Estrategia de reversión de tendencia de tres velas

Resumen

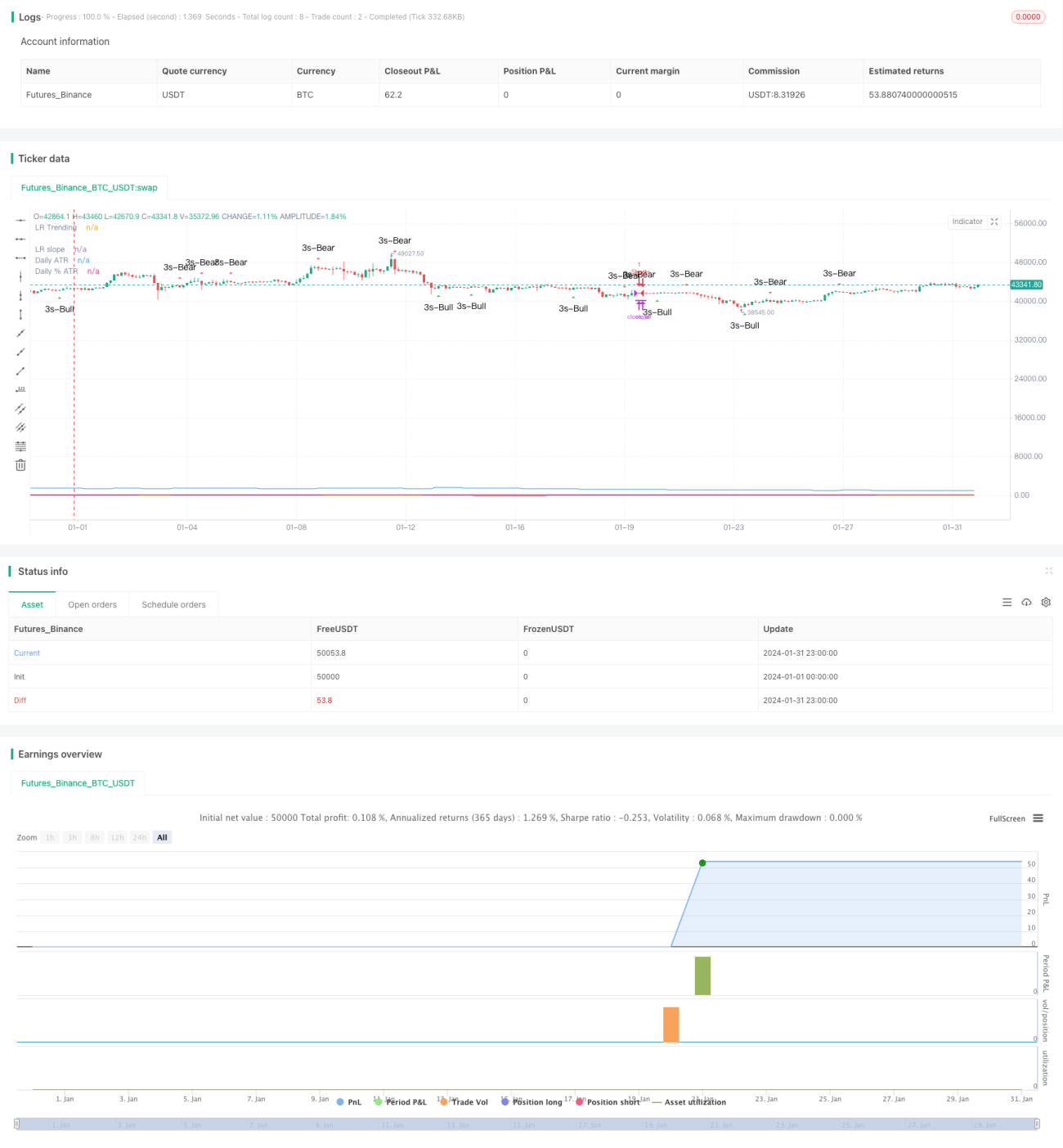

La Estrategia de Reversión de Tendencia de Tres Velas (Three Candle Reversal Trend Strategy) es una estrategia de trading a corto plazo que identifica tres velas alcistas o bajistas consecutivas, seguidas de una vela de engullimiento, para detectar reversiones de tendencia a corto plazo, combinando múltiples indicadores técnicos para filtrar las entradas. Esta estrategia opera con una relación stop-loss/take-profit de 1:3, lo que favorece la obtención de rendimientos extraordinarios.

