Estrategia de trading de reversión por ruptura de canal

Resumen

La estrategia de trading de reversión por ruptura de canal es una estrategia de reversión que sigue un canal de precios con puntos de toma de ganancias y stop loss móviles. Utiliza el método de media móvil ponderada para calcular el canal de precios y establece posiciones largas o cortas cuando el precio rompe el canal.

Principio de la estrategia

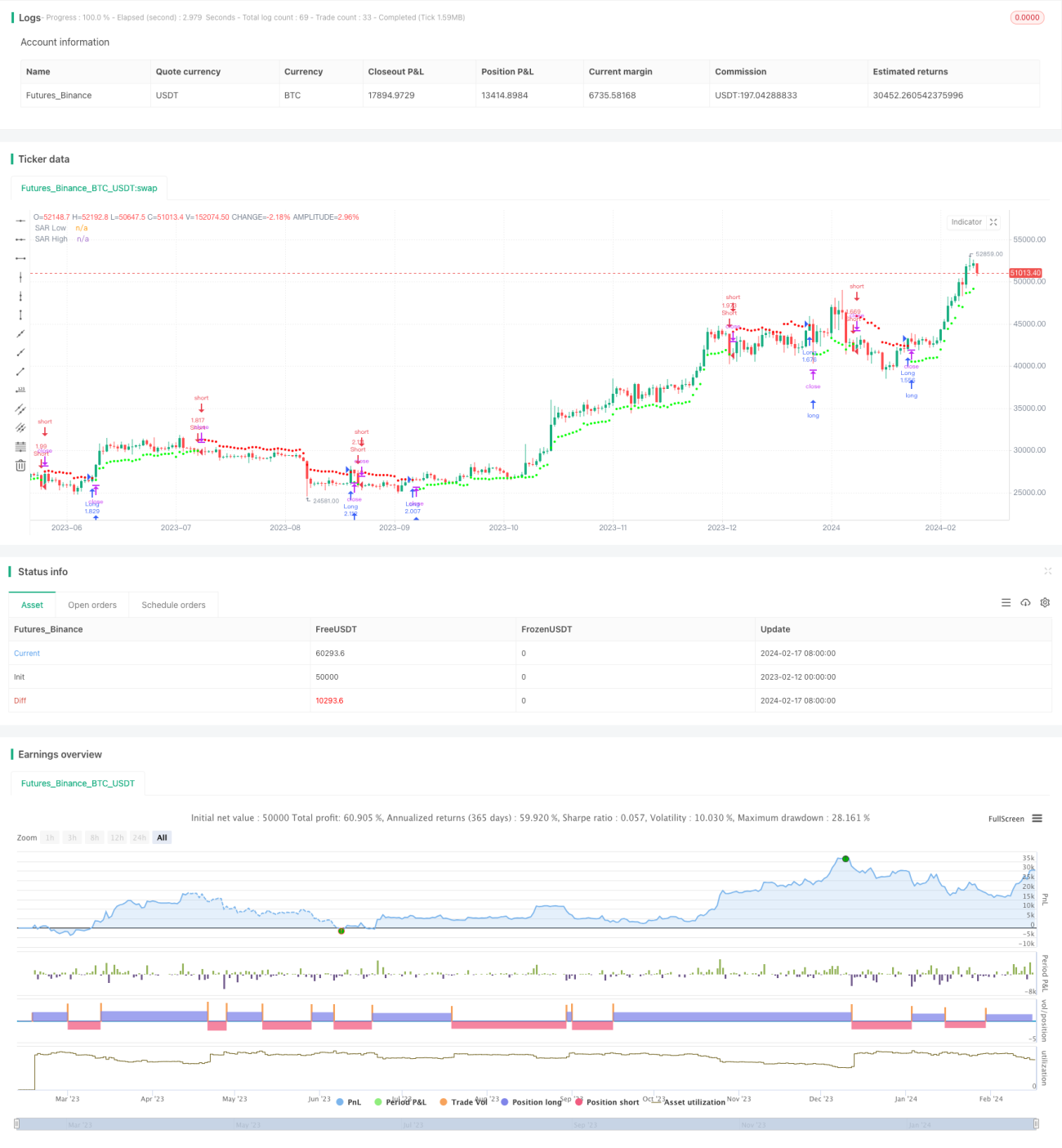

La estrategia primero calcula la volatilidad del precio utilizando el indicador de rango verdadero promedio (ATR) de Wilder. Luego, basándose en el valor ATR, calcula la constante de rango promedio (ARC). El ARC es la mitad del ancho del canal de precios. A continuación, calcula los límites superior e inferior del canal, que son los puntos de toma de ganancias y stop loss, denominados puntos SAR. Cuando el precio rompe el límite superior, se abre una posición corta; cuando rompe el límite inferior, se abre una posición larga.

Específicamente, primero se calcula el ATR de las últimas N velas. Luego se multiplica el ATR por un coeficiente para obtener el ARC. El ARC multiplicado por el coeficiente controla el ancho del canal. El ARC se suma al precio de cierre más alto de las N velas para obtener el límite superior del canal, es decir, el SAR alto. El ARC se resta del precio de cierre más bajo para obtener el límite inferior del canal, es decir, el SAR bajo. Si el precio de cierre rompe el límite superior, se abre una posición corta; si rompe el límite inferior, se abre una posición larga.

Ventajas de la estrategia

- Utiliza la volatilidad del precio para calcular un canal adaptativo que puede seguir los cambios del mercado.

- Es una estrategia de reversión, adecuada para mercados con cambios de tendencia.

- Los stops móviles de toma de ganancias y pérdidas permiten asegurar ganancias y controlar el riesgo.

Riesgos de la estrategia

- Las operaciones de reversión pueden quedar atrapadas fácilmente; es necesario ajustar adecuadamente los parámetros.

- En mercados con grandes fluctuaciones, las posiciones pueden cerrarse fácilmente.

- Parámetros inadecuados pueden provocar operaciones excesivamente frecuentes.

Soluciones:

- Optimizar el período ATR y el coeficiente ARC para que el ancho del canal sea razonable.

- Combinar indicadores de tendencia para filtrar los momentos de entrada.

- Aumentar el período ATR para reducir la frecuencia de las operaciones.

Direcciones de optimización de la estrategia

- Optimizar el período ATR y el coeficiente ARC.

- Agregar condiciones de apertura, como combinar el indicador MACD.

- Agregar una estrategia de stop loss.

Resumen

La estrategia de trading de reversión por ruptura de canal utiliza un canal para seguir los cambios de precio, abriendo posiciones en reversión cuando la volatilidad aumenta, y establece stops móviles adaptativos de toma de ganancias y pérdidas. Esta estrategia es adecuada para mercados laterales dominados por reversiones; si los puntos de reversión se identifican con precisión, puede generar buenos rendimientos de inversión. Sin embargo, se debe prestar atención a evitar stops demasiado amplios y problemas de optimización de parámetros.

- 1