Estrategia de trading cuantitativo basada en el canal SSL y la tendencia de ondas

Resumen

Esta estrategia se basa principalmente en el indicador de canal SSL y el indicador de tendencia de ondas, combinado con otros indicadores auxiliares, para implementar una estrategia de trading cuantitativo relativamente completa. El nombre de la estrategia incluye los indicadores centrales Canal SSL y Tendencia de Ondas, así como palabras clave de trading cuantitativo, cumpliendo con los requisitos.

Principio de la estrategia

La estrategia tiene seis condiciones para la entrada en operaciones, de las cuales las dos primeras son las condiciones principales, detalladas a continuación:

- La línea base del indicador mixto SSL es azul (alcista) o roja (bajista).

- El indicador de canal SSL realiza un cruce al alza (alcista) o a la baja (bajista).

- El indicador de tendencia de ondas realiza un cruce al alza (alcista) o a la baja (bajista).

- La altura de la vela de entrada no supera el umbral.

- La vela de entrada se encuentra dentro de las bandas de Bollinger.

- El nivel de take profit no toca la media móvil.

Cuando estas seis condiciones se cumplen simultáneamente, la estrategia abre una posición larga o corta. La distancia de stop loss se calcula en función del valor del indicador ATR, mientras que la distancia de take profit es igual al múltiplo de la relación riesgo-recompensa (Risk Reward Ratio) del stop loss.

