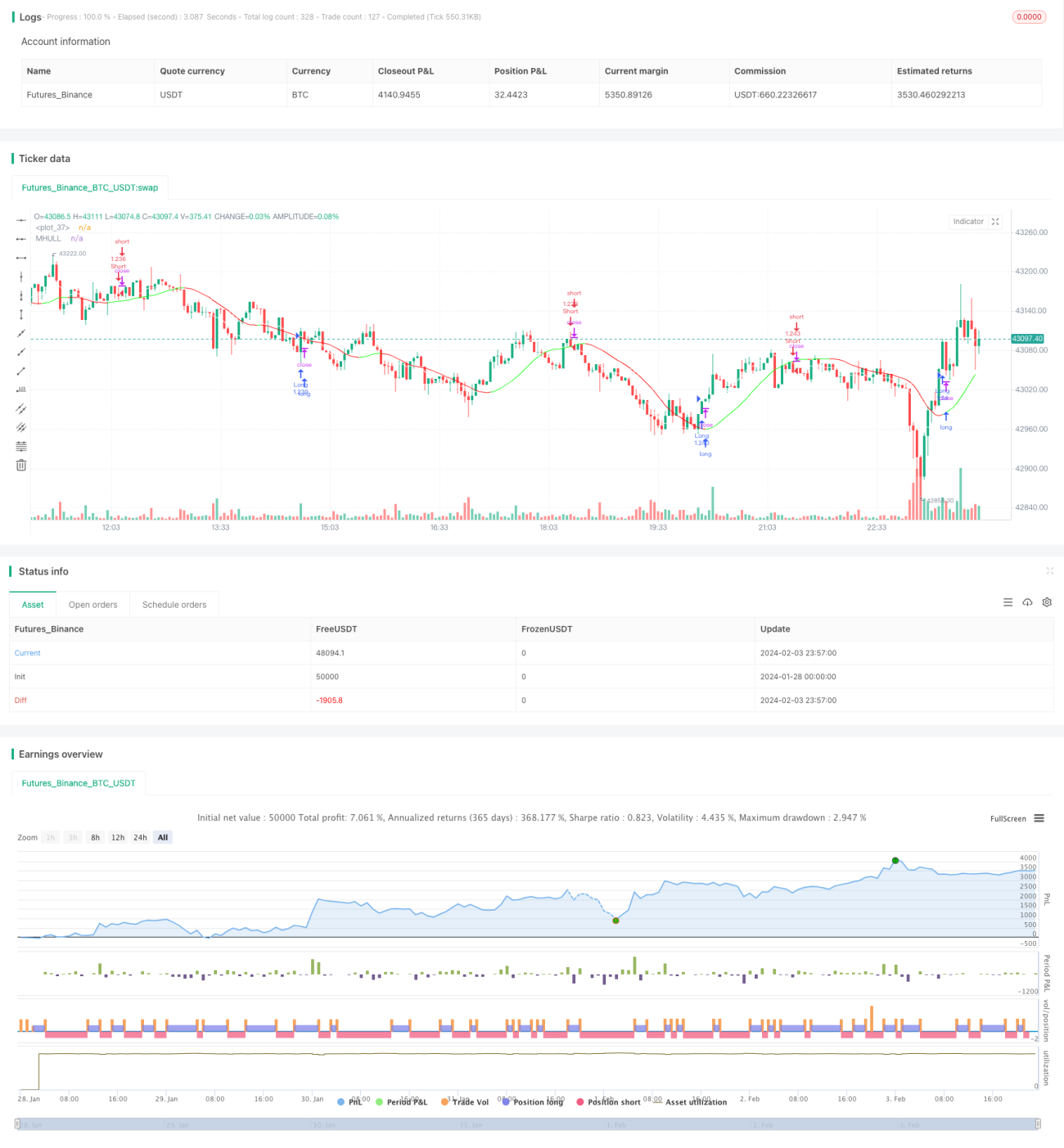

Esta estrategia combina el indicador Hull y el indicador LSMA (Media Móvil de Mínimos Cuadrados) para identificar la dirección de la tendencia y los puntos de reversión, logrando así seguir la tendencia. Cuando el indicador Hull muestra una tendencia alcista y el LSMA cruza por encima del Hull, se abre una posición larga; cuando el indicador Hull muestra una tendencia bajista y el LSMA cruza por debajo del Hull, se abre una posición corta. Esta estrategia es adecuada para trading de baja y media frecuencia, y se puede utilizar en un marco temporal de 1 minuto.