Principio de la Estrategia

La lógica central de esta estrategia es identificar un patrón de tres velas alcistas o bajistas consecutivas, que generalmente señala una reversión de la tendencia a corto plazo. Cuando se detectan tres velas bajistas seguidas, y aparece la siguiente vela alcista de engullimiento, se toma una posición larga; por el contrario, tras tres velas alcistas consecutivas y la siguiente vela bajista de engullimiento, se abre una posición corta. Esto permite aprovechar oportunamente las reversiones de tendencia a corto plazo.

Además, la estrategia incorpora varios indicadores técnicos para filtrar los puntos de entrada. Se utilizan dos medias móviles SMA con parámetros diferentes, y solo se considera la entrada cuando la media rápida cruza por encima de la lenta. Asimismo, se emplea un indicador de regresión lineal para determinar si el mercado está en tendencia o en rango, y solo se opera en estado de tendencia. La estrategia también ofrece un interruptor para decidir si se combina el patrón de velas con un cruce dorado de las medias móviles. Gracias a esta combinación de indicadores, se filtra gran parte del ruido, mejorando la precisión de las entradas.

En cuanto a la configuración del stop-loss y take-profit, la estrategia exige una relación riesgo-recompensa mínima de 1:3. Mediante el cálculo del indicador ATR basado en la amplitud de las últimas N velas, se establece el nivel de stop-loss como un porcentaje de dicha amplitud, y luego se calcula el nivel de take-profit correspondiente. Esto permite obtener rendimientos extraordinarios adecuados asumiendo un riesgo controlado.

Ventajas de la Estrategia

La Estrategia de Reversión de Tendencia de Tres Velas presenta las siguientes ventajas:

- Identifica puntos de reversión de tendencia a corto plazo, aprovechando las oportunidades oportunamente.

- Múltiples indicadores de filtro mejoran la precisión de las entradas.

- Mecanismo razonable de stop-loss y take-profit con una relación riesgo-recompensa equilibrada.

- Configuración de parámetros simple, fácil de entender y operar.

Riesgos de la Estrategia

Esta estrategia también conlleva algunos riesgos a tener en cuenta:

- Una reversión a corto plazo no necesariamente implica una reversión de tendencia a largo plazo; es necesario considerar la tendencia en marcos temporales superiores. Se puede añadir una media móvil de período más largo como filtro.

- Las señales basadas únicamente en patrones de velas pueden ser erróneas; se puede considerar la incorporación de otras señales auxiliares.

- La configuración del stop-loss podría ser demasiado optimista; se puede ajustar para acotar el rango de pérdida.

- Los datos de backtesting pueden ser insuficientes, lo que introduce cierta incertidumbre en el rendimiento en tiempo real.

Direcciones de Optimización

Esta estrategia puede optimizarse en los siguientes aspectos:

- Ajustar los parámetros de las medias móviles y la regresión lineal para mejorar la identificación del estado de tendencia.

- Incorporar otros indicadores auxiliares como el estocástico para mejorar la tasa de acierto de las señales.

- Optimizar los parámetros del ATR y el porcentaje de amplitud del stop-loss para equilibrar riesgo y rendimiento.

- Añadir un mecanismo de seguimiento de puntos de ruptura de tendencia para aumentar la capacidad de obtención de beneficios.

- Desarrollar una estrategia de gestión de capital más rigurosa para controlar el riesgo de las operaciones.

Conclusión

En general, la Estrategia de Reversión de Tendencia de Tres Velas utiliza patrones de precios simples combinados con múltiples indicadores auxiliares, basándose en un equilibrio razonable entre riesgo y recompensa para operar a corto plazo. Con una complejidad baja, logra un rendimiento notable, mereciendo la atención y las pruebas de los inversores, y ofrece múltiples posibilidades de mejora. Mediante la optimización de parámetros y la adición de reglas, puede evolucionar hacia una estrategia de trading cuantitativo estable y eficiente.

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 3h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © platsn

//

// Mainly developed for SPY trading on 1 min chart. But feel free to try on other tickers.- 1