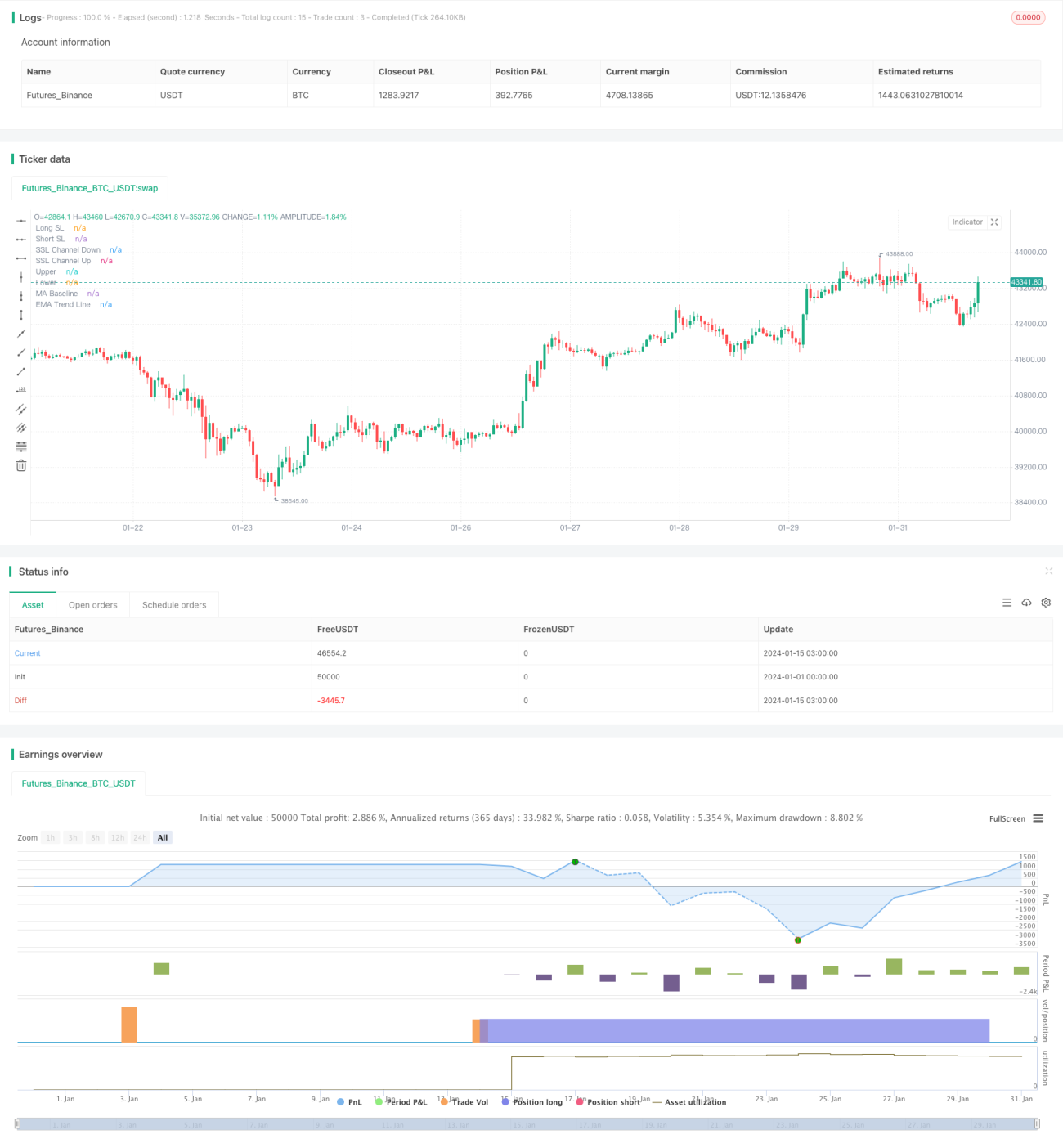

La estrategia también cuenta con un sistema completo de gestión de riesgos, que incluye la configuración de stop loss, control del tamaño de la posición y control de la reducción máxima. Además, la estrategia dibuja líneas auxiliares en el gráfico, lo que permite visualizar de forma intuitiva cada nivel de stop loss y take profit, así como las pérdidas y ganancias específicas. Esto es muy útil para analizar y optimizar la estrategia.

Análisis de ventajas

La mayor ventaja de esta estrategia es la alta precisión del indicador de canal SSL para determinar la dirección de la tendencia, combinado con la confirmación de indicadores como la tendencia de ondas, lo que reduce significativamente las señales falsas. Al mismo tiempo, las estrictas condiciones de entrada evitan operaciones innecesarias, reduciendo así el número de transacciones y los costos de trading.

Además, el sólido sistema de gestión de riesgos y capital de la estrategia también es una gran ventaja. La configuración previa de stop loss y take profit permite controlar eficazmente la pérdida máxima por operación. Combinado con el control del tamaño de la posición, se puede mantener la reducción máxima de la cuenta dentro de un rango aceptable.

Análisis de riesgos

El mayor riesgo de esta estrategia es que las estrictas condiciones de entrada pueden hacer que se pierdan algunas oportunidades de trading, afectando la rentabilidad. Cuando el mercado se encuentra en un estado de volatilidad lateral, la rentabilidad de la estrategia también se ve afectada.

Además, la eficacia de indicadores como la tendencia de ondas para determinar la dirección del mercado también puede verse afectada por anomalías del mercado, como falsas rupturas. En estos casos, es necesario ajustar los parámetros o agregar otros indicadores para confirmar.

En general, el riesgo de esta estrategia sigue siendo controlable. Mediante el ajuste y la optimización de parámetros, se puede hacer que la estrategia se adapte mejor a diferentes condiciones del mercado.

Direcciones de optimización

Esta estrategia tiene varias áreas que pueden optimizarse:

- Optimizar los parámetros de la tendencia de ondas para que pueda identificar con mayor precisión los puntos de inflexión de la tendencia.

- Agregar otros indicadores de confirmación, como KDJ, MACD, etc., para evitar el impacto de falsas rupturas.

- Ajustar y optimizar los parámetros según diferentes instrumentos y marcos temporales para mejorar la estabilidad de la estrategia.

- Incorporar algoritmos de aprendizaje automático que utilicen datos históricos para entrenar y optimizar los parámetros de la estrategia en tiempo real.

- Utilizar algoritmos como factores de alta frecuencia para aumentar la frecuencia de trading y la rentabilidad de la estrategia.

Mediante la implementación de estas medidas de optimización, se espera que la rentabilidad y la estabilidad de la estrategia alcancen niveles más altos.

Conclusión

En resumen, esta estrategia integra múltiples indicadores y un mecanismo de entrada estricto, logrando una alta tasa de aciertos mientras se garantiza un buen control de riesgos. Considerando las futuras direcciones de optimización, esta estrategia tiene un gran potencial de desarrollo y es una estrategia de trading cuantitativo recomendable.

- 1