Principio de la estrategia

-

El indicador Hull se utiliza para determinar la dirección de la tendencia del valor. Cuando la línea media (MHULL) está por encima de la línea inferior (LHULL), indica una tendencia alcista; en caso contrario, indica una tendencia bajista.

-

El indicador LSMA se utiliza para identificar puntos de reversión de la tendencia. Cuando el LSMA cruza por encima del MHULL, indica que la tendencia alcista se está formando o acelerando; cuando el LSMA cruza por debajo del MHULL, indica que la tendencia bajista se está formando o acelerando.

-

Combinando ambos, cuando el indicador Hull muestra una tendencia alcista (MHULL > LHULL) y el LSMA cruza por encima del MHULL, se abre una posición larga; cuando el indicador Hull muestra una tendencia bajista (MHULL < LHULL) y el LSMA cruza por debajo del MHULL, se abre una posición corta.

-

El stop loss se establece en el punto de fluctuación más reciente. El stop loss para posiciones largas es el mínimo reciente, y para posiciones cortas es el máximo reciente.

Análisis de ventajas

Esta estrategia presenta las siguientes ventajas:

-

El indicador Hull reacciona rápidamente y puede capturar los cambios de tendencia a tiempo; el LSMA tiene una fuerte suavidad, lo que hace que la identificación de señales de reversión sea precisa y confiable. La combinación de ambos produce buenos resultados.

-

El cruce del LSMA filtra las señales falsas del indicador Hull, reduciendo la probabilidad de operaciones erróneas.

-

El uso de puntos de fluctuación como niveles de stop loss protege al máximo el capital.

-

Es adecuada para trading de baja y media frecuencia y se puede utilizar en marcos temporales de 1 minuto o incluso inferiores, lo que le confiere una amplia aplicabilidad.

Análisis de riesgos

Esta estrategia también presenta algunos riesgos:

-

En mercados laterales, el indicador Hull y el LSMA pueden generar múltiples cruces, lo que provoca un exceso de operaciones. Se deben ajustar adecuadamente los parámetros para reducir la frecuencia de trading.

-

El stop loss basado en puntos de fluctuación puede activarse debido a ajustes de precios a corto plazo, por lo que se debe ampliar adecuadamente la distancia de los niveles de stop loss.

-

Debido al retraso del indicador LSMA, puede haber un ligero riesgo de juicio erróneo. Se debe confirmar con otros indicadores, como patrones de velas.

Direcciones de optimización

Esta estrategia se puede optimizar en los siguientes aspectos:

-

Optimizar los parámetros del indicador Hull y del LSMA para que su combinación se ajuste mejor a diferentes instrumentos y marcos temporales.

-

Agregar condiciones de filtro basadas en volatilidad, volumen, etc., para evitar operaciones erróneas en mercados laterales.

-

Incorporar algoritmos de aprendizaje automático para ayudar a determinar la tendencia predominante.

-

Utilizar técnicas como el aprendizaje profundo para identificar niveles clave de soporte y resistencia, haciendo que el stop loss sea más razonable.

Resumen

Esta estrategia, mediante la combinación del indicador Hull y el LSMA, evalúa los cambios en la dirección de la tendencia y ejecuta operaciones de seguimiento de tendencia. Sus ventajas son la simplicidad de operación, la rápida respuesta y la amplia aplicabilidad en el trading cuantitativo de baja y media frecuencia. Mediante una mayor optimización de las condiciones de filtro, la asistencia en la toma de decisiones y los algoritmos de stop loss, se pueden obtener mejores resultados de la estrategia.

- 1